|

市場調査レポート

商品コード

1851205

世界のペット保険:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Global Pet Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 世界のペット保険:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月23日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

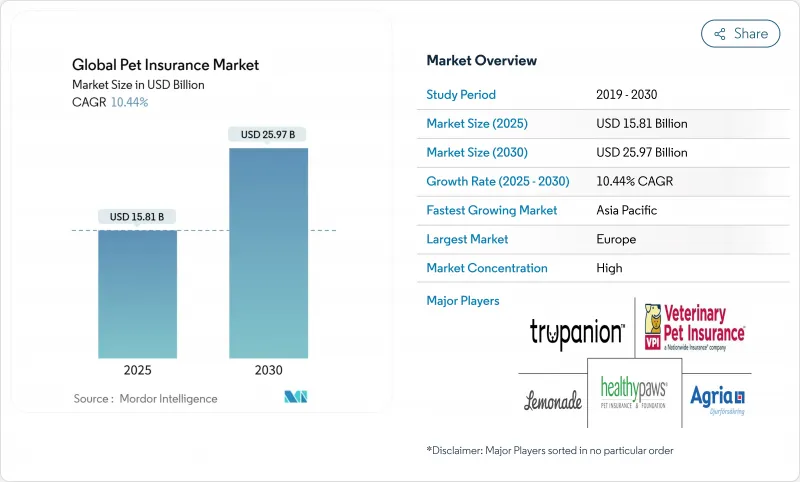

世界のペット保険市場は2025年に158億1,000万米ドルに達し、2030年にはCAGR 10.44%を反映して259億7,000万米ドルに達すると予測されています。

この堅調な成長見通しは、世界的なペット飼育率の上昇、獣医学的インフレの深刻化、規制の明確化によって、一部のレガシー・プレーヤーが保険契約数を削減する中でも保険料が拡大し続けていることを裏付けています。一般的なインフレ率を上回るペースで上昇している高額な獣医療費の自己負担分を包括的な補償で補うことができるため、保険料の引き上げは引き続き堅調です。デジタル・ネイティブの保険会社は、ペットケアのエコシステム内に組み込まれた販売網が意向の高い瞬間に顧客を捕捉する一方で、加入の摩擦を減らすことで加入を加速させています。AIを活用したクレーム自動化の並行的な進展により、処理コストの削減とサービススピードの向上が図られ、新規契約者のペット保険市場に対する好意的な認識が強まる。

世界のペット保険市場動向と洞察

ペット飼育の増加とペットの人間化

ペット飼育の増加とペットを家族の一員とみなす考え方が、堅調な保険料需要を後押ししています。ペットのケアに対する世界の支出は2023年に1,470億米ドルに達し、中でも獣医サービスが最も急成長しているため、飼い主は経済的保護を求めるようになっています。ミレニアル世代とZ世代がペット飼育率を押し上げ、腫瘍学や整形外科手術のような高度な治療に対して高い支払い意欲を示しています。中国はこの人口動態の変化を示しており、80%の飼い主がパンデミック後も支出を維持または増やし、猫経済を強化しています。飼い主とペットの間の感情的な結びつきは、ペット保険市場の比較的価格弾力的な需要につながり、長期的な拡大を支えています。

CPIを上回る獣医療費の上昇

米国労働統計局は、2024年の獣医療サービスCPIの前年比上昇率を8.1%と、一般的なCPI上昇率の2倍以上を記録しました。その要因としては、人材不足(AVMA Workforce Dashboardによると、2024年の獣医の欠員は24%増)、および現在世界中で2,500以上の病院を運営するマース・ベテリナリーヘルス社のような大手チェーンに価格決定権が集中する統合の進行が挙げられます。Trupanionの請求データ集計によれば、犬の十字靭帯修復術の平均請求額は2024年に4,700米ドルを超え、2年間で19%急増しました。NAPHIAは、2024年に北米で初めて保険金支払額が40億米ドルを超え、前年比23%増になると指摘しています。保険金の増加は損害率を圧迫するが、同時に包括的な補償の価値を拡大し、保険料の伸びを維持します。

可処分所得に対する保険料の高いインフレ率

保険料の伸びは多くの世帯の賃金上昇を上回り続けています。カリフォルニア州保険局は、2024年の全州平均で12~15%の保険料上昇を示す料率申請を承認し、沿岸部の郡では20%を超えるところもあります。レモネードの2024年第4四半期の株主書簡では、動物病院のインフレと薬品費の上昇を理由に、ペット保険商品の価格を14%引き上げることを明らかにしています。米国の実質賃金の中央値は同時期にわずか4%しか上昇していないため、経済格差は拡大し、AVMA Practice Metricsプログラムによって記録された健康診断の受診頻度の2.3%低下を促しています。EUの低所得地域では、FEDIAFの2024年調査によると、保険料を理由に保険加入を見送った飼い主は26%で、2022年の19%から増加しています。所得の伸びが回復するか、低価格の新商品が登場しない限り、特に新興市場において、価格に敏感な層への普及は停滞する可能性があります。

セグメント分析

傷害・疾病保険は2024年の保険料の64.1%を占め、ペット保険市場の中核をなしています。このセグメントは、飼い主が2万米ドルを超えるような高額な緊急事態からの保護を重視することから、安定した更新を享受しています。CAGR13.23%の成長が予測されるウェルネス・アドオンは、商品を災害時だけでなく、定期検診や予防接種にまで広げるものです。このような位置づけは、一括払いの獣医費用よりも予測可能な月々の費用を予算化することを好む若い層を惹きつける。ペット保険のウェルネス補償の市場規模は、より多くの保険会社が予防サービスを疾病補償にバンドルすることで差別化を図り、保険金の支払いを安定させるため、急速に拡大すると予測されます。

包括的なモデルは遺伝性疾患や慢性疾患にも対応し、かつては顧客満足の妨げとなっていた不意打ち的な除外項目を減らします。2024年第1四半期のデータでは、特別食などの経常費用が421米ドル、X線検査が819米ドルとなっており、包括的なプランに対する消費者の意欲が強まっています。リスクプールが成熟し、AI主導のアンダーライティングが価格設定を洗練させるにつれ、保険会社は人間の医療保険を反映したより広範な給付パッケージを提供しながらも利幅を維持することができます。

2024年の保険料に占める犬の割合は78.2%で、これは犬の飼育が定着していることと平均的な獣医費用が高いことを反映した水準です。米国、ドイツ、英国では犬の個体数が多いため、正確なプライシングを支える保険数理上のデータセットが充実しており、イヌのペット保険市場シェアは安定しています。ネコはその後に続くが、取引額が低いためネコの保険はより価格に敏感で、給付金のキャリブレーションに影響を与えています。

エキゾチック・ペットは、鳥、ウサギ、爬虫類の専門的な補償が登場するにつれて、2030年までのCAGRが12.21%と最も急速に成長するスライスを形成しています。Nationwide社が2024年に鳥類とエキゾチック・ペットの保険に最高90%の払い戻しを行うプランを発表したことは、米国世帯の15%が従来とは異なる動物を飼っていると推定されることに対する市場の反応を示しています。専門獣医の不足により平均治療費が上昇することで、価値提案が強化され、保険加入が促進されます。その結果、保険料が多様化し、ペット保険市場全体が従来の犬・猫セグメントにとどまらない広がりを見せています。

地域分析

欧州は2024年の世界保険料の44.1%を占め、数十年にわたるペット保険の規制支援と文化的正常化を反映しています。スウェーデンは1世紀以上前にこのカテゴリーを開拓し、消費者の信頼の基盤を築いた。ドイツ、英国、フランスは、厳しい動物愛護法と高い可処分所得に支えられ、この地域の保険料の大部分を占めています。この地域の規制当局によれば、2024年の損害保険売上高の19%をデジタル・チャネルが占めており、今後数年間でペット保険市場をさらに押し上げるであろうオンラインの勢いが増していることを示しています。

アジア太平洋は2030年までのCAGRが10.50%で、最も急成長している地域です。中産階級の所得が上昇し、主要都市で猫ブームが起こる中、ペットケア経済がCAGR12.9%で拡大している中国がこの軌道を牽引しています。普及率はまだ低いが、対応可能なペット数が多いため、ペット保険市場の認知度と規制の明確性が向上すれば、ペット保険市場は大幅な成長を遂げることになります。日本は成熟した顧客基盤を維持し、オーストラリアは北米の消費者行動を反映してペット保険への加入意欲が高いです。インドと東南アジア諸国は、可処分所得が増加し、ペット医療に対する文化的態度が進化すれば、長期的な可能性があります。

北米は、2023年末時点で年率16.7%増の625万頭のペット保険に加入しており、引き続き大規模な保険取扱高を確保しています。高度な獣医療インフラが高価値の保険設計を支えているが、激しい競合が利幅を圧縮しています。複数の州にまたがるNAICモデル法の実施により、情報開示が標準化され、コンプライアンス上のばらつきが減少し、複数州にまたがる商品の発売が簡素化されます。カナダは増加成長に寄与し、メキシコの中産階級の拡大は将来の上昇を示唆します。継続的な保険料のインフレは当面の逆風であるが、高額な獣医費用に直面する飼い主の間で保険の価値が認識されつつあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- ペット飼育の増加とペット・ヒューマニゼーションの動向

- CPIを上回る獣医療費の高騰

- マイクロチップ義務化とNAICモデル法の展開

- ペットケアのエコシステム(小売業者、ウェルネス・アプリ)に組み込まれた保険

- 雇用主負担のペット福利厚生プログラム

- AIを活用したダイナミック・アンダーライティングとリアルタイム・クレーム・オートメーション

- 市場抑制要因

- 高い保険料インフレ対可処分所得

- 世界的に統一された獣医手技コーディングの欠如

- 特定品種の不利な損害率が引き金となった保険会社の撤退

- 新興市場における認知度の低さと文化的障壁

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力/消費者

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 政策タイプ別

- 事故と病気

- 事故のみ

- ウェルネス/予防ケア・アドオン

- 慢性/遺伝性疾患

- 動物のタイプ別

- 犬

- 猫

- その他のペット(鳥類、エキゾチック、馬など)

- プロバイダータイプ別

- 民間保険会社

- 相互保険会社/協同組合保険会社

- インシュアテック・オンリー・プロバイダー

- 政府関連/公的スキーム

- 販売チャネル別

- ダイレクト・ツー・コンシューマー(デジタル&電話)

- 仲介型(代理店/ブローカー、バンカシュアランス、その他の伝統的な第三者チャネルを含む)

- 組み込み(ペット小売店、動物病院、eコマース)

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧(スウェーデン、ノルウェー、デンマーク、フィンランド)

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Trupanion Inc.

- Nationwide(VPI)

- Anicom Holdings Inc.

- Embrace Pet Insurance Agency LLC

- Figo Pet Insurance LLC

- Hartville Group(ASPCA)

- Healthy Paws Pet Insurance LLC

- Lemonade Inc.

- ManyPets Ltd.

- Agria Djurforsakring AB

- RSA Group(MORE THAN)

- Petplan(Fetch)

- Pets Best Insurance Services LLC

- MetLife Pet Insurance(PetFirst)

- Dotsure.co.za

- Oneplan(South Africa)

- PetSure(Australia)

- iPet Insurance(Japan)

- Chewy/Trupanion Pet-Partner Plans

- Pumpkin Pet Insurance(Zoetis)

- Allianz(Petplan Germany)