|

市場調査レポート

商品コード

1851202

湿潤創傷ドレッシング:市場シェア分析、産業動向&統計、成長予測(2025年~2030年)Moist Wound Dressings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 湿潤創傷ドレッシング:市場シェア分析、産業動向&統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月17日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

概要

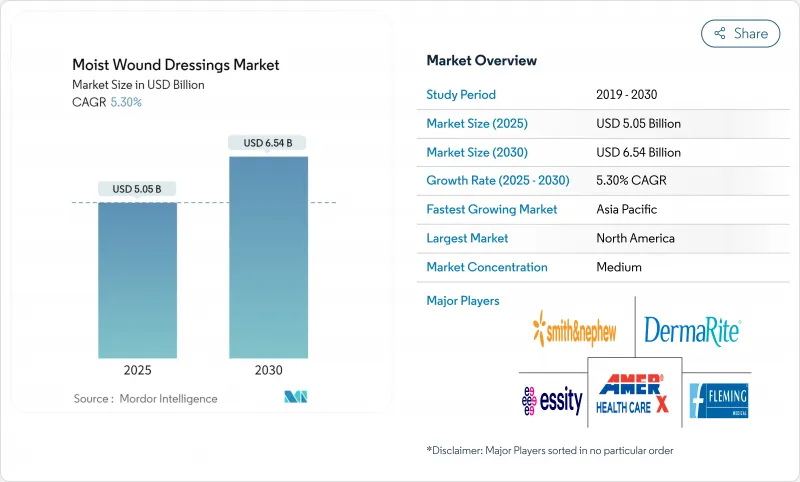

湿潤創傷ドレッシング市場は2025年に50億5,000万米ドルを生み出し、現在のCAGR 5.30%の成長軌道をたどると、2030年には65億4,000万米ドルに達すると予測されます。

乾燥したガーゼから保湿性のあるソリューションへの継続的な移行がこの進歩を支えています。加齢や糖尿病に関連した慢性創傷の世界的な増加によって、病院や支払者は、水分バランスの最適化によって入院期間の長期化やコストのかかる合併症の発生が抑えられるという認識を強めています。スマートセンサー層、pH応答性ポリマー、抗菌性添加剤によって医療従事者がドレッシング材に期待するものが変化し、かつては日用品だった製品がデータを活用した治療法へと変貌を遂げるにつれ、競合の激しさも増しています。米国食品医薬品局(FDA)は2025年6月、酵素感染感知ドレッシングをクラスII機器に指定し、次世代モニタリング技術の道筋を明確にしました。これと並行して、実証可能な治療効果に報いる償還制度改革により、エビデンスに裏付けられたブランドへの購買決定が促され、材料科学と測定可能な臨床上の有益性を組み合わせることができるメーカーを中心とした統合が促進されています。

世界の湿潤創傷ドレッシング市場の動向と洞察

慢性・急性創傷の増加

慢性創傷を持つ米国人は約670万人で、末梢動脈疾患、肥満、糖尿病が高齢化とともに増加すると予想されています。米国心臓協会は2024年、糖尿病性足潰瘍患者の生涯リスクは25%を超え、切断後5年間の死亡率は70%に達すると指摘しています。このような統計から、医療提供者は治癒サイクルを短縮し、再入院を抑制する高度な湿潤ドレッシング材の早期使用に舵を切っています。欧州連合(EU)の病院コストモデルでは、糖尿病性足潰瘍の入院は患者1人当たり平均4,888ユーロ(5,308米ドル)で、コストの88%が長期入院に関連しています。そのため、支払者は保湿プロトコルをオプションとしてではなく、コスト回避のためのツールとしてとらえています。

老年人口と糖尿病有病率の増加

アジア太平洋では毎年4,500万人以上の65歳以上の高齢者が増加しており、その多くが糖尿病、末梢神経障害、血管不全を患っています。Scientific Reportsによると、糖尿病患者の44.4%が神経障害を発症し、21.7%が切断手術を受け、96.9%がQOLの低下を報告しています。高血糖は酸化ストレスとマクロファージのアンバランスを誘発し、自然閉鎖期を遅らせる。先進湿潤ドレッシング材は、内因性成長因子を温存し、滲出液管理を最適化することにより、このような生物学的障害に対処し、多くの専門クリニックで第一選択治療となっています。

高い製品コストと処置コスト

スペインでは、慢性創傷治療に3年間で3,499万1,854ユーロ(3,805万7,000米ドル)を費やしており、材料費だけで845万5,787ユーロ(920万3,000米ドル)、残りを臨床医の時間が占めています。週に何度もドレッシング材を交換することで、支払者にとっても患者にとっても出費がかさみます。同様のパターンはインドでも見られ、糖尿病性足潰瘍の治療はポケットマネーで支払われることが多く、先進的なドレッシング材へのアクセスが狭まっています。段階的な製品ラインアップと小さなパックサイズは、価格差を埋めることを目的としているが、イノベーションをコモディティ化するリスクがあります。

セグメント分析

発泡ドレッシング材は、術後創傷、圧迫創傷、外傷創傷に幅広く適用できることを反映して、2024年の湿潤創傷ドレッシング市場シェアの23.87%を占めました。ポリウレタンをマトリックスとするドレッシング材は、高い吸収性と断熱性のバランスを保ち、ドレッシング材の交換を減らし、創傷周囲の皮膚を保護します。銀イオンと柔軟なトリラミネートを組み合わせたSmith+NephewのALLEVYN Ag+SURGICALのような技術的なアップグレードは、臨床的な魅力を強化しています。ハイドロコロイドは、現在の売上規模では小さいが、CAGRは最速の6.02%です。高いゲル形成能と7日間の装着時間により、ハイドロコロイドは特に在宅介護において、動けない患者の褥瘡予防策としてますます好まれるようになっています。ハイドロコロイド製剤に対するFDAの合理化された510(k)免除措置は、参入障壁を低くし、ニッチプレーヤーに臭気制御、透明性、生分解性の革新に拍車をかけています。

2025年から2030年にかけて、アルギン酸塩とハイドロゲルのカテゴリーは、発泡体に全面的に課題するのではなく、明確な役割を切り開くと予想されます。アルギン酸塩のカルシウム・ナトリウムイオン交換は、大量に滲出する創傷の止血性能を支えており、救急外来で不可欠な存在であり続ける。冷却鎮痛効果が珍重されるハイドロゲルシートは、腫瘍学関連の放射線熱傷や壊死組織の剥離を支配しています。フィルム、接触層、複合ドレッシング材は、ニッチな地位を保ちつつも、スマート・プラットフォームのセンサー・バッキングとして再注目されています。これらの力学が相まって、湿潤創傷ドレッシング市場で永続的なポジションを目指す企業にとって、多製品ポートフォリオが必須であることを補強しています。

湿潤創傷ドレッシング市場レポートは、製品別(フォーム、アルギン酸塩、ハイドロコロイド、ハイドロゲル、その他)、用途別(熱傷、褥瘡、糖尿病性潰瘍、手術創、その他)、最終用途別(病院、在宅介護、その他)、地域別(北米、欧州、アジア太平洋、中東・アフリカ、南米)に分類されています。本レポートでは、上記すべてのセグメントの金額(米ドル)を掲載しています。

地域分析

北米は依然として技術と償還の進化の震源地です。この地域の支払者は、メディケア、民間保険会社、退役軍人健康管理局であり、臨床的に実証された製品の急速な普及を後押ししています。医療機関は、発泡ドレッシング材とスマートフォン連動のpHセンサーをバンドルした遠隔モニタリングキットの導入を増やしており、炎症が急増した際に即日介入が可能になっています。国境を越えたサプライチェーンは米国・メキシコ・カナダ協定のおかげで回復しているが、メーカー各社は関税や運賃の変動を緩和するために生産を現地化しています。

アジア太平洋の軌跡は、疫学と政策の収束を反映しています。中国の「ヘルシー・チャイナ2030」計画では、慢性疾患予防のための資金が計上され、ハイドロファイバードレッシングが剥離の頻度を減らす糖尿病フットクリニックへの投資が行われています。インドでは、州レベルの医療保険制度が、四肢救済手術を受ける低所得患者に対して高度なドレッシング材を払い戻し、公的セクターの入札を刺激しています。日本と韓国の市場は、超高齢化社会における圧迫傷害の予防に重点を置いており、MRI検査中もそのままの状態を維持できるように設計されたシリコンフォーム製予防材の採用を促進しています。

欧州は微妙な成長を示しています。北欧の医療制度は在宅ケアを重視しており、看護師の訪問を最小限に抑える12日間の装着プロトコルを備えた抗菌性フォームの普及が進んでいます。南欧では公的予算が限られているため、費用対効果の研究が有利です。最近のNHSイングランドの実データでは、プレーンガーゼからハイドロコロイドに切り替えた場合、毎週のドレッシング交換が19%削減され、年間170万米ドルの節約になったことが示されています。東欧の共通調達手続きへの加盟は価格の調和をもたらすが、同時にアジア太平洋地域のサプライヤーとの競合を激化させ、現地の既存企業に持続可能性認証やリサイクル可能なパッケージングによる差別化を迫ることになります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 慢性・急性創傷の増加

- 老年人口と糖尿病有病率の増加

- 加速する在宅慢性創傷管理の導入

- OECD外来診療における有利な診療報酬改革

- 遠隔モニタリングを可能にするスマートセンサー・ドレッシングスの台頭

- 気候の影響による熱傷・外傷の増加

- 市場抑制要因

- 高い製品と手続きコスト

- 新興国における償還の制限

- 湿潤ドレッシングの不適切な使用による感染リスク

- 銀ドレッシング材の環境毒性規制強化

- バリュー/サプライチェーン分析

- テクノロジーの展望

- 規制情勢

- ポーターのファイブフォース分析

- 買い手の交渉力/消費者

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品別

- フォームドレッシング

- アルジネートドレッシング

- ハイドロコロイドドレッシング

- ハイドロゲルドレッシング

- フィルムドレッシング

- コラーゲンドレッシング

- 抗菌/銀ドレッシング

- 接触層ドレッシング

- その他

- 用途別

- 熱傷

- 褥瘡

- 糖尿病性足潰瘍

- 手術創/外傷創

- 静脈性下腿潰瘍

- その他の用途

- エンドユーザー別

- 病院

- 在宅ケア

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 市場シェア分析

- 企業プロファイル

- Smith & Nephew plc

- Molnlycke Health Care AB

- 3M(Health Care)

- ConvaTec Group PLC

- Coloplast A/S

- Essity AB(BSN medical)

- Cardinal Health Inc.

- B. Braun Melsungen AG

- Medtronic plc(Acelity/KCI)

- Johnson & Johnson(Ethicon)

- Lohmann & Rauscher GmbH

- Hartmann Group

- Urgo Medical

- Hollister Incorporated

- Integra LifeSciences

- DermaRite Industries LLC

- AMERX Health Care Corp.

- Fleming Medical Ltd.

- Derma Sciences(Nipro)

- Milliken Healthcare