自動車熱管理:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

Automotive Thermal Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1940587

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

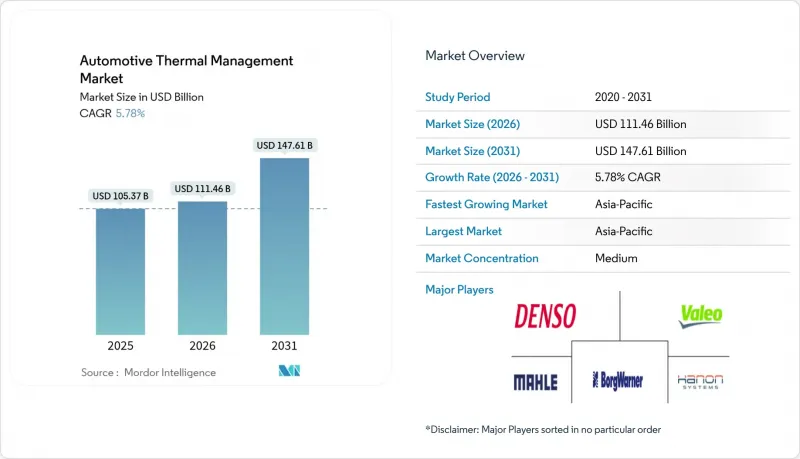

自動車用熱管理市場の規模は、2026年には1,114億6,000万米ドルと推定されております。

2025年の1,053億7,000万米ドルから成長し、2031年には1,476億1,000万米ドルに達すると予測されております。2026年から2031年にかけての年間平均成長率(CAGR)は5.78%と見込まれております。

この成長は、急速な電動化、世界のCO2排出規制およびCAFE規制の強化、ならびに統合型バッテリー冷却システム、車室内空調(HVAC)、パワーエレクトロニクス向け熱ループへの需要増加に起因しております。バッテリー式電気自動車(BEV)は、内燃機関車に比べて単位当たりで5分の2多い熱処理容量を必要とするため、サプライヤーは、バッテリー温度を最適な15~35℃の範囲に維持し、パックの寿命を延ばし、800Vの急速充電ハードウェアをサポートするアーキテクチャの再設計を迫られています。特にアジア太平洋地域における競合圧力により、浸漬冷却、マルチ回路モジュール、PFASフリー冷媒ヒートポンプなどの技術革新が加速し、車両の航続距離、快適性、規制順守性の向上に貢献しております。

世界の自動車用熱管理市場の動向と洞察

主流化するEVが電池熱管理の重要性を高める

バッテリーパックは現在、熱管理予算全体の5分の1を占めており、従来型車両ではごくわずかだった割合から増加しています。現代モービスは最近、標準プレート比で10倍の熱伝達効率を実現し、厚みを0.8mmに薄型化、温度均一性を20℃改善し暴走リスクを大幅に低減するパルス式ヒートパイプを導入しました。統合型ヒートポンプ式HVACは廃熱を回収し、BEVの冬季航続距離をわずかに延長します。また、バッテリー、キャビン、インバーターの冷却機能を統合モジュールにまとめたサプライヤー各社は、複数プラットフォームでの受注を獲得しています。

ボンネット内800Vアーキテクチャが加速するSiCインバータ冷却

プレミアムEVは現在、175℃の接合部温度に対応可能な800Vシリコンカーバイドインバーターを採用しています。液浸絶縁冷却により熱抵抗を0.1℃/W以下に抑え、350kWを超える充電速度を実現するとともに、15万サイクル以上の信頼性を確保しています。NXP社およびWolfspeed社が最近発表したリファレンス設計には、この液体ループが組み込まれており、高電力アプリケーションにおける空冷から直接液体冷却への移行を強調しています。

統合型熱モジュールの高い部品コスト

統合モジュールは複数の部品を単一筐体に集約しますが、このアプローチは個別部品使用と比較してコストを大幅に増加させます。これにより、限られた熱容量予算内で動作する車両には課題が生じます。この課題に対処するため、サプライヤーはプラットフォーム標準化、垂直統合、自動組立プロセスなどの戦略に注力し、コスト効率の向上と量産採算点の達成を目指しています。

セグメント分析

2025年時点で、エンジン冷却は内燃機関車輌の基盤として自動車熱管理市場の35.01%を占めました。一方、バッテリーシステムは5.83%のCAGRで最も急速に拡大しており、OEMメーカーがパック・モジュール・セルレベルの冷却回路へリソースを再配分していることを反映しています。現在ではBEVの熱管理予算のほぼ半分をこれらの回路が占めています。

ステランティスのインテリジェントバッテリー統合システムは冷却プレート、インバーター、充電器を一体化し、エネルギー効率を10%、電力密度を最小限向上させます。デュアルソースヒートポンプの普及により車内空調は安定を維持する一方、廃熱回収とEGRモジュールは商用分野で成長しています。800V駆動系の普及に伴い、モーターとインバーターの冷却技術が急速に進展しており、それぞれ最大200W/cm2の放熱性能が求められています。

2025年時点で、液体間接冷却ループは自動車熱管理市場シェアの42.77%を占めました。これは成熟したラジエーター、リザーバー、ポンプ技術に支えられたものです。液浸冷却に関連する自動車熱管理市場規模はCAGR5.82%で拡大しており、物理的優位性により許容電力密度が10倍向上する特性を反映しています。

現代自動車のナノフィルム空気冷却技術は車内温度を12.5℃低下させ、大幅な省エネルギーを実現し、軽量システムにおける空冷技術のニッチを証明しました。相変化材料はピーク負荷時にセルを保護し、ハイブリッドループは複数の媒体を相互接続し、AI監視による最適経路選択を実現します。

地域別分析

アジア太平洋地域は2025年に自動車熱管理市場シェアの39.17%を占め、5.86%のCAGRで成長を牽引しました。これは2024年にBYDが製造した中国製EVと、2025年の大幅な目標が原動力となっています。ハノンシステムズの大規模なコンプレッサー拡張は、低コストのアジア供給ラインを活用しつつ北米組立を支援します。日本および韓国のティア1サプライヤーは、パルス式ヒートパイプなどの技術革新を推進し、地域の技術競合力を維持しております。

北米は厳しい燃費基準と、フォード、GM、テスラなどの主要自動車メーカーによるEVへの大規模な資本投入により、第2位の地位を確固たるものにしております。先進プラットフォームの急速な普及が、炭化ケイ素インバーター冷却や予測熱制御技術への需要拡大を牽引しております。メキシコのコスト効率に優れた製造拠点は、ポンプ、バルブ、熱交換器への投資を引き続き誘致しておりますが、熟練技術者の不足が複雑なEVサービス業務の管理に課題をもたらしております。

欧州は厳格な規制枠組みと強固なエンジニアリングの伝統を併せ持ちます。野心的な排出削減目標と特定化学物質の段階的廃止が、環境に優しい冷媒への移行を加速させています。フォードは最近プロパンベースのシステムを導入し、熱管理における革新性を示しました。ドイツのメーカーは統合モジュールと排気ガス再循環熱回収システムを優先的に開発しており、フランスではバッテリー式電気自動車への積極的な推進により、バッテリー冷却ソリューションの需要が大幅に増加しています。このプレミアム市場でのポジショニングは、車両1台あたりの熱管理支出の増加を支え、サプライヤーの持続的な収益性を確保しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 主流となるEVの普及がバッテリーの熱管理機能の需要を促進

- 高級装備・快適装備の拡充による自動車1台あたりのHVAC価値向上

- ボンネット下800VアーキテクチャがSICインバータ冷却を加速

- 内燃機関のターボダウンサイジングによるエンジン及びオイルクーラー需要の増加

- 厳格化するCO2排出規制/燃費基準がマルチ回路冷却システムを推進

- PFAS段階的廃止が自然冷媒ヒートポンプへの転換を促進

- 市場抑制要因

- 統合型熱モジュールの高BOMコスト

- 液体/浸漬システムにおける信頼性と漏洩経路リスク

- 低GWP冷媒の供給網不足

- 複雑なEV冷却ループに対するサービス技術者の能力不足

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測(金額(米ドル))

- 用途別

- エンジン冷却

- キャビン/HVAC熱管理

- トランスミッション熱管理

- 廃熱回収/排気ガス再循環(EGR)

- バッテリー熱管理

- モーターおよびパワーエレクトロニクス冷却

- 技術タイプ別

- 空調・冷暖房

- 液体間接冷却

- ダイレクト冷却/液浸冷却

- 相変化/PCMシステム

- ハイブリッド&統合ループ

- コンポーネント別

- 熱交換器(ラジエーター、CAC、オイルクーラー)

- コンプレッサー及びポンプ

- サーマルコントロールバルブ及びマニホールド

- 高電圧冷却液ヒーター

- センサー及びコントローラー

- 推進タイプ別

- 内燃機関車

- ハイブリッド電気自動車

- プラグインハイブリッド車

- バッテリー式電気自動車

- 燃料電池電気自動車

- 車両タイプ別

- 乗用車

- 小型商用車

- 大型トラック・バス

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- フランス

- 英国

- イタリア

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- トルコ

- 南アフリカ

- エジプト

- ナイジェリア

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Denso Corporation

- Hanon Systems

- Valeo SE

- MAHLE GmbH

- Gentherm Inc.

- Robert Bosch GmbH

- Dana Inc.

- BorgWarner Inc.

- Modine Mfg. Co.

- Schaeffler AG

- ZF Friedrichshafen AG

- Kendrion N.V.

- Continental AG

- TI Fluid Systems

- Sanden Holdings

- Boyd Corporation

- VOSS Automotive

- Grayson Thermal Systems

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日