|

市場調査レポート

商品コード

1444179

動物用寄生虫駆除剤:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Veterinary Parasiticides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 動物用寄生虫駆除剤:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

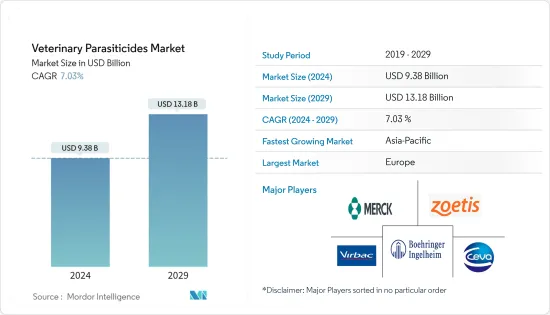

動物用寄生虫駆除剤の市場規模は、2024年に93億8,000万米ドルと推定され、2029年までに131億8,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に7.03%のCAGRで成長します。

COVID-19のパンデミックにより、動物の世話の需要が減少しました。感染症対策と州全体のロックダウンにより、パンデミックは動物病院やクリニックの受診数に影響を与えました。 2022年6月にインディアン・ジャーナル・オブ・アニマル・サイエンスに掲載された研究によると、ロックダウン期間の違いや獣医師間で受診した症例数に大きな差があり、ペットの種類ごとに聞いた症例数が減少した(54.9%)。ロックダウン中はヤギ(35.3%)、羊(29.1%)、牛(25.5%)、水牛(21.6%)が続いた。ロックダウン中、獣医師の受診は27.3%減少し、動物病院への農家の受診は61.9%減少しました。その結果、パンデミック中は獣医師の休日の減少や動物用医薬品の不足により、市場に混乱が生じることが予想されます。しかし、制限が解除されてから業界は急速に回復しました。今後数年間、獣医師の来院数の増加と動物病院の再開が市場の成長を促進すると予想されます。

動物用寄生虫駆除剤市場は、人獣共通感染症の蔓延とペットや家畜から人間への感染の増加、および動物のヘルスケア費の増加により、急速な成長を示すと予想されます。 2021年 9月にInfection Ecology &Epidemiologyに掲載された研究によると、世界で最も危険な人獣共通感染症の1つはサルモネラ症です。動物におけるサルモネラ菌の蔓延とサルモネラ菌種の伝播増加の危険因子動物から人間までがはっきりと分かりました。スペインでは、犬のサルモネラ菌の有病率は1.85%でした。中国では、243頭の犬のサルモネラ菌感染率が9.47%と若干高いことが判明しました。したがって、犬におけるこれらの病気のリスクが高いため、予測期間中に治療の需要が増加すると予想されます。

さらに、世界中でペットの採用が増加しているため、予測期間中に市場の成長が促進される可能性があります。たとえば、人民疾病動物薬局(PDSA)のPAWレポート 2022によると、2022年に英国には1,020万匹のペットの犬、1,110万匹のペットの猫、100万匹のペットのウサギがいたとのことです。同じ情報源は、英国の52%がペットであったと報告しています。このペットの普及の増加により、予測期間中の市場の成長が促進されると予想されます。

したがって、上記のすべての要因が市場の成長を促進すると予想されます。しかし、動物用寄生虫駆除剤の承認に対する厳しい規制政策と動物用寄生虫駆除剤製品の高価格が、動物用寄生虫駆除剤市場の発展を妨げています。

動物用寄生虫駆除剤の市場動向

コンパニオンアニマルは予測期間中に高い成長を示すことが予想されます

コンパニオンアニマル部門は、ペットの飼い主の数とペットの世話に関する追加の意思決定の増加により、高いCAGRで発展すると予想されます。 2021年6月に米国ペット製品協会(APPA)が実施した全国ペット所有者調査2021-2022によると、ペット所有者の51%が、倫理的に調達された環境に優しいペット用品に対しては、より多くのお金を払っても構わないと考えています。さらに、ペットの飼い主の35%は、COVID-19感染症のパンデミック中に、ペット用品、ウェルネス製品、その他のペットケア用品への支出が例年よりも増えたと報告しています。このような事例は、予測期間中の市場の成長にプラスの影響を与える可能性があります。

さらに、人間と動物の間の愛情の結果として、コンパニオンアニマルの養子縁組が世界的に増加しています。これは、不確実な時期のストレスを軽減し、社会的孤立によるうつ病や不安を和らげる効果的な方法として広く認められています。予測期間中のこのセグメントの成長を推進する可能性があります。 2021年 3月、ペットケア生産者工業会(IVH)とドイツペット貿易産業協会(ZZF)は調査結果を発表しました。調査によると、2020年にはドイツの家庭には約3,500万匹の犬、猫、小型哺乳類、ペットの鳥が暮らしていました。全体として、2020年にはドイツの全世帯の47%が少なくとも1匹のペットを飼っていました。この傾向は、2020年にさらに増加すると予想されています。予測期間。

さらに、コンパニオンアニマルの市場関係者による新製品の発売は、市場の成長に重要な役割を果たしています。たとえば、2021年 6月、エランコアニマルヘルスは、犬の総合的な寄生虫防御用の新しいCredelioPlusの最近の英国での販売承認を受けて、包括的な寄生虫駆除剤ポートフォリオの開発を完了しました。

したがって、上記のすべての要因は、予測期間中に市場の成長を促進すると予想されます。

北米は市場で最大のシェアを保持すると予想され、予測期間中にも同様に成長すると予想されます

現在、北米は動物用寄生虫駆除剤市場を独占しており、今後数年間でその傾向が強まると予想されています。米国は、動物の養子縁組の拡大と一人当たりの動物ヘルスケア費の増加により、他国の中でもかなりの市場シェアを維持すると思われます。北米におけるペットの養子縁組の増加傾向も市場の成長を促進すると予想されます。たとえば、米国ペット製品協会(APPA)が実施した2021年から2022年の全国ペット所有者調査によると、米国の世帯の約70%がペットを飼っており、これは9,050万軒に相当し、猫は4,530万匹、犬は6,900万匹となっています。さらに、カナダやメキシコなど、この地域の他の国々でもペットの所有率が最近増加しています。 2022年 5月に発行されたPet Keenによると、カナダの家庭の38%が猫を飼っており、35%が犬を飼っていると予測されています。その結果、この地域でのペットの養子縁組と所有は、これらの動物が寄生虫に感染しやすいため、寄生虫感染の蔓延を増加させると予測されています。さらに、上記の情報源は、カナダのペットの飼い主がこれまで以上にペットにお金を費やしており、17%がペットのヘルスケアに年間500ドル以上を費やす用意があると述べています。その結果、ペットは寄生虫に感染しやすくなり、動物への支出が増加すると寄生虫治療への支出が増加し、市場の成長を促進する可能性があります。

主要企業は、市場の成長に貢献するために、製品の発売、合併、買収、パートナーシップなどの戦略計画と新しい開発を積極的に行っています。たとえば、2022年 6月に、Zoetis Inc.は、非公開のペットケア遺伝学企業であるBasepawsを買収する合意を報告しました。この買収により、精密動物医療分野におけるゾエティスのポートフォリオが前進し、皮膚科および寄生虫駆除剤におけるペットケアのイノベーションの将来のパイプラインに情報が提供され、形成されることになります。したがって、上記の要因は北米の動物用寄生虫駆除剤市場に起因すると考えられ、予測期間中に成長が見られると予想されます。

動物用寄生虫駆除剤業界の概要

動物用寄生虫駆除剤市場は、いくつかの企業が存在し、適度な競争が続いています。業界の主要企業は、地元市場企業の獲得を活用して地理的プレゼンスを拡大することに継続的に注力しています。主要市場企業による地元支払者の動物医療資産の買収により、主要市場企業はさまざまな地理的地域での存在感を高め、動物用医薬品ポートフォリオを拡大することができました。市場参加者には、Elanco Animal Health Incorporated、Boehringer Ingelheim International GmbH、Vetoquinol SA、Zoetis Incなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 食中毒および人獣共通感染症の有病率の上昇

- ペット動物の養子縁組の増加

- 動物医療費の増加

- 市場抑制要因

- 動物用寄生虫駆除剤の厳格な承認プロセス

- 高価な動物用寄生虫駆除剤製品

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 製品タイプ別

- 外部寄生虫駆除剤

- 内部寄生虫駆除剤

- エンドクトサイド

- 動物の種類別

- 食料生産動物

- 伴侶動物

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東およびアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Bayer AG

- Boehringer Ingelheim

- ELI Lilly and Company

- Merck &Co. Inc.

- Sanofi

- Zoetis Inc.

- Ceva Sante Animale

- Virbac

- Perrigo Company PLC

- Soparfin SCA(Vetoquinol SA)

第7章 市場機会と将来の動向

The Veterinary Parasiticides Market size is estimated at USD 9.38 billion in 2024, and is expected to reach USD 13.18 billion by 2029, growing at a CAGR of 7.03% during the forecast period (2024-2029).

The COVID-19 pandemic reduced the demand for animal care. Due to infection control measures and statewide lockdowns, the pandemic impacted the number of visits to veterinary hospitals and clinics. According to the study published in the Indian Journal of Animal Science in June 2022, there was a significant difference in the number of cases attended during different lockdown periods and among veterinarians, with a decline in the number of cases heard across pet species (54.9%), followed by goats (35.3%), sheep (29.1%), cattle (25.5%), and buffalo (21.6%) during the lockdown. During the lockdown, veterinarian visits fell by 27.3%, while farmer visits to veterinary clinics fell by 61.9%. As a result, the market is expected to be disrupted during the pandemic due to decreased veterinary holidays and a lack of veterinary pharmaceuticals during the pandemic. However, since restrictions were removed, the industry recovered quickly. In coming years, a rise in veterinarian visits and the reopening of veterinary clinics are expected to drive the market's growth.

The veterinary parasiticides market will show rapid growth due to the rising zoonotic disease prevalence and transmission from pets and farm animals to humans and rising animal healthcare expenditure. According to the study published in the Infection Ecology & Epidemiology in September 2021, one of the most dangerous zoonotic diseases in the world is salmonellosis. Salmonella prevalence in animals and risk factors for increased transmission of salmonella spp. from animals to people were evident. In Spain, the prevalence of salmonella in dogs accounted for 1.85%. In China, 243 dogs were found to have a slightly higher prevalence of salmonella at 9.47%. Thus, a higher risk of these diseases in dogs is expected to increase the demand for treatment over the forecast period.

Moreover, the growing adoption of pets worldwide is likely to propel the market's growth over the forecast period. For instance, according to the People's Dispensary for Sick Animals (PDSA) PAW Report 2022, there were 10.2 million pet dogs, 11.1 million pet cats, and 1 million pet rabbits in the United Kingdom in 2022. The same source reported 52% of UK adults would own a pet in 2022. This rising adoption of pets is expected to drive the market's growth over the forecast period.

Thus, all the abovementioned factors are expected to propel the market's growth. However, the stringent regulatory policies for the approval of animal parasiticides and the high cost of animal parasiticide products are hindering the development of the veterinary parasiticides market.

Animal Parasiticides Market Trends

Companion Animals is Expected to show High Growth During the Forecast Period

The companion animal segment is expected to develop at a high CAGR due to the increasing number of pet owners and their extra pet care decisions. According to National Pet Owners Survey 2021-2022 by the American Pet Products Association (APPA) in June 2021, 51% of pet owners are willing to pay more for ethically sourced and environmentally friendly pet items. Furthermore, 35% of pet owners reported spending more on pet supplies, wellness products, and other pet care items during the COVID-19 pandemic than in previous years. Such instances may positively impact the market's growth over the forecast period.

Additionally, the adoption of companion animals is rising globally as a result of the affection between humans and animals, which is widely acknowledged as an effective way to reduce stress during a period of uncertainty and assist in easing depression and anxiety due to social isolation, which is likely to propel the segment's growth over the forecast period. In March 2021, the Industrial Association of Pet Care Producers (IVH) and the German Pet Trade and Industry Association (ZZF) announced a survey result; as per the survey, almost 35 million dogs, cats, small mammals, and pet birds lived in German households in 2020. Overall, 47% of all German households owned at least one pet in 2020. The trend is further expected to grow during the forecast period.

Furthermore, new product launches by market players for companion animals play a significant role in market growth. For instance, in June 2021, Elanco Animal Health completed developing its comprehensive parasiticide portfolio with the recent marketing authorization of the new CredelioPlus in the United Kingdom for all-around parasite protection for dogs.

Thus, all the above factors are expected to boost the market's growth over the forecast period.

North America is Expected to Hold a Largest Share in the Market and Expected to do Same in the Forecast Period

North America currently dominates the veterinary parasiticides market and is anticipated to do so in the coming years. The United States is likely to maintain its substantial market share among the other nations, owing to expanding animal adoption and rising per capita animal healthcare expenditure. The rising trend of pet adoption in North America is also expected to drive the market's growth. For instance, according to the National Pet Owners Survey 2021-2022, conducted by the American Pet Products Association (APPA), around 70% of United States households have a pet, equating to 90.5 million houses, with 45.3 million cats and 69 million dogs. Furthermore, pet ownership recently increased in other nations in the region, including Canada and Mexico. According to Pet Keen, published in May 2022, a projected 38% of Canadian homes own a cat, and 35% own a dog. As a result, pet adoption and ownership in the region are projected to increase the prevalence of parasite infection as these animals are more susceptible to becoming infected with parasites. Furthermore, the source above indicated that pet owners in Canada are spending more money on their pets than ever before, with 17% prepared to spend more than USD 500 per year on pet healthcare. As a result, pets are more prone to become infected with parasites, and higher expenditure on animals may increase spending on parasite treatment, boosting the market's growth.

The major players are actively making strategic planning and new developments such as product launches, mergers, acquisitions, and partnerships to contribute to the market's growth. For instance, in June 2022, Zoetis Inc. reported the agreement to acquire Basepaws, a privately held petcare genetics company. The acquisition will advance Zoetis' portfolio in the precision animal health space and inform and shape its future pipeline of petcare innovations in dermatology and parasiticides. Therefore, the factors above are attributed to the market for veterinary parasiticides in North America and are anticipated to witness growth over the forecast period.

Animal Parasiticides Industry Overview

The veterinary parasiticides market is moderately competitive, with several players. Key players in the industry are focusing continuously on expanding their geographic presence using acquiring local market players. Acquisition of animal health assets of local payers by significant market players enabled major market players to increase their presence across various geographic regions and expand their veterinary health product portfolio. Some market players are Elanco Animal Health Incorporated, Boehringer Ingelheim International GmbH, Vetoquinol SA, and Zoetis Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Food Borne and Zoonotic Diseases

- 4.2.2 Growing Adoption of Pet Animals

- 4.2.3 Rising Animal Health Expenditure

- 4.3 Market Restraints

- 4.3.1 Stringent Approval Process for Animal Parasiticides

- 4.3.2 High Cost of Animal Parasiticide Products

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Product Type

- 5.1.1 Ectoparasiticides

- 5.1.2 Endoparasiticides

- 5.1.3 Endectocides

- 5.2 By Animal Type

- 5.2.1 Food-producing Animals

- 5.2.2 Companion Animals

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Bayer AG

- 6.1.2 Boehringer Ingelheim

- 6.1.3 ELI Lilly and Company

- 6.1.4 Merck & Co. Inc.

- 6.1.5 Sanofi

- 6.1.6 Zoetis Inc.

- 6.1.7 Ceva Sante Animale

- 6.1.8 Virbac

- 6.1.9 Perrigo Company PLC

- 6.1.10 Soparfin SCA (Vetoquinol SA)