|

市場調査レポート

商品コード

1444360

獣医診断 - 市場シェア分析、業界動向と統計、成長予測(2024年~2029年)Veterinary Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 獣医診断 - 市場シェア分析、業界動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 117 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

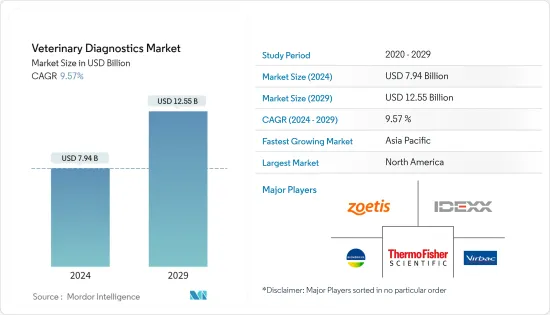

獣医診断市場規模は2024年に79億4,000万米ドルと推定され、2029年までに125億5,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に9.57%のCAGRで成長します。

COVID-19の発生は、政府の規制により獣医診断サービスを含むさまざまなヘルスケアサービスの停止につながったため、獣医診断市場に大きな影響を与えました。たとえば、JAAWSが2022年 2月に発行した記事では、COVID-19により、2020年にカナダと米国の動物病院の70%が閉鎖されたと報告されています。したがって、当初は調査対象市場の成長が妨げられていました。COVID-19感染症を最小限に抑えるため、獣医師の診断サービスを一時停止します。ただし、現在のシナリオでは、獣医診断サービスの再開につながる新型COVID-19症例の減少と、ロックダウン後に報告されたペットの養子縁組の大幅な増加が、予測期間中に調査対象市場の安定した成長につながると予想されます。

調査対象市場の成長を促進する要因は、ペットの養子縁組と動物のヘルスケア費の増加、人獣共通感染症の発生率の増加、開発途上地域における獣医師の数と可処分所得の増加です。たとえば、2022年5月、カナダの2021年農業国勢調査報告書には、カナダの農場が前年(2020年)と比べて豚と豚の頭数が3.4%増加したと報告されたと記載されています。 2021年、カナダには1,460万頭の豚と豚がいた。同様に、APPAが実施した2021年から2022年の全国ペット所有者調査では、米国における犬の定期訪問にかかる年間支出額が猫の178ドルと比較して242ドルであると報告されています。その結果、ペットや家畜の採用の増加と動物のヘルスケア費の増加が、調査対象市場の成長を推進しています。

動物の人獣共通感染症の症例数は近年大幅に増加しています。症例数の増加に伴い、疾患を治療する必要性も大幅に高まっており、獣医学診断市場の成長を促進すると予想されています。例えば、2022年7月にWHOが発表した論文では、アフリカでは、動物に由来し、その後種を変えて人間に感染するサル痘ウイルスなどの人獣共通感染症の病原体による大流行のリスク増大に直面していると報告されています。この10年間で、この地域における人獣共通感染症の発生数は63%増加しました。同情報筋はまた、2022年1月1日から2022年7月8日までに累計2,087件のサル痘症例があり、そのうち確認されたのは203件のみであると報告しました。したがって、動物における人獣共通感染症の増加により、獣医学診断薬の需要が増加しており、それによって研究対象市場の成長が促進されています。

さらに、市場企業による拡大も市場の成長を促進しています。たとえば、2021年 11月、アヴィアジェン・インドはタミル・ナドゥ州にある獣医診断研究所を拡張しました。研究所では、アビアジェンの繁殖ストックの健康状態を定期的に監視しています。したがって、このような拡張により獣医学診断に利用できる施設が増加し、市場の成長に貢献します。

したがって、ペットの養子縁組と動物のヘルスケア費の増加により、人獣共通感染症の発生率の上昇が市場の成長を推進しています。しかし、ペットのケアや画像機器のコストが高いこと、獣医師の不足が獣医学診断市場の成長を妨げています。

獣医診断市場の動向

分子診断セグメントは、予測期間中に大幅な成長を遂げると推定されています。

分子診断セグメントは、家畜やペットの飼い主が迅速な検査結果とその費用対効果を求める傾向が高まっているため、予測期間中に大幅な成長が見込まれると予想されます。この分野の拡大は、猫白血病、犬パルボウイルス、フィラリア、感染性腹膜炎などの流行している動物の病気を特定するために設計された検査数の増加によって促進されると予想されます。さらに、ペットや家畜の飼い主の数の増加と動物の健康への関心の高まり、伴侶動物や家畜の病気の蔓延、自宅で頻繁に検査できる手頃な価格の免疫測定検査が利用しやすくなったことも寄与しています。

家畜における鳥インフルエンザの症例の増加により、分子診断検査の需要が増加しており、それによってこの分野の成長が促進されています。たとえば、2022年4月にカナダ政府が発表した報告書によると、2022年3月にはさまざまな鳥類、トルコ、アヒル/ニワトリ、ガチョウ、クジャクが鳥インフルエンザに感染しました。この病気はすべての人に急速に広がりました。したがって、家畜種を検出するための分子診断検査が増加し、それによってこの部門の成長に貢献します。

同様に、2021年7月、欧州ペットフード連盟は、2020年3月から2021年3月までに、英国で約320万匹のペットを引き取った家族がいると推定されると報告しました。このように、欧州の家庭におけるペットの養子縁組数の多さにより、ペットの飼い主の間でペット動物の健康に対する意識が高まっており、それが獣医学的診断の需要を増大させており、それによってこの分野の成長に貢献しています。

市場企業による機器やその他の製品の発売により、市場の成長が促進されています。たとえば、2021年 8月、HORIBA UK Limitedは、POCKIT Central向けにいくつかの新しい病原体PCR検査を開始しました。これは、あらゆる獣医研究室で迅速かつ正確なPCR検査を可能にする社内の獣医PCR分析装置です。このような発売も市場セグメントの成長を推進しています。

さらに、2022年 1月に、RingbioはFlexy Pet Rapid Testを販売するために、petrapidtest.comという名前の専門Webサイトを立ち上げました。これらのキットは、伴侶動物の病気を検出するためのラテラルフローイムノアッセイ、ELISA、およびリアルタイムPCRに基づいており、ペットの飼い主や動物病院にとって役立ちます。これらの製品のうち、リアルタイムPCRは小規模動物病院向けに特別に設計されており、ウイルス、マイコプラズマ、寄生虫の感染を確認できます。企業が講じたこのようなマーケティング戦略も、このセグメントの成長を促進します。

したがって、家畜における鳥インフルエンザの症例の増加、ペットの採用の増加、新製品の発売により、このセグメントは上記の要因により、予測期間中に大幅な成長を示すと予想されます。

北米は、予測期間中に大幅な成長を遂げると予想されます。

北米地域は、米国、カナダ、メキシコの3か国で構成されます。調査対象の市場は、ペットや家畜の採用の増加、より優れた診断施設の利用可能性、主要な市場企業の存在による技術開発により、この地域で大幅な成長が見込まれると予想されます。

家畜の養子縁組の増加傾向も、この地域の市場の成長を推進しています。たとえば、2022年3月、農務省は2021年にメキシコの牛輸入量が大幅に増加したと報告しました。同情報筋はまた、2021年のメキシコの畜産セクターの成長率が5.4%であると報告しました。したがって、メキシコにおける家畜数の増加により獣医学的疾患のリスクが増大し、国内の獣医学診断薬の需要が増加しており、それによって研究対象の動物の成長を促進しています。市場。

さらに、獣医師の数の増加も調査対象市場の成長を促進しています。たとえば、2022年 9月、米国労働統計局は、獣医師の雇用が2021年から2031年にかけて19%増加すると予測されており、これは全職業の平均よりもはるかに速い速度であると報告しました。また、同情報筋は、10年間で平均して毎年約4,800人の獣医師の求人が見込まれていると報告しました。したがって、獣医師の数の増加は獣医学診断サービスの増加につながり、それによって調査対象市場の成長を促進します。

予防診断ツールの開発も、獣医師の診察と予防ケアの増加に貢献しています。たとえば、2021年4月、Mars Veterinary Healthの一部であるAntech Diagnosticsは、73万件の獣医受診の遡及調査から得たすべての猫が、レナルテックの陽性または陰性後に改善された予防ケアを受けていたことを示す新しいデータを発表しました。 RenalTechは、猫のCKDが発生する2年前にそれを予測します。データによれば、予測診断ツールにより獣医師の診察が31%も増加したことが示されています。このような研究と予測診断ツールの開発も、この国の市場の成長を推進しています。

市場関係者による診断テストの発売数の増加も市場の成長を推進しています。たとえば、2021年 7月に、Vidium Animal HealthはSpotLight修理を開始しました。犬リンパ腫に対する高精度かつ迅速な分子診断検査です。 Vidioは、シティオブホープの関連会社であるトランスレーショナルゲノミクス調査(TGen)およびEthos Discoveryと共同で開発しました。

したがって、ペットおよび家畜の採用の増加、より優れた診断施設の利用可能性、および技術開発により、北米は予測期間中に大幅な成長を予測すると予想されます。

獣医診断業界の概要

獣医診断市場は競争が激しく、細分化されています。主要な市場企業は、動物の管理、特に気象条件の変化による病気から動物を保護するための診断技術の向上に焦点を当てています。獣医診断サービスを提供する企業には、BioMerieux SA、Heska Corporation、Idexx Laboratories、IDVet、Randox Laboratories Ltd.、Thermo Fisher Scientific Inc.、Virbac Corporation、Zoetis Inc.、BIOCHEK BV、INDICAL Bioscience GmbH、Neogen Corporation、およびBio-株式会社ラッド

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- ペット飼育の普及と動物医療費の増加

- 動物人獣共通感染症の負担増加

- 製薬会社によるペット保険と動物医療への投資の拡大

- 市場抑制要因

- 獣医師不足

- ペットケアと画像機器のコストが高い

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 製品タイプ別

- 機器

- キットと試薬

- ソフトウェアとサービス

- 技術別

- 免疫診断

- 臨床生化学

- 分子診断学

- 血液学

- その他の技術

- 動物タイプ別

- コンパニオンアニマル

- 犬

- 猫

- その他のコンパニオンアニマル

- 家畜

- 牛

- 豚

- 家禽

- その他の家畜

- コンパニオンアニマル

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- BioMerieux SA

- Heska Corporation

- Idexx Laboratories

- IDVet

- Randox Laboratories Ltd.

- Thermo Fisher Scientific Inc.

- Virbac Corporation

- Zoetis Inc.

- BIOCHEK BV

- INDICAL Bioscience GmbH

- Neogen Corporation

- Bio-Rad Inc.

第7章 市場機会と将来の動向

The Veterinary Diagnostics Market size is estimated at USD 7.94 billion in 2024, and is expected to reach USD 12.55 billion by 2029, growing at a CAGR of 9.57% during the forecast period (2024-2029).

The outbreak of COVID-19 has had a substantial impact on the veterinary diagnostics market because government regulations led to the suspension of various healthcare services, including veterinary diagnostics services. For instance, an article published by the JAAWS, in February 2022 reported that COVID-19 led to the shutting down of 70% of veterinary clinics in Canada and the US in 2020. Thus, initially, the studied market's growth was hampered due to the suspension of veterinary diagnostic services to minimize the COVID-19 infection. However, in the current scenario, it is anticipated that the decreasing COVID-19 cases leading to the resumption of veterinary diagnostic services and a significant increase in pet adoption reported after the lockdown will lead to the stable growth of the studied market over the forecast period.

The factors driving the growth of the studied market are the increased pet adoption and animal healthcare expenditure, rising incidence of zoonotic diseases, and the growing number of veterinary practitioners and disposable income in developing regions. For instance, in May 2022, Canada's 2021 Census of Agriculture report stated that farms in Canada reported a 3.4% increase in the number of hogs and pigs from the previous year (2020). In 2021, there were 14.6 million hogs and pigs in Canada. Similarly, the National Pet Owners Survey 2021-2022, conducted by the APPA, reported that the annual expenditure on routine visits for dogs accounts for USD 242 compared to USD 178 for cats in the United States. As a result, the increased pet and livestock adoption coupled with increasing animal healthcare expenditure are driving the growth of the studied market.

The number of zoonotic disease cases in animals has risen significantly in recent years. With the rise in the number of cases, the necessity to treat the disorders has also risen extensively, which is expected to propel the growth of the veterinary diagnostic market. For instance, an article published by WHO in July 2022, reported that Africa is facing a growing risk of outbreaks caused by zoonotic pathogens, such as the monkeypox virus which originated in animals and then switched species and infected humans. There has been a 63% increase in the number of zoonotic outbreaks in the region in the decade. The same source also reported that from 1 January 2022 to 8 July 2022 there have been 2,087 cumulative monkeypox cases, of which only 203 were confirmed. Thus, the increase in zoonotic diseases in animals is increasing the demand for veterinary diagnostics, thereby driving the growth of the studied market.

Furthermore, the expansion by the market players is also boosting the market's growth. For instance, in November 2021, Aviagen India expanded its veterinary diagnostic laboratory in Tamil Nadu. The laboratory monitors the health of the Aviagen breeding stock regularly. Thus, such expansion increases the facility available for veterinary diagnosis and contributes to the market's growth.

Thus, due to the increased pet adoption and animal healthcare expenditure, rising incidence of zoonotic diseases, are driving the growth of the market. However, the high cost of pet care and imaging devices and the lack of veterinarians are impeding the veterinary diagnostics market growth.

Veterinary Diagnostics Market Trends

The Molecular Diagnostics Segment is Estimated to Witness Significant Growth Over the Forecast Period.

The molecular diagnostics segment is expected to witness significant growth over the forecast period due to livestock and pet owners growing preference for quick test results and their cost-effectiveness. The segmental expansion is anticipated to be driven by the rising number of tests designed to identify prevalent animal diseases such as feline leukemia, canine parvovirus, heartworm, and infectious peritonitis. Furthermore, the increasing number of pet and livestock owners and the growing concern for their animal health, the rise in the prevalence of companion animal and livestock animal diseases, and the accessibility of affordable immunoassay tests that allow for frequent testing at home are also contributing to the growth of this segment.

The increasing cases of avian influenza in livestock animals are increasing the demand for molecular diagnostic tests, thereby driving the growth of this segment. For instance, in April 2022, as per the report published by the Government of Canada in April 2022, various avian species, turkeys, ducks/chickens, geese, and peafowls were infected by avian influenza in March 2022. The disease spreads rapidly among all livestock species, thus increasing molecular diagnostic tests for its detection, thereby contributing to the segment's growth.

Similarly, in July 2021, European Pet Food Federation reported that between March 2020 and March 2021, it was estimated families adopted around 3.2 million pets in Britain. Thus, the high number of pet adoption in European families is increasing awareness among pet owners about the health of pet animals, which is increasing the demand for veterinary diagnostics, thereby contributing to the growth of this segment.

The market players' launch of instruments and other products is augmenting the market's growth. For instance, in August 2021, HORIBA UK Limited launched several new pathogen PCR tests for its POCKIT Central. It is an in-house veterinary PCR analyzer with the potential for fast, accurate PCR testing in every veterinary lab. Such launches are also propelling the growth of the market segment.

Furthermore, in January 2022, Ringbio launched a professional website names petrapidtest.com to market Flexy Pet Rapid Test. These kits are based on lateral flow immunoassay, ELISA, and real-time PCR to detect companion animal diseases, which can be helpful for pet owners and vet clinics. Among these products, real-time PCR is specially designed for small vet clinics and can confirm infection of viruses, mycoplasma, and parasite. Such marketing initiatives taken by the players also augment the segment's growth.

Thus, with the increasing cases of avian influenza in livestock animals, increased pet adoption, and new product launches, the segment is expected to show significant growth over the forecast period due to the abovementioned factors.

North America is Expected to Witness a Significant Growth Over the Forecast Period.

The North American region comprises of following three countries United States, Canada, and Mexico. The studied market is expected to witness significant growth in the region due to the increasing adoption of pet and livestock animals, availability of better diagnostics facilities, and technological developments due to the presence of key market players.

The increasing trend for livestock adoption also propels the market's growth in the region. For instance, in March 2022, USDA reported that in the year 2021, Mexico's cattle imports considerably increased. The source also reported that 5.4% growth in Mexico's livestock farming sector in 2021. Thus, the increasing livestock number in Mexico is increasing the risk of veterinary diseases which is increasing the demand for veterinary diagnostics in the country, thereby driving the growth of the studied market.

Moreover, the growing number of veterinary practitioners is also driving the growth of the studied market. For instance, in September 2022, the US Bureau of Labor Statistics reported that employment of veterinarians is projected to grow 19% from 2021 to 2031, much faster than the average for all occupations. Also, the same source reported that about 4,800 openings for veterinarians are projected each year, on average, over the decade. Thus, the increasing number of veterinary practitioners is leading to increasing veterinary diagnostic services, thereby driving the growth of the studied market.

The development of preventive diagnostic tools also contributes to the increasing number of veterinary visits and preventive care. For instance, in April 2021, Antech Diagnostics, a part of Mars Veterinary Health, released new data that shows that all cats from a retrospective review of 730,000 veterinary visits received improved preventive care following a positive or negative RenalTech. RenalTech predicts CKD in cats two years before it occurs. The data shows that the predictive diagnostic tool increased veterinary visits by as much as 31%. Such studies and the development of predictive diagnostics tools are also driving the market growth in the country.

The increasing number of launches of diagnostic tests by the market players is also propelling the market's growth. For instance, in July 2021, Vidium Animal Health launched SpotLight repair. It is a highly accurate and rapid molecular diagnostic test for canine lymphoma. Vidio developed it in collaboration with the Translational Genomics Research Institute (TGen), an affiliate of the City of Hope, and Ethos Discovery.

Thus, due to the increasing adoption of pet and livestock animals, availability of better diagnostics facilities, and technological developments, North America is expected to project significant growth over the forecast period.

Veterinary Diagnostics Industry Overview

The veterinary diagnostics market is competitive and fragmented. The major market players are focusing on improved diagnostics techniques for animal care, especially protecting animals from diseases due to changing weather conditions. Some companies that provide veterinary diagnostic services are BioMerieux SA, Heska Corporation, Idexx Laboratories, IDVet, Randox Laboratories Ltd., Thermo Fisher Scientific Inc., Virbac Corporation, Zoetis Inc., BIOCHEK BV, INDICAL Bioscience GmbH, Neogen Corporation, and Bio-Rad Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Adoption of Pet Ownership and Animal Health Expenditure

- 4.2.2 Increased Burden of Animal Zonotic Diseases

- 4.2.3 Growing Pet Insurance and Animal Health Investments by Pharmaceutical Companies

- 4.3 Market Restraints

- 4.3.1 Lack of Veterinarians

- 4.3.2 High Cost of Pet Care and Imaging Devices

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Product Type

- 5.1.1 Instruments

- 5.1.2 Kits and Reagents

- 5.1.3 Software and Services

- 5.2 By Technology

- 5.2.1 Immunodiagnostics

- 5.2.2 Clinical Biochemistry

- 5.2.3 Molecular Diagnostics

- 5.2.4 Hematology

- 5.2.5 Other Technologies

- 5.3 By Animal Type

- 5.3.1 Companion Animals

- 5.3.1.1 Dogs

- 5.3.1.2 Cats

- 5.3.1.3 Other Companion Animals

- 5.3.2 Livestock Animals

- 5.3.2.1 Cattle

- 5.3.2.2 Swine

- 5.3.2.3 Poultry

- 5.3.2.4 Other Livestock Animals

- 5.3.1 Companion Animals

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 BioMerieux SA

- 6.1.2 Heska Corporation

- 6.1.3 Idexx Laboratories

- 6.1.4 IDVet

- 6.1.5 Randox Laboratories Ltd.

- 6.1.6 Thermo Fisher Scientific Inc.

- 6.1.7 Virbac Corporation

- 6.1.8 Zoetis Inc.

- 6.1.9 BIOCHEK BV

- 6.1.10 INDICAL Bioscience GmbH

- 6.1.11 Neogen Corporation

- 6.1.12 Bio-Rad Inc.