|

市場調査レポート

商品コード

1687348

反射防止コーティング:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Anti-Reflective Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 反射防止コーティング:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

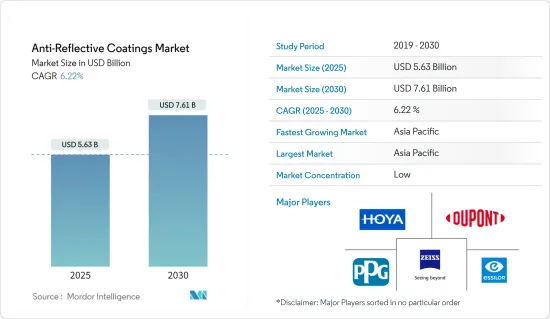

反射防止コーティングの市場規模は2025年に56億3,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは6.22%で、2030年には76億1,000万米ドルに達すると予測されます。

各国が特定の規則や規制を課しているため、COVID-19の流行期にはさまざまな分野の需要が鈍化しました。しかし、2021年には業界が回復し、市場の需要が回復しました。

主なハイライト

- 短期的には、眼鏡用途の需要増と太陽光発電産業からの需要増が市場の成長を押し上げると見込まれます。

- 加えて、反射防止コーティングのコスト高と厳しい環境規制が市場成長の妨げになると予想されます。

- しかし、薄膜製造技術の開発は、市場に有利な成長機会をもたらすと思われます。

- アジア太平洋は、反射防止コーティング市場を独占し、予測期間中に最も急成長する市場となる見込みです。

反射防止コーティング市場の動向

眼鏡用途の需要が増加

- 反射防止メガネは、コンピューターの画面、テレビ、フラットパネルなど、さまざまな電子ディスプレイからのまぶしさを軽減するための手頃な解決策を提供します。

- これらのコーティングは、まぶしさを軽減し、ディスプレイの読みやすさを高め、眼精疲労を軽減し、視覚の明瞭さを向上させます。

- 米国保健福祉省によると、近視は米国の40歳以上の人口の約23.9%(約3,400万人)に影響を及ぼしています。

- 世界保健機関(WHO)によると、2023年8月現在、世界で約22億人が近視または遠視の障害を持っています。さらに、視力障害に伴う生産性低下の世界的コストは4,110億米ドルと推定されています。

- Vision Councilは、米国の眼鏡市場は2023年に656億米ドルと評価され、その重要性をさらに強調しています。同国は約44,850の実店舗を誇り、米国の成人の93%が何らかのアイウェアを常用しています。

- このため、これらの障害に対応しながら、それぞれのアイレンズの需要が高まり、同国における反射防止コーティングの需要がさらに高まると予想されます。

中国がアジア太平洋地域を支配する見込み

- アジア太平洋地域は、半導体、電子機器、ソーラーパネル、その他の製造業務に対する需要の増加により、世界市場を独占しています。中国の太陽電池産業は活況を呈していますが、過剰生産能力と貿易摩擦の激化に悩まされています。欧米諸国は供給過剰の可能性を恐れ、輸出を制限するよう北京に圧力をかけています。国家エネルギー局(NEA)のデータによると、2023年、中国は他のどの国よりも多くのソーラーパネルを設置しました。この実績は、世界の再生可能エネルギーの状況において、すでに主導的な地位を確立していた中国をさらに強化するものです。驚くべきことに、中国は2023年に216.9ギガワットの太陽光発電を追加し、2022年に記録した87.4ギガワットを上回りました。

- また、2024年第1四半期の時点で、中国はソーラーパネル設置の勢いを維持していますが、2023年に見られた154%の急増に比べると鈍化しています。2024年3月、中国の太陽光発電の累積容量は660ギガワットに達し、NEAが報告した2023年末までの米国の179ギガワットとは対照的です。

- 中国は、スマートフォン、テレビ、電線、ケーブル、ポータブルコンピューティングデバイス、ゲームシステム、その他の個人用電子機器などの電子機器製品を含む、世界最大の電子機器生産拠点を有しており、エレクトロニクス分野で最高の成長を記録しました。同国は電子機器の国内需要に応えるとともに、電子機器製品を他国に輸出しています。

- 2023年、中国の半導体産業は力強い成長を遂げ、集積回路(IC)の総生産量は3,514億個に達し、前年比6.9%増を記録しました(工業情報化省による)。

- さらに、半導体産業協会は、半導体製造における中国の躍進を強調しています。予測によれば、2024年には中国の世界半導体生産能力シェアは13%急増し、月産ウエハー860万枚に達する可能性があります。

- このように、上記の要因により、中国はアジア太平洋市場における優位性を維持する態勢を整えています。

反射防止コーティング産業概要

反射防止コーティング市場は、DuPont、PPG Industries Inc.、Hoya Vision Care Company、Zeiss International、Essilor(順不同)などの主要企業によって断片化されています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 眼鏡用途からの需要増加

- 太陽光発電産業からの需要増加

- その他

- 抑制要因

- 反射防止コーティングのコスト高

- 厳しい環境規制

- その他

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- 成膜方法別

- 化学蒸着法

- 電子ビーム蒸着法

- スパッタリング法

- その他

- 用途別

- 半導体

- 電子デバイス

- 眼鏡

- ソーラーパネル

- 車載ディスプレイ

- その他

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- マレーシア

- タイ

- インドネシア

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- カタール

- アラブ首長国連邦

- ナイジェリア

- エジプト

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル(概要、財務、製品・サービス、最近の動向)

- AccuCoat Inc.

- AGC Inc.

- Beneq

- DuPont

- Edmund Optics Inc.

- EKSMA Optics UAB

- ESSILOR OF AMERICA INC.

- Honeywell International Inc.

- HOYA

- Majestic Optical Coatings LLC

- Optical Coatings Japan

- Optics Balzers AG

- Optimum RX Group

- PPG Industries Inc.

- Spectrum Direct

- Torr Scientific Ltd

- ZEISS

- Zygo

第7章 市場機会と今後の動向

- 薄膜製造技術の開発

- その他の機会

The Anti-Reflective Coatings Market size is estimated at USD 5.63 billion in 2025, and is expected to reach USD 7.61 billion by 2030, at a CAGR of 6.22% during the forecast period (2025-2030).

Due to specific rules and regulations imposed by countries, the demand in various sectors slowed during the COVID-19 pandemic. However, the industry recovered in 2021, rebounding the demand in the market.

Key Highlights

- Over the short term, the increasing demand for eyewear applications and rising demand from the solar power generation industry are expected to boost the market's growth.

- Additionally, the high cost of anti-reflective coatings and stringent environmental regulations are expected to hinder the market's growth.

- However, developing thin-film fabrication technologies will likely create lucrative growth opportunities in the market.

- Asia-Pacific is expected to dominate the anti-reflective coatings market and be the fastest-growing market during the forecast period.

Anti-Reflective Coatings Market Trends

The Demand for Eyewear Applications is Increasing

- Anti-reflective glasses offer an affordable solution to glare from various electronic displays, including computer screens, televisions, and flat panels.

- These coatings reduce glare, enhance display readability, lessen eye strain, and improve visual clarity.

- According to the US Department of Health & Human Services, nearsightedness affects about 23.9% of the United States's population over 40 (about 34 million people).

- According to the World Health Organization (WHO), as of August 2023, around 2.2 billion people worldwide had near or distant vision impairment. Moreover, the global costs of productivity losses associated with vision impairment are estimated to be USD 411 billion.

- The Vision Council highlights that the United States optical market was valued at USD 65.6 billion in 2023, further underlining its significance. The country boasts approximately 44,850 brick-and-mortar optical retail outlets, with a striking 93% of US adults regularly sporting some form of eyewear.

- This is expected to enhance the demand for respective eye lenses while addressing these impairments, further enhancing the demand for anti-reflective coatings in the country.

China is Expected to Dominate the Asia-Pacific Region

- Asia-Pacific has dominated the global market due to the increasing demand for semiconductors, electronics, solar panels, and other manufacturing operations. While China's solar industry is experiencing a boom, it grapples with overcapacity and escalating trade tensions. Western nations are pressuring Beijing to limit exports, fearing a potential oversupply. According to data from the National Energy Administration (NEA), in 2023, China installed more solar panels than any other nation. This achievement bolstered its already leading position in the global renewable energy landscape. In a remarkable display, China added 216.9 gigawatts of solar power in 2023, surpassing its 2022 record of 87.4 gigawatts.

- Also, as of the first quarter of 2024, China maintained its momentum in solar panel installations, albeit slower than the 154% surge seen in 2023. In March 2024, China's cumulative solar capacity reached 660 gigawatts, a stark contrast to the United States' 179 gigawatts by the end of 2023, as reported by the NEA.

- China has the world's largest electronics production base, which includes electronic products, such as smartphones, TVs, wires, cables, portable computing devices, gaming systems, and other personal electronic devices, and recorded the highest growth in the electronics segment. The country serves the domestic demand for electronics and exports electronic output to other countries.

- In 2023, China's semiconductor industry witnessed robust growth, with the total output of integrated circuits (ICs) reaching 351.4 billion pieces, marking a 6.9% increase from the previous year, as per the Ministry of Industry and Information Technology.

- Additionally, the Semiconductor Industry Association highlights China's strides in semiconductor manufacturing. Projections suggest that China's global semiconductor capacity share could surge by 13% in 2024, reaching 8.6 million monthly wafers.

- Thus, due to the above-mentioned factors, China is poised to maintain its dominance in the Asia-Pacific market.

Anti-Reflective Coatings Industry Overview

The anti-reflective coatings market is fragmented due to major players, including DuPont, PPG Industries Inc., Hoya Vision Care Company, Zeiss International, and Essilor (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand from Eyewear Applications

- 4.1.2 Rising Demand from the Solar Power Generation Industry

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 High Cost of Anti-reflective Coatings

- 4.2.2 Stringent Environmental Regulations

- 4.2.3 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 By Deposition Method

- 5.1.1 Chemical Vapor Deposition

- 5.1.2 Electronic Beam Deposition

- 5.1.3 Sputtering

- 5.1.4 Other Deposition Methods

- 5.2 By Application

- 5.2.1 Semiconductors

- 5.2.2 Electronic Devices

- 5.2.3 Eyewear

- 5.2.4 Solar Panels

- 5.2.5 Automotive Displays

- 5.2.6 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles (Overview, Financials, Products and Services, and Recent Developments)

- 6.4.1 AccuCoat Inc.

- 6.4.2 AGC Inc.

- 6.4.3 Beneq

- 6.4.4 DuPont

- 6.4.5 Edmund Optics Inc.

- 6.4.6 EKSMA Optics UAB

- 6.4.7 ESSILOR OF AMERICA INC.

- 6.4.8 Honeywell International Inc.

- 6.4.9 HOYA

- 6.4.10 Majestic Optical Coatings LLC

- 6.4.11 Optical Coatings Japan

- 6.4.12 Optics Balzers AG

- 6.4.13 Optimum RX Group

- 6.4.14 PPG Industries Inc.

- 6.4.15 Spectrum Direct

- 6.4.16 Torr Scientific Ltd

- 6.4.17 ZEISS

- 6.4.18 Zygo

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Development of Thin Film Fabrication Technologies

- 7.2 Other Opportunities