手術台:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)

Surgical Tables - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 115 Pages

- 納期

- 2~3営業日

- 商品コード

- 1851184

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

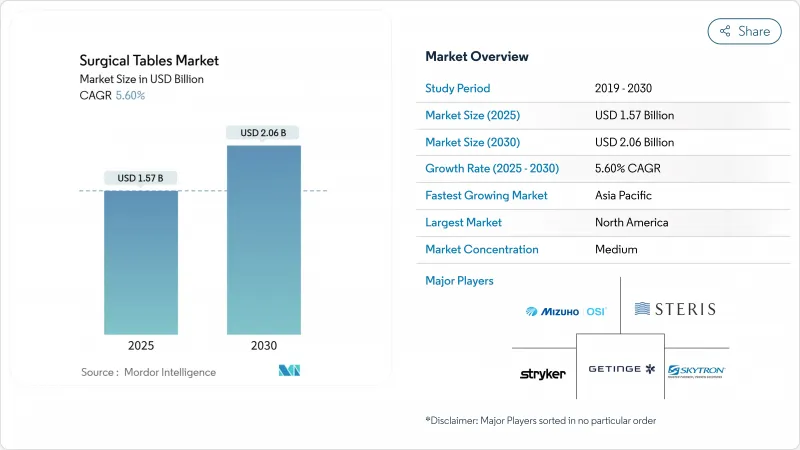

手術台市場は2025年に15億7,000万米ドル、2030年には20億6,000万米ドルに達し、CAGR 5.6%で成長する見込みです。

人口動態の高齢化によって整形外科と心臓血管外科の症例数が増加し、外来患者の治療が外来手術センター(ASC)に移行し、ロボット対応手術室(OR)が患者位置決めプラットフォームの技術水準を引き上げています。病院は、リアルタイムのイメージングをサポートするために、炭素繊維の放射線透過性天板にアップグレードしており、一方、欧米の持続可能性義務化では、エネルギー効率の高いモジュール設計が評価されています。競争戦略は、プロバイダーが調達と統合を簡素化できるように、手術台を画像処理、照明、ロボットに結びつけるバンドルORエコシステムを中心に展開されるようになってきています。プレミアムセグメントのメーカーも、中堅病院の資本予算の制約を緩和するサービスや融資プログラムを開始しています。

世界の手術台市場の動向と洞察

手術件数の増加とASCの拡大

米国の外科手術の大部分は外来で行われており、整形外科や消化器外科の複雑な症例は、病院の外来部門よりも45~60%低いコストで運営され、平均待ち時間が20%短縮されることから、引き続き注目を集めています。ASCの成長により、ベンダーはフットプリントを小さくし、症例間で素早く回転するコンパクトな多専門テーブルを提供するようになりました。資本支出を抑えるため、メーカー各社は現在、特殊な天板に対応したモジュール式のベースを販売しており、センターは、患者数が正当化されるまでアップグレードを延期することができます。グループ購入契約や、機器のサービスとしての資金調達は、導入への障壁をさらに低くしています。

高齢化により整形外科および心臓外科の症例数が増加

人口の高齢化は、関節再建、骨折修復、および正確な位置決めと肥満体重制限を必要とするインターベンショナル心臓外科手術の需要を高めています。米国の整形外科手術件数は年間660万件に達すると予測されており、高荷重リフトと圧迫傷害軽減センサーの必要性が高まっています。XSENSORのForeSite ORのような一体型圧力マッピングを備えた肥満対応テーブルは、手術患者の最大45%に影響する病院内圧傷害を軽減します。

中堅病院におけるプレミアム価格と設備投資の凍結

運営コストの上昇とインフレにより、小規模病院は設備購入を遅らせ、再生機器や複数年リースを選択するようになっています。人工関節全置換術の症例数が増加しているにもかかわらず、メディケアからの償還金が減少しているため、マージンが圧迫され、ハイエンドの画像対応テーブルの正当化が難しくなっています。ベンダーは、施設にベースを設置し、後から接続キットを追加できる段階的アップグレードパスや、メンテナンス、再製造コンプライアンス、ソフトウェアアップデートをバンドルしたサービス契約などで対抗しています。

セグメント分析

2024年の手術台市場シェアは、一般外科が35.78%を占めました。病院は、午前中は盲腸、午後は肥満症例に対応する汎用性の高いクイックスイッチ・プラットフォームを好んでいます。このセグメントの幅広い手技構成は、買い替えのためのスケールメリットをサポートし、そのワークフローは、取り外し可能なアームボードや結石除去用レッグサポートなどの標準化されたアクセサリーと一致しています。一方、ロボットによる胆嚢摘出術の導入により、多くの医療提供者は、手動油圧式ベースから、スピードと一貫性のためにフットスイッチメモリープロファイルを特徴とする電動コラムシステムへの置き換えを進めています。

整形外科と外傷の手術は、2030年までのCAGRが6.78%となり、この市場で最速となります。Zimmer Biomet社のTMINI Miniature Robotic Systemのような膝・股関節ロボットは、フライス加工中にミリ以下の精度を維持する剛性の高い低振動サーフェスに依存しています。テーブルメーカーは、大腿骨遠位部を再ポジショニングすることなく露出させ、麻酔時間とX線被曝を短縮する、長手方向のスライドとチルトレンジで対応しています。脳神経外科と心臓血管の専門分野ではシェアは小さいが、カーボントップ、360°のCアームクリアランス、ナビゲーションシステムと統合する頭部固定インターフェースを要求するため、割高な価格設定となっています。病院が分野横断的なハイブリッド・ルームを追求するにつれて、需要は同じシャーシで脊椎、血管、頭蓋のワークフローをサポートし、在庫とサービスのオーバーヘッドを削減するユニバーサル・プラットフォームへとシフトしています。

地域分析

北米は2024年の売上高の38.75%を占め、高い手術件数と先進ロボットの早期導入に支えられています。米国のASC市場だけでも、2028年までに売上高が590億米ドル近くに達する可能性があり、コスト最適化された回転の速いテーブルの注文に拍車をかけています。メディケアによる部位にとらわれない償還の推進は、病院からASCへの機器の移行をさらに加速させ、GetingeとSTERISの地域サービスネットワークはダウンタイムを短縮し、ブランドへのこだわりを強化します。

欧州は、持続可能性と規制の厳しさが購買を形成する、成熟した買い替え主導型市場を形成しています。ASHRAE 189.3ガイドラインは入札スコアに影響し、エネルギー効率の高いモータードライブやリサイクル可能なパッケージングを購入者に促しています。ゲティンゲの外科用ワークフロー部門は、2023年第4四半期に15.6%の増収を達成しました。グリーンな公共調達基準に関連した資本助成金は、手術件数の伸びは横ばいであるにもかかわらず、安定した需要を維持する可能性が高いです。

アジア太平洋地域は最も急成長している地域で、CAGRは6.84%と予測されます。中国、インド、ASEAN諸国では、ヘルスケア・インフラ投資と医療ツーリズムの拡大がハイブリッドルームの導入を促進しています。シンガポールにあるメドトロニックのロボティクス・エクスペリエンス・スタジオは、トレーニングハブが地域全体に先進的な手術室技術の普及を加速させることを示しています。ベンチャー企業の資金調達は過去2年間で22%減少したが、ベトナムと韓国における国内製造イニシアティブは、輸入関税と供給のボトルネックを相殺し、現地化されたテーブル生産を支援するのに役立っています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 手術件数の増加とASCの拡大

- 高齢化により整形外科と心臓外科の症例数が増加

- 統合OR&ロボット対応テーブルのアップグレード

- 術中イメージングを可能にする炭素繊維製放射線透過性トップ

- 高度な患者ポジショニング機能を必要とする低侵襲手術とロボット手術の急増

- 病院の持続可能性義務化により、エネルギー効率の高いモジュール式テーブルプラットフォームが好まれる

- 市場抑制要因

- 中堅病院におけるプレミアム価格と設備投資の凍結

- 高度なテーブルのための熟練したOR技師の不足

- 炭素繊維サプライチェーンの変動性

- 再処理と規制遵守の厳格化により、医療提供者の生涯所有コストが上昇

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 手術タイプ別

- 一般外科

- 整形外科&外傷

- 循環器

- 脳神経外科

- その他

- 材料別

- 金属

- 炭素繊維複合材料

- エンドユーザー別

- 病院

- 外来手術センター

- 専門クリニック

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 中東

- GCC

- 南アフリカ

- その他中東

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 市場シェア分析

- 企業プロファイル

- Getinge AB

- Stryker Corporation

- Steris plc

- Trumpf Medical(Baxter/Hill-Rom)

- Mizuho OSI

- Skytron LLC

- Schaerer Medical AG

- Merivaara Corp.

- Alvo Medical

- LINET Group SE

- Mindray Medical Intl.

- Opt SurgiSystems Srl

- Eschmann Holdings Ltd

- Allengers Medical Systems

- Nuvo Inc.

- AGA Sanitatsartikel GmbH

- Meditek Canada

- Staan Bio-Med Engg. Pvt Ltd

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 115 Pages

- 納期

- 2~3営業日