|

市場調査レポート

商品コード

1851882

ポイントオブケア分子診断:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Point-of-Care Molecular Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ポイントオブケア分子診断:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月02日

発行: Mordor Intelligence

ページ情報: 英文 131 Pages

納期: 2~3営業日

|

概要

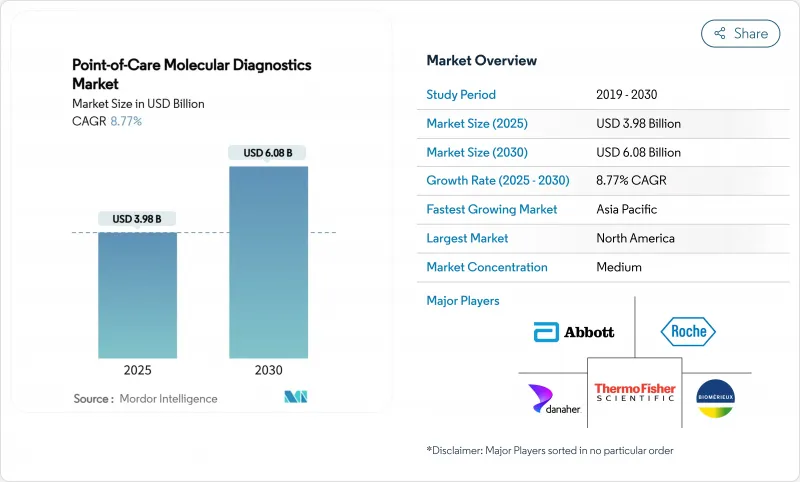

POC分子診断市場は、2025年に39億8,000万米ドル、2030年には60億8,000万米ドルに達すると予測され、2025-2030年のCAGRは8.77%です。

この堅調な成長軌道は、中央集中型の検査室から、ポリメラーゼ連鎖反応グレードの感度をベッドサイドで30分以内に提供するコンパクトなプラットフォームへの業界全体の移行を強調しています。成長の原動力には、呼吸器、消化器、性感染症、腫瘍の検査メニューの拡大、診断回復力への強力な公共投資、臨床医が結果をほぼ瞬時に検索、解釈、保存できるクラウドベースのデータ管理の迅速な統合などがあります。

一方、アジア太平洋地域は、中国とインドが抗菌薬スチュワードシップと高精度腫瘍学をサポートするための分散型検査に投資していることから、ボリュームエンジンとして台頭しつつあります。既存企業はサーマルサイクラーを小型化し、新規参入企業は温度サイクルを省略した等温システムを商品化し、両グループは散在する機器を統合診断ネットワークに結びつけるソフトウェアダッシュボードを展開するため、競合は激化しています。それでも、償還の曖昧さ、検査室が開発した検査の規制遵守にかかるコストの上昇、試薬流通のためのコールドチェーンインフラストラクチャのギャップなどが、特定の環境、特に熱帯地域や資源に乏しい地域など、最も恩恵を受ける可能性のある地域での普及を遅らせる恐れがあります。

世界のポイントオブケア分子診断市場動向と洞察

分散型で迅速な呼吸器感染症検査への需要の高まり

20分未満の呼吸器パネルが臨床的に広く採用されたことで、救急部の待ち時間が短縮され、経験的薬剤の使用が減り、不必要な入院が制限されました。医療システムの報告によると、ポイント・オブ・ケアの分子検査結果は、大半の診察において治療計画を変更し、抗菌薬スチュワードシップを向上させ、入院期間を短縮しています。接続モジュールは、HL7またはFHIRを使用して電子カルテにデータをプッシュし、感染制御チームに、以前は数時間後に到着していたデータをほぼリアルタイムで可視化します。これらの明確な運用上の利点は、インフルエンザやコロナウィルスの季節に大量のカートリッジを供給する原動力となり、その結果、POC分子診断市場のメーカーにとって安定した経常収益を確保することになります。

POC分子診断導入に対する政府とプログラムによる支援

National Institutes of Health Point-of-Care Technologies Research Networkは、2024年に6つの的を絞った資金募集を開始し、腫瘍学、感染症、慢性疾患モニタリングにおけるプロトタイプ開発を加速させる。米国食品医薬品局は、2024年6月に最初のポイントオブケアC型肝炎RNAの認可を与え、慢性的に感染している数百万人の米国人に対する即日診断と治療を可能にします。欧州や日本における同様の構想は、将来のアウトブレイクに対する医療システムの備えを強化するため、プラットフォームの展開に複数年の予算を割り当てています。予測可能な公的セクターの支援は、一時的な需要曲線ではなく構造的な需要曲線を示すものであり、POC分子診断市場で競合する企業の資本計画を改善するものです。

細分化された不透明な診療報酬体系

中央検査室向けに設計されたコーディングフレームワークは、必ずしもニアペイシェントプラットフォームに適用されるとは限らず、プロバイダーは支払率について確信が持てないです。2024年にFDAが決定した検査室が開発した検査の施行裁量権の段階的廃止は、ベンダーが公平な払い戻しを求めて支払者に働きかける一方で、新たなコンプライアンスと文書化のコストを課すことになります。腫瘍学および多発性がんの早期発見パネルは、規制当局の認可が下りるまでに適用範囲の決定が遅れ、臨床的有用性が明らかであるにもかかわらず、その普及が遅れているため、さらに大きな不確実性に直面しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 分散型で迅速な呼吸器感染症検査の需要増加

- POC分子診断導入のための政府とプログラムによる支援

- 新たな応用を可能にする技術の進歩(例:オンコロジー、抗菌スチュワードシップ)

- POC MDxの非従来型セッティング(例:医院、小売薬局)への拡大

- 米国の医院におけるCLIA免除マルチプレックスPCRプラットフォームの採用状況

- マイクロ流体カートリッジの革新がアジアにおけるオンコロジー遺伝子パネルを促進する

- 市場抑制要因

- 細分化され不透明な保険償還状況

- 高い規制と移行コスト

- 熱帯低所得地域における凍結乾燥試薬のコールドチェーン・ギャップ

- アイソサーマルNAATの偽陽性による臨床医の懐疑心

- 規制の見通し

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品・サービス別

- アッセイ&キット

- 計器/分析装置

- ソフトウェア&デジタルサービス

- 用途別

- 感染症

- 腫瘍学

- 血液学

- 出生前検査および新生児検査

- 内分泌学

- ファーマコゲノミクスとコンパニオンDx

- その他の用途

- 技術別

- PCRベース

- INAAT

- その他のテクノロジー

- エンドユーザー別

- 病院

- ホームケア

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Abbott

- F. Hoffmann-La Roche Ltd

- Danaher

- Thermo Fisher Scientific Inc.

- BioMerieux SA

- Siemens Healthineers AG

- Becton, Dickinson and Company

- Hologic Inc.

- Qiagen N.V.

- QuidelOrtho Corporation

- Visby Medical Inc.

- OraSure Technologies Inc.

- Meridian Bioscience Inc.

- Co-Diagnostics Inc.

- Pfizer Inc.

- T2 Biosystems Inc.

- Genedrive plc

- Binx Health, Inc.