|

市場調査レポート

商品コード

1438563

血液悪性腫瘍治療:世界市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Global Hematologic Malignancies Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 血液悪性腫瘍治療:世界市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 111 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

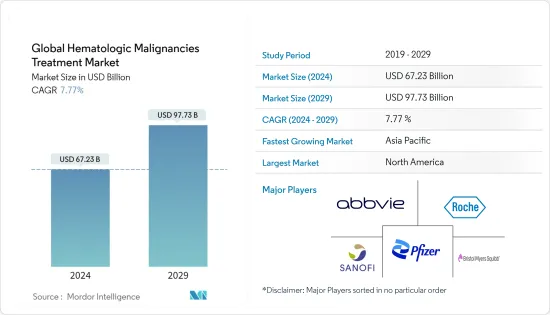

血液悪性腫瘍治療の世界市場規模は2024年に672億3,000万米ドルと推計され、2029年には977億3,000万米ドルに達すると予測され、予測期間中(2024~2029年)のCAGRは7.77%で成長すると予測されます。

COVID-19パンデミックの発生によりほとんどの選択的治療が延期されたため、血液悪性腫瘍治療市場も大きな影響を受けました。しかし、急性白血病をはじめとする重篤な疾患では治療の延期は推奨されないため、パンデミック期間中も万全の防御体制で血液悪性腫瘍の治療を行えるよう、最近では必要なガイドラインや対策が打ち出されています。Acta Haematologica, 2020に掲載された調査論文によると、より集中的でない治療法を採用し、患者とスタッフ間の接触を最小限に抑え、臨床訪問の回数を減らし、経過観察のための遠隔医療を奨励することが、血液悪性腫瘍患者の治療の効果的な結果を助けることができます。United Kingdom Coronavirus Cancer Monitoring Project(UKCCMP)が2020年に実施した調査によると、COVID-19感染の重症化リスクは血液がん患者で約57%と高いことが判明しています。したがって、前述の要因を考慮すると、COVID-19パンデミックは調査市場の成長に影響を与えると予想されます。

血液悪性腫瘍治療市場の成長に寄与する主な要因は、血液がんの新興国市場における罹患率の上昇と、血液悪性腫瘍治療市場を牽引する新たな治療法の開拓に重点が置かれるようになっていることです。Globocan 2020によると、白血病の推定罹患率はアジアが最も高く、2020年に230,650例が診断され、次いで欧州の100,020例、北米の67,784例となっています。このように、世界的に白血病の罹患率が高いことが、市場成長の原動力になると予想されます。

合併、買収、製品上市、提携、共同研究など、主要企業による取り組みが市場成長を後押しすると予想されます。例えば、2021年5月、東京に本社を置く中外製薬は、再発または難治性(R/R)のびまん性大細胞型B細胞リンパ腫(DLBCL)の治療に使用できる抗がん剤/抗微小管結合抗CD79bモノクローナル抗体「ポリビー点滴静注30mgおよび140mg」の発売を発表しました。

2021年2月、米国食品医薬品局は、少なくとも2種類の他の全身治療に反応しなかった特定のタイプの大細胞型B細胞リンパ腫の成人患者を治療するための細胞ベースの遺伝子治療薬であるBreyanzi(lisocabtagene maraleucel)を承認しました。このような製品上市の増加は、研究対象の市場に成長機会をもたらす可能性が高いです。しかし、治療にかかる薬剤費が高いことが市場の主な抑制要因となっています。

血液悪性腫瘍治療市場の動向

化学療法がセグメントをリードし、予測期間中に健全な成長が見込まれる

化学療法は治療の第一選択薬であるため、同市場では化学療法が最大セグメントとなっています。一般的に、ほとんどの種類の血液がんでは化学療法が一般的な治療法であり、がんの種類に応じて特定の薬剤または薬剤の組み合わせが使用されます。大規模な患者プールと血液がんの罹患率の増加が、調査したセグメントの成長の主な促進要因です。また、早期段階での疾患の可能性とその後の治療に対する理解の高まりが、このセグメントの成長を促進すると予想されます。

米国がん学会によると、シタラビン(シトシンアラビノシドまたはアラC)と、ダウノルビシン(ダウノマイシン)またはイダルビシンなどのアントラサイクリン系薬剤は、急性骨髄性白血病の治療に使用される最も一般的な化学療法薬です。クラドリビン(2-CdA)、フルダラビン、ミトキサントロン、エトポシド(VP-16)、6-チオグアニン(6-TG)、ヒドロキシ尿素、プレドニゾンやデキサメタゾンなどの副腎皮質ステロイド薬、メトトレキサート(MTX)、6-メルカプトプリン(6-MP)、アザシチジン、デシタビンなどが急性骨髄性白血病の化学療法に使用されます。また、製品認可の増加は、調査対象市場の成長を助長すると予想されます。例えば、2020年9月、米国FDAは、急性骨髄性白血病の成人患者の治療を継続するために、Bristol Myers Squibb社のアザシチジン(オヌレグ)300mg錠、CC-486を承認しました。同様に、2019年6月、米国食品医薬品局は、少なくとも2回の前治療後に進行または再発したびまん性大細胞型B細胞リンパ腫(DLBCL)の成人患者を治療するために、化学療法薬ベンダムスチンおよびリツキシマブとの併用でポリビーを使用することを承認しました。このように、前述の要因から、研究セグメントは予測期間中に大きな成長を遂げると予想されます。

北米が市場を独占しており、予測期間中も同様と予想される

北米は予測期間を通じて血液悪性腫瘍治療市場全体を支配すると予想されます。主要プレイヤーの存在、血液がん患者の高い有病率、確立されたヘルスケアインフラ、ブランド薬の入手可能性などが、北米における調査市場シェアの大きな要因となっています。

Global Cancer Observatoryによると、2020年には北米地域で67,784例近くの白血病と推定35,318例の多発性骨髄腫が報告されました。白血病リンパ腫協会によると、2021年には、米国で白血病を患っているか寛解状態にある人は、合わせて397,501人と推定されます。また、2021年には米国で約61,090人が白血病と診断される見込みであるとしています。このように、この地域における血液がん患者数の増加は、市場成長の主な促進要因です。

政府の有益な取り組みや研究提携の増加は、市場成長の促進要因として期待されています。例えば、2020年12月、白血病リンパ腫協会(LLS)は、白血病、リンパ腫、骨髄腫、その他の血液がん患者に対する効果的な治療選択肢を見つけるための研究を進展させるために、主要ながん機関や財団と提携を結び、約1,700万米ドルの研究助成金を共同出資する共同研究を開始しました。2020年12月、ジャズ・ファーマシューティカルズは、急性リンパ芽球性白血病(ALL)またはリンパ芽球性リンパ腫(LBL)患者の治療における多剤併用化学療法レジメンの一部として使用するためのJZP-458の生物製剤承認申請(BLA)を提出しました。

多くの企業が市場シェアを拡大するために、製品の上市、提携、共同研究、合併、買収など、さまざまな戦略的取り組みを行っています。例えば、2020年10月、AstraZeneca Pharma India社は、Calquenceのブランド名で様々なタイプの白血病(白血病(CLL)および小リンパ球性リンパ腫)の治療に使用されるアカラブルチニブ100mgカプセルの発売を発表しました。2019年5月、米国食品医薬品局は、慢性リンパ性白血病または小リンパ球性リンパ腫の成人患者を対象としたベネトクラックスの共同開発を行うアッヴィ・インクとジェネンテック・インクを承認しました。以上の発展により、同市場は堅調な成長が見込まれます。

血液悪性腫瘍治療業界の概要

血液悪性腫瘍治療市場は適度に統合されており、複数の大手企業で構成されています。現在市場を独占している企業には、ファイザー、F.ホフマン・ラ・ロシュ、サノフィ、ブリストル・マイヤーズスクイブ、アッヴィ、ノバルティス、グラクソ・スミスクライン、アムジェン、ジョンソン・エンド・ジョンソン、武田薬品工業などがあります。M&Aや新製品開発などの戦略を実施しています。例えば、グラクソ・スミスクラインPLCは2020年8月、再発または難治性の多発性骨髄腫患者に対するファースト・イン・クラスの抗BCMA(B細胞成熟抗原)療法であるBLENREP(belantamab mafodotin-blmf)の米国FDA承認を取得しました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 血液がんの発生率の増加

- 早期診断の可能性に関する意識の高まり

- 新しい治療法の開発に対する注目の高まり

- 市場抑制要因

- 薬価の高騰

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 病態別

- 白血病

- リンパ腫

- 骨髄腫

- 療法別

- 化学療法

- 免疫療法

- 標的療法

- その他の治療法

- エンドユーザー別

- 病院薬局

- 医療機関

- eコマースプラットフォーム

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Pfizer Inc.

- F. Hoffmann-LA Roche Ltd

- Sanofi SA

- Bristol-Myers Squibb Company

- AbbVie Inc.

- Novartis AG

- GlaxoSmithKline PLC

- Amgen Inc.

- Takeda Pharmaceutical Co. Ltd

- Johnson & Johnson

- Incyte Corporation

- AstraZeneca PLC

- Celldex Therapeutics Inc.

- Kite Pharma(Gilead Sciences)

- Atara Biotherapeutics

第7章 市場機会と今後の動向

第8章 COVID-19の市場への影響

The Global Hematologic Malignancies Treatment Market size is estimated at USD 67.23 billion in 2024, and is expected to reach USD 97.73 billion by 2029, growing at a CAGR of 7.77% during the forecast period (2024-2029).

As most elective treatments were deferred due to the outbreak of the COVID-19 pandemic, the hematologic malignancies treatment market was also impacted significantly. However, delayed treatment is not recommended for severe diseases, especially acute leukemia, and thus, necessary guidelines and measures have been put forth recently to allow hematologic malignancies' treatments during the pandemic with all protective measures. According to the research article published in Acta Haematologica, 2020, employing less intensive therapy options, minimizing the exposure between patient and staff, reducing the number of clinical visits, and encouraging telemedicine for follow-up consultations can aid in the effective outcome of treatment of patients with hematologic malignancies. As per the research study carried out by the United Kingdom Coronavirus Cancer Monitoring Project (UKCCMP), 2020, the risk of experiencing severe cases of COVID-19 infection was found to be higher, at about 57%, among patients with blood cancers. Thus, given the aforementioned factors, the COVID-19 pandemic is expected to impact the growth of the studied market.

The major factors attributing to the growth of the hematologic malignancies treatment market are the growing incidence of blood cancer and an increasing emphasis on the development of new treatments, driving the hematologic malignancies treatment market. According to Globocan 2020, the estimated incidence of leukemia was the highest in Asia, with 230,650 cases diagnosed in 2020, followed by 100,020 cases in Europe and 67,784 cases in North America. Thus, the high incidence of leukemia worldwide is expected to drive market growth.

Initiatives by major players such as mergers, acquisitions, product launches, partnerships, and collaborations are expected to boost the market growth. For instance, in May 2021, Tokyo-based Chugai Pharmaceutical Co. Ltd announced the launch of an anticancer agent/antimicrotubule binding anti-CD79b monoclonal antibody called Polivy intravenous infusion 30 mg and 140 mg that can be used for the treatment of relapsed or refractory (R/R) diffuse large B-cell lymphoma (DLBCL).

In February 2021, the United States Food and Drug Administration approved Breyanzi (lisocabtagene maraleucel), a cell-based gene therapy to treat adult patients with certain types of large B-cell lymphoma who have not responded to at least two other types of systemic treatment. Such rising product launches will likely provide growth opportunities to the market studied. However, the high cost of the medication involved in the treatment is the major restraint to the market.

Hematologic Malignancies Treatment Market Trends

Chemotherapy Leads the Segment, and it is Expected to Witness a Healthy Growth Over the Forecast Period

As chemotherapy is the first line of treatment, it is the largest segment in the studied market. Generally, for most types of blood cancers, chemotherapy is the common treatment, and a particular drug or combination of drugs is used depending on the type of cancer. The large patient pool and the increasing incidence of blood cancers are the major drivers for the growth of the studied segment. Also, the growing understanding of the possibility of the disease at the early stage and its subsequent treatment are expected to drive the segment growth.

According to the American Cancer Society, Cytarabine (cytosine arabinoside or ara-C) and anthracycline drugs, such as daunorubicin (daunomycin) or idarubicin, are the most common chemo drugs used in the treatment of acute myeloid leukemia. Cladribine (2-CdA), Fludarabine, Mitoxantrone, Etoposide (VP-16), 6-thioguanine (6-TG), Hydroxyurea, Corticosteroid drugs, such as prednisone or dexamethasone, Methotrexate (MTX), 6-mercaptopurine (6-MP), Azacitidine, and Decitabine are used in chemotherapy of acute myeloid leukemia. Also, the rising product approvals are expected to aid in the growth of the studied market. For instance, in September 2020, the US FDA approved Bristol Myers Squibb's azacytidine (Onureg) 300 mg tablets, CC-486, to continue treating adult patients with acute myeloid leukemia. Similarly, in June 2019, the United States Food and Drug Administration granted approval to Polivy to be used in combination with the chemotherapy drug bendamustine and a rituximab, to treat adult patients with diffuse large B-cell lymphoma (DLBCL) that has progressed or returned after at least two prior therapies. Thus, owing to the aforementioned factors, the studied segment is expected to witness significant growth over the forecast period.

North America Dominates the Market, and it is Expected to do the Same in the Forecast Period

North America is expected to dominate the overall hematologic malignancies treatment market throughout the forecast period. The presence of key players, high prevalence of blood cancer patients, established healthcare infrastructure, and availability of branded drugs are some of the key factors accountable for the large share of the studied market in North America.

According to the Global Cancer Observatory, in 2020, nearly 67,784 cases of leukemia and an estimated 35,318 cases of multiple myeloma were reported in the North American region. According to the Leukemia and Lymphoma Society, in 2021, an estimated combined total of 397,501 people in the United States were living with or in remission from leukemia in the United States. It also stated that around 61,090 people were expected to be diagnosed with leukemia in the United States in 2021. Thus, the increasing number of blood cancer cases in the region is a major driving factor for the growth of the market.

Beneficial government initiatives and an increase in the number of research partnerships are some of the drivers expected to drive market growth. For instance, in December 2020, the Leukemia and Lymphoma Society (LLS) initiated a collaboration to form alliances with leading cancer institutions and foundations to co-fund nearly USD 17 million in research grants to progress the research in finding effective treatment options for patients with leukemia, lymphoma, myeloma, and other blood cancers. In December 2020, Jazz Pharmaceuticals submitted the Biologics License Application (BLA) for its JZP-458 for use as a component of a multiagent chemotherapy regimen in the treatment of patients with acute lymphoblastic leukemia (ALL) or lymphoblastic lymphoma (LBL).

Many companies are undertaking a variety of strategic initiatives like product launches, partnerships, collaborations, mergers, and acquisitions to boost their market share. For instance, in October 2020, AstraZeneca Pharma India announced the launch of Acalabrutinib 100 mg capsules, which are used for the treatment of various types of leukemias (leukemia (CLL) and small lymphocytic lymphoma) under the brand name Calquence. In May 2019, the United States Food and Drug Administration approved AbbVie Inc. and Genentech Inc., jointly developing venetoclax for adult patients with chronic lymphocytic leukemia or small lymphocytic lymphoma. Thus, due to the above-mentioned developments, the market is expected to see robust growth.

Hematologic Malignancies Treatment Industry Overview

The hematologic malignancies treatment market is moderately consolidated and consists of several major players. Some of the companies currently dominating the market include Pfizer Inc., F. Hoffmann-LA Roche Ltd, Sanofi SA, Bristol-Myers Squibb Company, AbbVie Inc., Novartis AG, GlaxoSmithKline PLC, Amgen Inc., Johnson & Johnson, and Takeda Pharmaceutical Co. Ltd. Most of the major players are focusing on expanding their businesses in the developing regions to boost their market shares. They are implementing strategies like mergers and acquisitions and new product developments. For instance, in August 2020, GlaxoSmithKline PLC received US FDA approval for its BLENREP (belantamab mafodotin-blmf), a first-in-class anti-BCMA (B-cell maturation antigen) therapy for the treatment of patients with relapsed or refractory multiple myeloma.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Incidence of Blood Cancer

- 4.2.2 Increasing Awareness about the Possibility of Early Diagnosis

- 4.2.3 Increasing Emphasis on Development of New Treatments

- 4.3 Market Restraints

- 4.3.1 High Cost of Medication

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Disease Condition

- 5.1.1 Leukemia

- 5.1.2 Lymphoma

- 5.1.3 Myeloma

- 5.2 By Therapy

- 5.2.1 Chemotherapy

- 5.2.2 Immunotherapy

- 5.2.3 Targeted Therapy

- 5.2.4 Other Therapies

- 5.3 By End User

- 5.3.1 Hospital Pharmacies

- 5.3.2 Medical Stores

- 5.3.3 E-commerce Platforms

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle-East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle-East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Pfizer Inc.

- 6.1.2 F. Hoffmann-LA Roche Ltd

- 6.1.3 Sanofi SA

- 6.1.4 Bristol-Myers Squibb Company

- 6.1.5 AbbVie Inc.

- 6.1.6 Novartis AG

- 6.1.7 GlaxoSmithKline PLC

- 6.1.8 Amgen Inc.

- 6.1.9 Takeda Pharmaceutical Co. Ltd

- 6.1.10 Johnson & Johnson

- 6.1.11 Incyte Corporation

- 6.1.12 AstraZeneca PLC

- 6.1.13 Celldex Therapeutics Inc.

- 6.1.14 Kite Pharma (Gilead Sciences)

- 6.1.15 Atara Biotherapeutics