|

市場調査レポート

商品コード

1433909

腎臓透析装置市場:世界市場シェア分析、産業動向・統計、成長予測(2024年~2029年)Global Renal Dialysis Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 腎臓透析装置市場:世界市場シェア分析、産業動向・統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

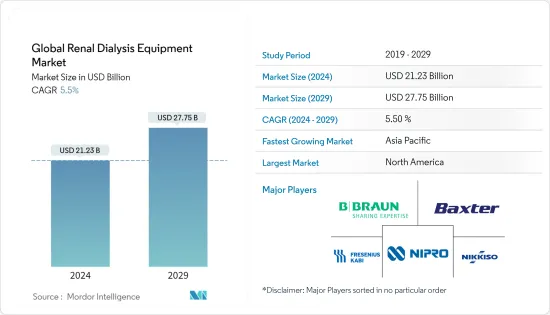

世界の腎臓透析装置市場規模は2024年に212億3,000万米ドルと推定され、2029年までに277億5,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に5.5%のCAGRで成長します。

新型コロナウイルス感染症(COVID-19)のパンデミックはヘルスケア分野に影響を与えました。COVID-19ウイルス感染症のパンデミックの影響を受けた人々は、腎臓病やその他の慢性疾患を発症していることが判明しました。 2022年3月に更新された、COVID-19感染症が腎臓病に及ぼす影響に関するジョンズ・ホプキンス大学の論文によると、新型COVID-19感染症に感染した人の一部には腎臓障害の兆候が見られ、以前に腎臓に問題がなかった人でも感染したといいます。さらに、ニューヨークと中国で入院したCOVID-19症患者の約30%が中等度または重度の腎障害を発症しました。COVID-19患者の血液検査の異常と尿中の高タンパク濃度は腎臓の問題の兆候であり、場合によっては腎臓の損傷や透析の必要性につながった。重篤な症例の場合、患者の回復には6週間以上かかりました。感染者の約1%がこの病気で死亡しました。したがって、COVID-19は調査対象の市場に重大な影響を与えました。

市場の成長を牽引する要因としては、末期腎疾患患者(ESRD)の増加、腹膜透析の需要の増加、費用対効果が高く正確な携帯型透析装置の増加、先端技術などが挙げられます。

先進新興諸国でも、腎疾患などの腎疾患の発生率が増加しています。透析は、末期腎障害(ESRD)または慢性腎臓病の患者に紹介されます。 2021年10月にFrontiers in public Health誌に掲載された「高齢者患者における尿路感染症の横断的評価:有病率、投薬計画の複雑さ、および治療結果に関連する要因」と題した記事によると、外来患者数は約700万人だといいます。 ,尿路感染症による救急外来受診件数は100万件、入院件数は10万件で、毎年高齢者の全感染症の約25%を占めています。

2022年4月にキドニー・インターナショナル・サプリメント誌に掲載された「慢性腎臓病の疫学:最新情報2022年」というタイトルの記事によると、進行性疾患である慢性腎臓病は、これまでに世界中の一般人口の10%以上に影響を及ぼしていると報告されています。 8億人以上の個人に。世界中で腎臓病に罹患している人口が多いため、予測期間中に腎臓透析装置市場の成長がさらに高まる可能性があります。

腎臓透析装置市場は、透析センター数の拡大、新たな透析製品開発のための研究開発費の増加、末期腎疾患の増加により、良好な成長が見込まれています。 2021年11月、フレゼニウス・メディカル・ケアは、5008S血液透析(HD)装置や新しい自動腹膜透析(APD)装置など、末期腎臓病患者が自宅で快適に透析を行えるようにする新しいデジタル化オプションを披露しました。

ただし、透析に関連する合併症やリスク、償還問題などの要因により、予測期間中の市場の成長が妨げられる可能性があります。

腎臓透析装置市場動向

血液透析(HD)機器セグメントは、予測期間中に最も速い成長率を示すと予想される

腎不全患者の有病率の増加により、世界的に血液透析装置の導入は着実に増加しています。血液から老廃物や水分をろ過するために使用されます。したがって、市場プレーヤーは、市場全体の成長に役立つ新しい血液透析装置の開発に焦点を当てていることがわかります。

COVID19は非常に感染力の高い感染症であり、一般集団における予後はさまざまです。血液透析療法を受けている患者は、感染症を発症しやすくなっています。さらに、年齢、高血圧、糖尿病、がん、慢性呼吸器疾患や心臓血管疾患などの危険因子は、最悪の予後と関連しています。たとえば、2021年11月にJournal of Nephrologyに掲載された「長期透析を受けるメディケア患者におけるCOVID-19ウイルス感染症の危険因子と死亡率」と題された記事によると、新型COVID-19感染症に関連した慢性腎不全患者の状態は次のとおりでした。悪いです。新型コロナウイルス感染症(COVID-19)は腎臓に感染し、急性腎障害を引き起こす可能性があります。

また、2021年 1月に国際環境調査および公衆衛生ジャーナルに掲載された「血液透析患者の死亡率に関連するヘモグロビンレベルの変動と要因:78か月の追跡調査」と題された別の記事では、血液透析患者の死亡率に関連するいくつかの危険因子が示されています。ヘモグロビンの変動を含む腎臓病は、病気の重症度に大きな役割を果たしました。このような関連リスク要因により、腎臓透析装置市場の成長がさらに高まる可能性があります。

このセグメントの成長を牽引している要因には、末期腎疾患(ESRD)などの腎臓病の有病率の上昇や、市場関係者による革新的な製品の市場投入の増加などが含まれます。国立糖尿病・消化器・腎臓病研究所(NIDDK)によると、2020年、末期腎疾患(ESRD)としても知られるESKDは米国で約78万6,000人が罹患しており、そのうち71%が透析を必要とし、29人が透析を必要としています。腎臓移植が必要な割合。 ESKDは、女性2人が発症するごとに3人の男性が罹患します。しかし、人口のほとんどは初期段階で診断されず、最終的には世界中で死に至ります。

さらに、ヘルスケアにおける技術の進歩により、人間工学が改善された血液透析機械の開発が行われました。たとえば、2021年 3月、Fresenius Medical Care北米(FMCNA)とDaVita Kidney Careはパートナーシップを拡大し、NxStage家庭用血液透析(HHD)機械、透析用品、コネクテッドヘルスプラットフォームを含む家庭用透析技術を提供しました。したがって、上記の要因が予測期間中にセグメントの成長を促進すると予想されます。

北米は市場で重要なシェアを保持すると予想されており、予測期間にも同様のシェアを獲得すると予想されます。

北米市場の成長を牽引する要因には、腎臓透析部門における新技術の大量採用が含まれます。新型コロナウイルス感染症(COVID-19)のパンデミックの影響を受ける人の数が多いことも、腎臓病の影響を受ける人の数を増やし、市場の成長をさらに加速させました。また、公的ヘルスケア費の急増や、先進的な治療の利用可能性に関する意識向上プログラムも増えています。

2019年新型コロナウイルス感染症(COVID-19)は、高齢者や慢性腎臓病(CKD)などの慢性疾患に苦しむ個人の死亡率が高くなります。 2021年3月に更新された米国疾病管理予防センター(CDC)の2021年の慢性腎臓病に関するデータによると、米国成人の約15%、または約3,700万人が慢性腎臓病(CKD)に苦しんでいます。

2022年1月にJournal of Kidney Medicineに掲載された「2型糖尿病患者と非糖尿病患者のCKD有病率:米国の地域差」と題した論文によると、米国における慢性腎臓病の主な原因は糖尿病だった。国内の糖尿病患者数の増加も慢性腎臓病に罹患する人の増加に寄与し、それによって腎臓透析装置市場の成長に拍車をかけた。

米国市場に関与している市場プレーヤーには、DaVita、Baxter International、Medtronic、米国Renal Careなどがあります。これらの企業は、市場での地位を維持するために、コラボレーション、合併、買収、製品革新などのさまざまな戦略を採用しました。革新的な透析製品とサービスを開発する英国の医療技術パイオニアであるクアンタダイアリシステクノロジーズ社は、2021年 1月に米国食品医薬品局から小型でシンプルな高性能血液透析システムSC+を米国で販売するための510(k)認可を取得しました。州。

したがって、上記の要因は、予測期間中に市場の成長を促進すると予想されます。

腎臓透析装置業界の概要

腎臓透析装置市場は細分化されており、複数の市場プレーヤーが存在し、競争が激しくなっています。一部の市場参加者は、新製品の発売、拡張、契約、合弁事業、パートナーシップ、買収などの戦略を使用して、この市場での拠点を拡大しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 腹膜透析需要の拡大

- 新しい透析製品開発のための研究開発費の伸び

- 腎臓病の有病率の増加

- 市場抑制要因

- 透析に伴う合併症とリスク

- 償還の問題

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 製品タイプ別

- 血液透析(HD)機器

- 腹膜透析(PD)機器

- 濃縮液および溶液

- カテーテルとチューブ

- その他の製品

- 用途別

- 血液透析

- 腹膜透析

- エンドユーザー別

- 施設内透析

- 在宅医療

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Fresenius Kabi AG

- Baxter International, Inc.

- Nipro Corporation

- B. Braun Melsungen AG

- Nikkiso Co. Ltd

- Asahi Kasei Corporation

- Medtronic PLC

- Rockwell Medical

- Teleflex Incorporated

- Medivators Inc

- Toray Medical Co. Ltd

- Hemoclean Co. Ltd

- Medtronic PLC

- Quanta

- Outset Medical Inc.

第7章 市場機会と今後の動向

The Global Renal Dialysis Equipment Market size is estimated at USD 21.23 billion in 2024, and is expected to reach USD 27.75 billion by 2029, growing at a CAGR of 5.5% during the forecast period (2024-2029).

The COVID-19 pandemic had an impact on the healthcare sector. People affected by the COVID-19 pandemic were found to develop kidney diseases and other chronic conditions. According to a Johns Hopkins University article on the impact of COVID-19 on kidney diseases updated in March 2022, some people infected with COVID-19 showed signs of kidney damage, and even those with no prior kidney problems were infected. Furthermore, approximately 30% of COVID-19 patients hospitalized in New York and China developed moderate or severe kidney injury. Atypical blood work and high protein levels in the urine were signs of kidney problems in COVID-19 patients, leading to kidney damage and the need for dialysis in some cases. For severe cases, patient recovery took six weeks or more. About 1% of infected patients died from the disease. Thus, COVID-19 had a profound impact on the market studied.

Some factors driving the market growth include the rise in the number of end-stage renal disease patients (ESRD), growing demand for peritoneal dialysis, rise in cost-effective and accurate portable dialysis apparatus, and advanced technologies.

There has been an increase in the incidence of renal diseases, such as kidney diseases, in developed and developing countries. Dialysis is referred to patients with an end-stage renal disorder (ESRD) or chronic kidney disease. According to an article titled 'A Cross-Sectional Assessment of Urinary Tract Infections Among Geriatric Patients: Prevalence, Medication Regimen Complexity, and Factors Associated With Treatment Outcomes' published in the journal of Frontiers in public Health in October 2021, about 7 million outpatient visits, 1 million emergency outpatient visits, and 100,000 hospitalizations were due to urinary tract infections, accounting for about 25% of all infectious diseases in the elderly each year.

As per the article titled 'Epidemiology of chronic kidney disease: an update 2022' published in the journal of Kidney International Supplements in April 2022, chronic kidney disease, a progressive condition, has affected over 10% of the general population worldwide till date, accounting for more than 800 million individuals. The large volume of the population affected by kidney diseases in the world is likely to add to the growth of the renal dialysis equipment market over the forecast period.

The renal dialysis equipment market is expected to show good growth due to the expanding number of dialysis centers, growth in research and development expenditure for developing new dialysis products, and increasing end-stage renal diseases. In November 2021, Fresenius Medical Care showcased new digitalized options that enable patients with end-stage kidney disease to perform dialysis in the comfort of their own homes, including the 5008S hemodialysis (HD) machine and a new automated peritoneal dialysis (APD) machine.

However, factors such as complications and risks associated with dialysis and reimbursement issues may impede the market growth over the forecast period.

Renal Dialysis Equipment Market Trends

Hemodialysis (HD) Equipment Segment is Expected to Exhibit the Fastest Growth Rate over the Forecast Period

Globally, hemodialysis equipment adoption is steadily increasing due to the increasing prevalence of kidney failure patients. It is used to filter wastes and water from the blood. Thus, market players are found focusing on the developments of the new hemodialysis equipment that help in the growth of the overall market.

COVID19 is a very high transmission infectious disease with a variable prognosis in the general population. Patients in hemodialysis therapy are vulnerable to developing an infectious disease. Moreover, risk factors such as age, hypertension, diabetes, cancer, and chronic respiratory and cardiovascular disease are associated with the worst prognosis. For instance, according to an article titled 'COVID-19 Risk Factors and Mortality Outcomes Among Medicare Patients Receiving Long-term Dialysis' published in the journal of Nephrology in November 2021, the conditions of patients with chronic kidney failure associated with COVID-19 were worse. COVID-19 infects the kidneys and may induce acute kidney injury.

Also, another article titled 'Variability in Hemoglobin Levels and the Factors Associated with Mortality in Hemodialysis Patients: A 78-Month Follow-Up Study' published in the International Journal of Environmental Research and Public Health in January 2021 indicated that several risk factors associated with kidney disease, including the hemoglobin variability, played a major role in the severity of the disease. Such associated risk factors are likely to add to the growth of the renal dialysis equipment market.

Some of the factors which are driving the segment growth include the rising prevalence of kidney diseases such as end-stage renal disease (ESRD), along with increasing innovative product launches in the market by market players. According to the National Institute on Diabetes and Digestive and Kidney Diseases (NIDDK), in 2020, ESKD, also known as an end-stage renal disease (ESRD), affects almost 786,000 people in the United States, with 71% requiring dialysis and 29% requiring a kidney transplant. ESKD affects three men for every two women who develop it. However, most of the population remains undiagnosed in the early stages, eventually leading to death worldwide.

Furthermore, technological advancements in healthcare have led to the development of hemodialysis machines with improved ergonomics. For instance, in March 2021, Fresenius Medical Care North America (FMCNA) and DaVita Kidney Care expanded their partnership to provide home dialysis technology, including NxStage home hemodialysis (HHD) machines, dialysis supplies, and a connected health platform. Thus, the above-mentioned factors are expected to drive segment growth over the forecast period.

North America is Expected to Hold a Significant Share in the Market and is Expected to do the Same in the Forecast Period.

The factors driving the market growth in North America include the massive adoption of new technologies in the kidney dialysis division. The large number of people affected by the COVID-19 pandemic also added to the number of people affected by kidney diseases, which added to the market growth. There is also a boom in public healthcare expenditure and increased awareness programs about the availability of advanced treatments.

The novel coronavirus disease 2019 (COVID-19) has a high mortality rate among older adults and individuals suffering from chronic conditions, such as chronic kidney diseases (CKD). According to the Centers for Disease Control and Prevention (CDC) data on chronic kidney disease in the United States 2021 updated in March 2021, about 15% of adults in the United States or around 37 million people suffer from chronic kidney diseases (CKD).

According to an article titled 'CKD Prevalence Among Patients With and Without Type 2 Diabetes: Regional Differences in the United States' published in the journal of Kidney Medicine in January 2022, diabetes mellitus was the leading cause of chronic kidney disease in the United States. The rising number of diabetic patients in the nation also contributed to the increasing number of people affected by chronic kidney disease, thereby adding to the growth of the renal dialysis equipment market.

Some of the market players involved in the United States market include DaVita, Baxter International, Medtronic, and U.S. Renal Care. These players adopted various strategies, such as collaborations, mergers, acquisitions, and product innovations, to maintain their market position. In January 2021, Quanta Dialysis Technologies Ltd, a British medical technology pioneer developing innovative dialysis products and services, received 510(k) clearance from the United States Food and Drug Administration to market its small and simple, high performance hemodialysis system SC+ in the United States.

Thus, the abovementioned factors are expected to drive market growth over the forecast period.

Renal Dialysis Equipment Industry Overview

The renal dialysis equipment market is fragmented and competitive, with several market players. Some market players have used strategies such as new product launches, expansions, agreements, joint ventures, partnerships, and acquisitions to increase their footprints in this market. Some of the market players include Fresenius Kabi AG, B. Braun Melsungen AG, Baxter International Inc., Nikkiso Co. Ltd, and Nipro Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Peritoneal Dialysis

- 4.2.2 Growth in R&D Expenditure for the Development of New Dialysis Products

- 4.2.3 Increasing Prevalence of Kidney Disease

- 4.3 Market Restraints

- 4.3.1 Complications and Risks Associated with Dialysis

- 4.3.2 Reimbursement Issues

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Product Type

- 5.1.1 Hemodialysis (HD) Equipment

- 5.1.2 Peritoneal Dialysis (PD) Equipment

- 5.1.3 Concentrates and Solutions

- 5.1.4 Catheters and Tubings

- 5.1.5 Other Products

- 5.2 By Application

- 5.2.1 Hemodialysis

- 5.2.2 Peritoneal Dialysis

- 5.3 By End User

- 5.3.1 In-Center Dialysis Settings

- 5.3.2 Home Care Settings

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle-East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle-East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Fresenius Kabi AG

- 6.1.2 Baxter International, Inc.

- 6.1.3 Nipro Corporation

- 6.1.4 B. Braun Melsungen AG

- 6.1.5 Nikkiso Co. Ltd

- 6.1.6 Asahi Kasei Corporation

- 6.1.7 Medtronic PLC

- 6.1.8 Rockwell Medical

- 6.1.9 Teleflex Incorporated

- 6.1.10 Medivators Inc

- 6.1.11 Toray Medical Co. Ltd

- 6.1.12 Hemoclean Co. Ltd

- 6.1.13 Medtronic PLC

- 6.1.14 Quanta

- 6.1.15 Outset Medical Inc.