ZigBee:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

ZigBee - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1642171

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

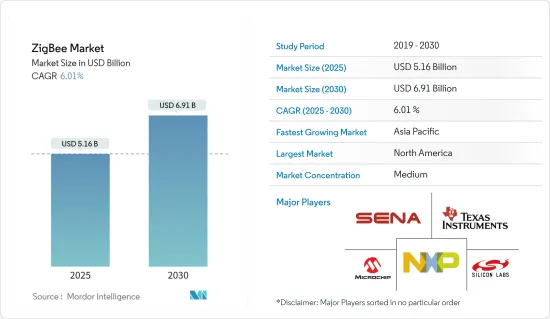

ZigBee市場規模は2025年に51億6,000万米ドル、2030年には69億1,000万米ドルに達すると予測され、予測期間(2025-2030年)のCAGRは6.01%です。

主なハイライト

- 世界のスマートホームデバイス導入の急増により、今後数年間はZigBee対応デバイスの需要が促進されます。スマートホーム市場が急速に拡大する中、ホームネットワークとシームレスに統合するスマート家電や電化製品のニーズが高まっています。ZigBeeプロトコルを利用することで、照明や空調システムから安全装置まで、さまざまな家電製品を遠隔操作することができ、エネルギー効率を高め、電力の浪費を抑えることができます。

- スマートデバイスの普及動向の拡大により、家電分野の成長により、新興国全体でIEEE 802.15.4に基づくデバイスの監視・制御に使用されるZigBeeベースの通信サービスの導入が促進されると予測されます。

- 大幅な進歩に伴い、スマートエネルギー/スマートグリッドやビルディングオートメーションシステムなど、様々な監視・制御アプリケーション向けに、安価なバッテリーで何年も動作可能な低コスト・低消費電力ソリューションを使用したZigBeeワイヤレスネットワークの大規模展開に対する需要の高まりが、市場を牽引すると予想されます。

- スマート・センサ技術の普及と接続の増加、クラウド・コンピューティングの飛躍的な進歩が、産業用IoTの普及と拡大を後押ししています。この動向は、製造ガジェットが短距離で相互作用しなければならない極小の産業環境におけるZigBeeの採用を増加させるとも予測されています。ZigBeeは802.15.4プロトコルをベースにしていますが、セキュリティはZigBee開発者によって効果的に処理されていません。この脆弱性は、802.15.4プロトコルのセキュリティ機能とIoTデバイスへのZigBee無線の実装を調査している多くの情報セキュリティ専門家の興味を刺激しています。

- エリクソンのモビリティレポート2023によると、バッテリ寿命が長く、低~中程度のスループットを持つ低複雑度、低コストのデバイスを大量に含む広域ユースケースをサポートする大規模IoT技術NB-IoTとCat-Mは、世界中で展開され続けています。世界では、128のサービス・プロバイダーがNB-IoTネットワークを展開または商業的に開始し、60がCat-Mを開始し、45が両方の技術を展開しています。セルラーIoTの総接続数は、2023年末には約30億に達すると予測されています。マッシブIoT技術の成長は、ネットワークに追加された機能によって強化され、周波数分割複信(FDD)帯域でスペクトラム共有によってマッシブIoTが4Gや5Gと共存できるようになります。

ZigBee市場動向

住宅オートメーション・セグメントが市場で大きなシェアを占める見込み

- 都市部の人口増加により、利用可能なリソースへの負担が増大するため、リソースのモニタリングが必要となっています。モノのインターネット(IoT)は、スマートデバイスに組み込まれたセンサーからデータを収集できるため、スマートシティ開発を支援するデジタルサービスの基盤として機能します。IoTは、現代の家庭に欠かせないものとなりつつある、多くの連携スマートガジェットを生み出しました。世界銀行は、スマートシティが2025年までに世界のGDPの約60%に貢献すると予想しています。

- スマートビルはまた、スマートグリッドにリンクさせることができ、スマートビルのコンポーネントと電力網が相互作用することを可能にします。この技術により、より効果的なエネルギー配給、事前のメンテナンス、迅速な停電解決が可能になります。コネクテッド・デバイスの使用が増えた結果、ZigBeeが採用され、スマート・ハブの普及を助けています。Amazon Echo、Google Home、Insteon Hub Pro、Samsung SmartThings、Wink Hubなどがスマートホームハブの一例です。

- さらに、IoTプラットフォームの世界的ベンダーであるTuyaは、スマートホームオートメーションハブを提供しています。複数のスマートホームデバイスを可能にするPegasus技術が搭載され、ギガビットルーターとZigBeeゲートウェイが付属します。プラットフォームや技術のベンダーとは別に、家電メーカーもZigBee技術を製品に取り入れています。例えば、照明システムを主要製品とする電子機器製造会社XALは、DALIとともにZigBeeオープン通信規格を提供するようになってきています。

- さらに、モノのインターネット(IoT)は、スマートホームガジェットの重要性の高まりと、利便性とエネルギー効率の両方を目指した自動化に対する消費者の旺盛な意欲に後押しされ、急速に現実のものとなりつつあります。コネクテッド・リビングのコンセプトは、主に住宅居住者のセキュリティを強化する能力から、中心的な役割を担っています。特筆すべきは、技術的な進歩がこうしたスマート・デバイスの普及に拍車をかけていることで、コネクテッド・ホームの枠組みの中で多様な用途が広がっています。

- また、米国国勢調査局によると、米国の住宅戸数は前年比で増加しており、昨年は約1億4,400万戸でした。さらに、2023年8月には米国で約11万4200戸の住宅建設が開始されます。このような住宅建設の増加は、調査対象市場の成長機会を生み出すと期待されています。2024年デジタル・ノマドの現状」によると、2024年3月時点でデジタル・ノマドが最も訪問した都市はロンドンで、世界中のデジタル・ノマドの旅行の約2.3%を占めました。デジタル・ノマドに対するこのような開発が、調査対象市場を牽引すると予想されます。

北米が市場で最も大きなシェアを占める見込み

- 北米は、同地域の多数のエンドユーザー業界関係者による先端技術へのニーズの高まりにより、顕著な市場の1つとなっています。さらに、この地域における高速ネットワーキング技術の進化が、市場の成長を後押ししています。小売業界は、スマートホームのためにドモティクスとオートメーションを取り入れています。照明、エンターテイメントシステム、家電製品、家の気候を制御するホームオートメーションシステムを備えています。例えば、Philips Lighting Holding BVは、居住者がいつ部屋にいるかを確認し、必要に応じて照明を調整できるスマート照明システムHueを提供しています。

- IT・通信部門は、ZigBeeプロトコルを統合したネットワーク・ハードウェアへの意欲の高まりによって、市場を独占する態勢を整えています。サムスンのスマートハブやグーグルのWi-Fiルーターなどの製品に搭載されているシリコンラボのチップは、BLEとZigBee Proをサポートしています。さらに、ZigBeeアライアンスの「All Hubs Initiative」は、エコシステム全体の信頼性、相互運用性、セキュリティを強化することを目的としています。この勢いに加え、D-LinkはZigBee技術を採用した最新ソリューションを発表しました。

- ZigBeeの住宅オートメーション分野は、大きな需要が見込まれています。技術を自社製品に組み込み、他のベンダーと提携するベンダーが増えています。さらに、米国国勢調査局によると、2023年8月に米国で約114,200戸の住宅建設が開始されます。このような大規模な新規居住者の建設は、調査された市場が成長する機会を生み出すと思われます。

- ヘルスケアにおけるIoT利用の増加は、業務の最適化に役立っています。IoTは、遠隔監視などの重要なソリューションを提供します。同分野におけるこれらのソリューションの利用は、より良い患者ケアの提供に役立っています。ソリューションはまた、患者の関与を高めることによって、医師が最高のケアを提供できるようにします。世界各国の政府は、遠隔地にも医療の恩恵が行き届くよう、ヘルスケアへの支出を増やしています。このテクノロジーは、ヘルスケアシステムを効率的に機能させる。例えば、OECDによると、米国政府はGDPの16.9%をヘルスケアに費やしています。

- さらに、ZigBeeの進歩はこの地域での普及を促進すると思われます。例えば、ZigBee 3.0では、ZigBee Cluster Library(ZCL)は利用可能な全てのクラスタを含んでおり、全てのデバイスがクラスタと関連機能を利用できる完全なツールボックスを提供します。ZigBee 3.0ソフトウェアスタックには、ネットワークへのノードのコミッショニングに一貫した動作を提供する「ベースデバイス」が組み込まれています。さらに、ZigBee 3.0は、様々なワイヤレスネットワークの増大するスケールと複雑さをサポートし、250ノード以上の大規模なローカルネットワークに対応します。さらに、ZigBee 3.0は強化されたネットワークセキュリティを提供します。

ZigBee産業概要

ZigBee市場は半固定的で、少数の主要プレイヤーで構成されています。市場シェアでは、数社が業界を支配しています。しかし、通信技術が接続媒体全体で進歩するにつれて、新たな企業が市場での存在感を強め、新興国全体で企業の足跡を広げています。

- 2024年4月NXPセミコンダクターズは、最新のMCX Wシリーズで2つの最先端マルチプロトコル・ワイヤレス・マイクロコントローラ・ユニット(MCU)を発表します。これらのMCUは、Matter、Thread、ZigBee、Bluetooth Low Energy(BLE)など、さまざまなプロトコルに対応しています。MCX W72xは、Bluetoothチャネルサウンディングを特長とする先駆的なワイヤレスMCUです。NXPは、これらの製品を産業用IoTアプリケーション向けに特別にカスタマイズしています。これらの製品は、NXPが最近リリースしたMCX AシリーズとMCX Nシリーズを補完するものです。さらに、これらの製品は、MCXポートフォリオのアーキテクチャ、コア、ペリフェラル、およびユーザーフレンドリーなMCUXpresso開発者エクスペリエンスに基づいて構築されたNXPのFRDM開発プラットフォームを活用しています。

- 2023年9月ダイキンオーストラリアは、ZigBee 3.0プロトコルを搭載し、ホワイト(BRC1H63W)およびブラック(BRC1H63K)仕上げの新しいスタイリッシュコントローラを発表。ZigBee3.0プロトコルを搭載し、ダイキンの各種ワイヤレスセンサーとのシームレスな接続を可能にしました。このアップグレードモデルは、オフタイマー、週間スケジュールタイマー、改良されたユーザーインターフェイスなどの追加機能を誇ります。また、専用アプリ「Daikin App」を使えば、ホーム画面からBluetooth機器と簡単にペアリングできます。また、ZigBee 3.0に対応したことで、さまざまなワイヤレスセンサーとの接続が可能になりました。ダイキンは、CO2センサー(CO2ZB1)、温湿度センサー(H24428)、人感センサー(H74426)、ドア・窓センサー(DWZB1-CE)の4種類のセンサーを提供しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 業界バリューチェーン分析

- COVID-19パンデミックの市場への影響評価

第5章 市場力学

- 市場促進要因

- 産業オートメーションとスマートホームにおけるコネクテッドデバイスの採用増加

- IoTエコシステム全体における高性能機器の低コスト化の動向の高まり

- 市場の課題

- ZigBee規格のネットワーク機器の製造における複雑さ

- 技術スナップショット

- Zigbeeメッシュ・ネットワーク

- Zigbee 3.0

- ZigBee RF4CE

- ZigBee PRO

- ZigBee IP

第6章 市場セグメンテーション

- エンドユーザー産業別

- IT・通信

- 住宅オートメーション

- 産業オートメーション

- ヘルスケア

- 小売

- その他のエンドユーザー産業

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- イタリア

- フランス

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 北米

第7章 ベンダー市場シェア

第8章 競合情勢

- 企業プロファイル

- Texas Instruments Incorporated

- NXP Semiconductors NV

- Microchip Technology Inc.

- Silicon Laboratories Inc

- Digi International Inc.

- Sena Technologies Inc.

- Nordic Semiconductor ASA

- Qualcomm Technologies Inc.

- Semiconductor Components Industries LLC(ON Semiconductor)

第9章 投資分析

第10章 市場の将来

目次

Product Code: 67134

The ZigBee Market size is estimated at USD 5.16 billion in 2025, and is expected to reach USD 6.91 billion by 2030, at a CAGR of 6.01% during the forecast period (2025-2030).

Key Highlights

- The surge in smart home device adoption globally is set to propel the demand for ZigBee-enabled devices in the coming years. With the smart home market expanding at a rapid pace, the need for smart consumer electronics and appliances that seamlessly integrate with home networks is on the rise. Utilizing the ZigBee protocol allows users to remotely control a range of home appliances, from lighting and HVAC systems to safety equipment, bolstering energy efficiency and curbing power wastage.

- Due to the expanding trend toward smart device adoption, the growing consumer electronics sector is predicted to boost the implementation of ZigBee-based communication services used for monitoring and controlling devices based on IEEE 802.15.4 throughout emerging countries.

- With significant advancements, the market is expected to be driven by growing demand for the ZigBee wireless network deployment on a large scale using low-cost, low-power solutions that can run for years on inexpensive batteries for a variety of monitoring and control applications across smart energy/smart grid and building automation systems.

- The acceptance of smart sensor technologies increases in connection, and breakthroughs in cloud computing have all aided in the acceptance and expansion of Industrial IoT. This trend is also predicted to increase ZigBee adoption in tiny industrial settings where manufacturing gadgets must interact over short distances. ZigBee is based on the 802.15.4 protocol, although security is not effectively handled by ZigBee developers. This vulnerability has piqued the interest of many information security professionals, who are investigating the security capabilities of the 802.15.4 protocol and the implementation of ZigBee radios in IoT devices.

- According to Ericsson Mobility report 2023, the Massive IoT technologies NB-IoT and Cat-M supporting wide-area use cases involving large numbers of low-complexity, low-cost devices with long battery lives and low-to-medium throughput continue to be rolled out across the world. Globally, 128 service providers have deployed or commercially launched NB-IoT networks, 60 have launched Cat-M, and 45 have deployed both technologies. The total number of cellular IoT connections is forecasted to reach around 3 billion at the end of 2023. The growth of massive IoT technologies is enhanced by added capabilities in the networks, enabling massive IoT to co-exist with 4G and 5G in frequency division duplex (FDD) bands via spectrum sharing.

ZigBee Market Trends

The Residential Automation Segment is Expected to Hold a Significant Share of the Market

- As the burden on available resources increases owing to urban population growth, there is a need for resource monitoring. As the Internet of Things (IoT) can gather data from sensors embedded in smart devices, it serves as the foundation for digital services that can aid in developing smart cities. IoT has given rise to many linked smart gadgets that are quickly becoming indispensable in modern households. The World Bank expects smart cities to contribute around 60% of global GDP by 2025.

- Smart buildings can also be linked to a smart grid, allowing smart building components and the electric grid to interact. This technology allows for more effective energy distribution, proactive maintenance, and swifter power outage resolution. The increased use of connected devices has resulted in the adoption of ZigBee, which aids in the proliferation of smart hubs. Amazon Echo, Google Home, Insteon Hub Pro, Samsung SmartThings, and Wink Hub are examples of smart home hubs.

- In addition, Tuya, a global vendor of tailored IoT platforms, provides a smart home automation hub. The technology will be equipped with Pegasus technology, which enables multiple smart home devices and comes with a Gigabit router and ZigBee gateway. Apart from platform and technology vendors, appliance manufacturers are incorporating ZigBee technology in their offerings. For example, XAL, an electronics manufacturing company whose major offerings are lighting systems, is increasingly offering ZigBee open communication standards along with DALI in its offerings.

- Furthermore, the Internet of Things (IoT) is rapidly becoming a reality, fueled by the rising significance of smart home gadgets and a surging consumer appetite for automation, aiming at both convenience and energy efficiency. The concept of connected living is taking center stage, primarily due to its capacity to bolster home residents' security. Notably, technological strides are spurring the uptake of these smart devices, which have a diverse array of applications within the connected home framework.

- Further, according to the US Census Bureau, the number of housing units in the United States has been growing Y-o-Y, and there were approximately 144 million homes in the past year. Further, in August 2023, approximately 114,200 home constructions started in the United States. Such a rise in residential construction is expected to create an opportunity for the studied market to grow. According to the 2024 State of Digital Nomads, London was the most visited city by digital nomads as of March 2024, accounting for roughly 2.3% of trips by digital nomads across the world. Such developments toward digital nomads are expected to drive the market studied.

North America is Expected to Account for the Most Significant Share in the Market

- North America is one of the prominent markets, owing to the growing need for advanced technology by numerous end-user industry players in the region. Additionally, the evolution of high-speed networking technologies in the area is aiding the market's growth. The retail sector is embracing domotics and automation for smart homes. It has a home automation system that controls the lights, entertainment system, appliances, and house climate. For instance, Philips Lighting Holding BV offers Hue, a smart lighting system that can see when residents are in the room and adjust lighting as needed.

- The IT and telecommunications sector is poised to dominate the market, driven by a rising appetite for network hardware integrating the ZigBee protocol. Silicon Labs' chips in products like Samsung's Smart Hub and Google's Wi-Fi router support BLE and ZigBee Pro. Furthermore, the ZigBee Alliance's "All Hubs Initiative" aims to bolster reliability, interoperability, and security across ecosystems. Adding to this momentum, D-Link unveiled its newest solutions featuring ZigBee technology.

- ZigBee's residential automation segment is expected to hold significant demand. An increasing number of vendors are incorporating technology into their offerings and forming alliances with other vendors. Further, according to the US Census Bureau, in August 2023, approximately 114,200 home constructions started in the United States. Such huge construction of new residents in the country would create an opportunity for the market studied to grow.

- The increasing use of IoT in healthcare is helping optimize operations. It offers vital solutions, such as remote monitoring. The usage of these solutions in the sector assists in providing better patient care. The solutions also empower physicians to deliver superlative care by increasing patients' engagement. Governments across the world are increasingly spending on healthcare to make sure that the healthcare benefits reach even the remotest places. This technology enables the healthcare systems to work efficiently. For instance, according to the OECD, the US government spent 16.9% of its GDP on healthcare.

- Further, the advancements of ZigBee would propel the adoption in the region. For instance, in ZigBee 3.0, the ZigBee Cluster Library (ZCL) contains all available clusters and thus provides a complete toolbox from which all devices take their clusters and associated functionality. The ZigBee 3.0 software stack incorporates a 'base device' that provides consistent behavior for commissioning nodes into a network. Further, ZigBee 3.0 supports the increasing scale and complexity of different wireless networks and muddles through large local networks of over 250 nodes. Additionally, ZigBee 3.0 provides enhanced network security.

ZigBee Industry Overview

The ZigBee market is semi-consolidated and consists of a few major players. In terms of market share, several players dominate the industry. However, as communication technology advances throughout the connection medium, new firms are strengthening their market presence and expanding their corporate footprint across emerging nations.

- April 2024: NXP Semiconductors introduces two cutting-edge multiprotocol wireless microcontroller units (MCUs) under its latest MCX W series. These MCUs support a range of protocols, including Matter, Thread, ZigBee, and Bluetooth Low Energy (BLE). The MCX W72x is the pioneer wireless MCU featuring Bluetooth Channel Sounding. NXP is specifically tailoring these offerings for industrial IoT applications. These additions complement NXP's recent releases in the form of the MCX A and MCX N series. Moreover, they leverage NXP's FRDM development platform, which is built on the MCX portfolio's architecture, core, peripherals, and user-friendly MCUXpresso developer experience.

- September 2023: Daikin Australia introduced the new Stylish Controller, available in white (BRC1H63W) and black (BRC1H63K) finishes, equipped with ZigBee 3.0 protocol. This enhancement allows seamless connectivity with a variety of Daikin's wireless sensors. The upgraded model boasts additional features, including an off-timer, a weekly schedule timer, and an improved user interface. Users can easily pair the controller with Bluetooth devices directly from the home screen using the dedicated Daikin App. The controller's ZigBee 3.0 compatibility broadens its connectivity options, supporting a range of wireless sensors. Daikin offers four sensor types: a CO2 sensor (CO2ZB1), a temperature and humidity sensor (H24428), a motion sensor (H74426), and a door/window sensor (DWZB1-CE).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porters Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of the COVID-19 Pandemic on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Adoption of Connected Devices Across Industrial Automation and Smart Homes

- 5.1.2 Rising Trend of Low Cost with High Performance Equipment Across IoT Ecosystem

- 5.2 Market Challenges

- 5.2.1 Complexity in the Manufacturing of Networking Equipment With ZigBee Standards

- 5.3 Technology Snapshot

- 5.3.1 Zigbee Mesh Network

- 5.3.2 Zigbee 3.0

- 5.3.3 ZigBee RF4CE

- 5.3.4 ZigBee PRO

- 5.3.5 ZigBee IP

6 MARKET SEGMENTATION

- 6.1 By End-user Industry

- 6.1.1 IT and Telecommunication

- 6.1.2 Residential Automation

- 6.1.3 Industrial Automation

- 6.1.4 Healthcare

- 6.1.5 Retail

- 6.1.6 Other End-user Industries

- 6.2 By Geography

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 Germany

- 6.2.2.3 Italy

- 6.2.2.4 France

- 6.2.3 Asia-Pacific

- 6.2.3.1 China

- 6.2.3.2 India

- 6.2.3.3 Japan

- 6.2.3.4 South Korea

- 6.2.4 Latin America

- 6.2.4.1 Brazil

- 6.2.4.2 Mexico

- 6.2.5 Middle East and Africa

- 6.2.1 North America

7 VENDOR MARKET SHARE

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Texas Instruments Incorporated

- 8.1.2 NXP Semiconductors NV

- 8.1.3 Microchip Technology Inc.

- 8.1.4 Silicon Laboratories Inc

- 8.1.5 Digi International Inc.

- 8.1.6 Sena Technologies Inc.

- 8.1.7 Nordic Semiconductor ASA

- 8.1.8 Qualcomm Technologies Inc.

- 8.1.9 Semiconductor Components Industries LLC (ON Semiconductor)

9 INVESTMENT ANALYSIS

10 FUTURE OF THE MARKET

ZigBee:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日