|

市場調査レポート

商品コード

1851139

航空機用スイッチ:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Aircraft Switches - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空機用スイッチ:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月25日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

概要

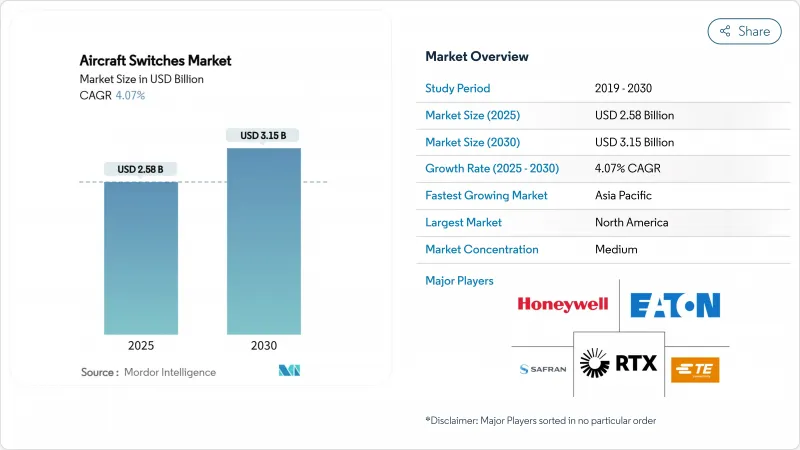

航空機用スイッチ市場規模は、2025年に25億8,000万米ドルと評価され、2030年には31億5,000万米ドルに拡大し、CAGR 4.07%で成長すると予測されています。

この軌跡は、電気サブシステムが従来の機械部品や油圧部品に取って代わり、機体全体のスイッチングポイントの数を増加させる、電動化アーキテクチャへの航空セクターの着実な軸足を反映しています。航空会社の機体更新スケジュールと国防近代化プログラムにより、2024年から2025年初頭にかけて、民間と軍用の両プラットフォームに一貫した注文の流れが確保されました。ソリッド・ステート・パワー・コントローラ、シリコン・カーバイド・デバイス、診断機能内蔵のスマート・スイッチが主流となり、離散的な電気機械部品から、予知保全統合が可能なソフトウェア定義のデータ共有モジュールへと重点が移りました。ベンダーの選択基準には、サイバーセキュリティーのコンプライアンスとサプライチェーンの完全性がますます含まれるようになり、中堅サプライヤーは認証のアップグレードに投資するか、大手同業他社からの統合提案を受け入れざるを得なくなりました。地域別では、北米が持続的な国防支出により売上高をリードしています。しかし、中国とインドが航空機の生産とMROの能力拡大を加速させたため、アジア太平洋地域が最も速い成長を記録しました。

世界の航空機用スイッチ市場の動向と洞察

次世代ナローボディ・プログラムにおける機材更新の波

航空アーキテクチャは、2024年に老朽化した単通路機体の更新を加速し、配電とフライトデッキ制御に高密度のスイッチングネットワークを必要とする電気アーキテクチャを指定します。ボーイングのB777X認証取得に向けた取り組みとエア・インディアの大型マルチ発注パッケージは、新規納入のたびに、コックピット、アビオニック・ベイ、客室ゾーンにまたがるスイッチのバンドル設置がどのように行われたかを典型的に示しています。オペレータは、20年の機体寿命にわたってソフトウェアのアップグレードに対応できる将来性のあるハードウェアを求め、ヘルス・モニタリング出力を備えた設定可能なソリッドステート・ユニットを提供するサプライヤを選好しました。

ソリッドステートスイッチを必要とする電動化サブシステムの急増

航空機の電化は二次システムから大電力作動ラインへと拡大し、スイッチの定格は500Aおよび1,000Vを超えました。Collins Aerospace社は、Clean Aviation SWITCHプログラムの下でメガワット級の電力分配モジュールを試作し、連続高温動作に対応する炭化ケイ素デバイスを検証しました。ハネウェルのシリコン・オン・インシュレータCMOSプロセスは、300℃定格のコンポーネントをサポートし、電力変換ベイをエンジンに近づけ、ハーネスの重量を減らすことを可能にしました。このような進歩は、プラットフォームOEMが分散型電気推進コンセプトに移行する中で、航空機用スイッチ市場を下支えしました。

適格部品認証待ち行列の遅延

FAAとEASAのエンジニアリング部門は、サイバーセキュリティとソフトウェア保証の審査が深まるにつれて案件の滞留に直面し、コンポーネント認可のリードタイムが12ヶ月から24ヶ月以上に伸びた。ボーイングのB777Xプログラムの遅延は、生産リリースを確定するための型式認証データを待つTier-1およびTier-2サプライヤーへの連鎖的な影響を浮き彫りにしました。専任の認証チームを持たない小規模のスイッチベンダーは、ラインフィットのポジションを失うリスクがあり、航空機用スイッチ市場全体の勢いを弱めています。

セグメント分析

コックピットスイッチは、パイロットがフライトに不可欠な作業を触覚プッシュボタン、ガード付きトグル、回転式セレクターに依存していたため、2024年の売上高の35.65%を維持した。ディスプレイやデータバスに障害が発生した場合、レギュレータは物理的なバックアップ制御ラインを必要とするため、手動設計が主流でした。このセグメントは、標準化されたオーバーヘッド・パネルによって統合が簡素化され、ユニット当たりのコストが低下した単通路航空機の持続的な納入から恩恵を受けました。

2030年までのCAGR予測では、航空電子工学の設置が最速の5.04%を記録しました。多機能ディスプレイ、フライト・マネジメント・コンピュータ、ヘルス・モニタリング・ユニットには、イーサネット・ベースのバックボーンでリンクされた高密度で低バウンスの自動リレーが必要でした。航空会社は、使用データを予測保守プラットフォームにストリーミングするスマートスイッチを組み込み、派遣の信頼性を向上させました。全体として、アビオニクスの成長は、統合型モジュール式アビオニクス・スイートの航空機用スイッチ市場規模の増加を支えました。

2024年の売上高の65.40%は手動式ユニットで、明確な触覚確認と簡単なライン・メンテナンスのために好まれる押しボタン・アセンブリが牽引しました。ロッカー型は、デザイン言語と照明効果により乗客の知覚を向上させる客室のポジションを獲得しました。手動の需要は、製造のスケールメリットと、複数のフリートにわたる安定した交換部品数を維持した。

自動スイッチは、電動化アーキテクチャが電気機械式コンタクタをソリッドステートコントローラに置き換えるため、CAGR 5.91%で上昇すると予測されます。アークフリーの半導体経路と機械的冗長性を組み合わせたハイブリッド・リレーが連続生産を開始し、低電圧降下とフェイルセーフの位置決めを組み合わせた。各配電センターには、従来のブレーカーに代わって、インテリジェントでアドレス指定可能なスイッチが何十個も設置されるようになり、この移行が航空機用スイッチ市場を拡大させています。

地域分析

北米は、包括的な防衛予算と活発な商業生産ラインに支えられ、2024年の売上高の37.80%を占めました。ボーイング、ハネウェル、カーティスライト、イートンがこの地域のサプライヤ・エコシステムを支え、FAA認証の専門知識が米国内のプログラム承認を集中させました。NGADとヘリコプターのアップグレードのための100億米ドル超の契約がいくつかあり、戦闘機、タンカー、回転翼機のカテゴリーにわたって一貫したスイッチ需要が確保されました。

CAGR5.60%で拡大が予想されるアジア太平洋は、中国のMROバリューチェーン上昇とインドの航空機受注急増から恩恵を受けました。エアバスは、中国のサービス部門が2043年までに610億米ドルに達し、整備が83%を占めると予測しました。インド政府は空港拡張のために120億米ドルを計上し、現地での部品生産を奨励したため、イートンとSIAECの提携に見られるように、欧米のサプライヤーは合弁会社を設立するようになりました。同地域の国産化重視の姿勢は、中堅メーカーに技術のライセンス供与や国産部品割当を獲得する機会を提供しました。

欧州は、エアバスの組立、GCAPの下での防衛協力、EUの気候変動基金に支援された研究開発プロジェクトに支えられ、安定を維持した。フランスとアイルランドで行われたコリンズ・エアロスペースのClean Aviation SWITCHプロトタイプは、ハイブリッド電気実証機のための高電圧配電戦略を検証し、地域の知的財産権を向上させました。同時に、EASAのサイバーセキュリティ義務化は認証の複雑性を高め、社内にコンプライアンス・リソースを持つサプライヤーを優遇し、航空機用スイッチ市場において適度な参入障壁を維持した。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 次世代ナローボディ・プログラムにおけるフリート更新の波

- ソリッドステートスイッチングを必要とする電動化サブシステムの需要が急増

- IFECと照明のアップグレードによる客室改装ブーム

- 急速な軍用回転翼機の再資本化予算

- スマートスイッチをバンドルしたデータ主導の予知保全契約

- 超小型リレーを可能にするシリコンオンインシュレータ(SOI)パワーデバイスのブレークスルー

- 市場抑制要因

- FAAとEASAにおける適格部品認証待ち行列の遅れ

- 銀カドミウム接点の原材料価格変動

- MROサプライチェーンにおける偽造部品の浸透

- スマートスイッチの部品コストを引き上げるサイバーハードニング要件

- バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 用途別

- コックピット

- キャビン

- エンジンとパワーアンシラリーユニット(APU)

- 航空電子工学

- その他

- スイッチタイプ別

- マニュアル

- 押ボタンスイッチ

- トグルスイッチ

- ロッカースイッチ

- ロータリースイッチ

- その他

- 自動

- 圧力スイッチ

- 温度スイッチ

- フロースイッチ

- リレーおよびコンタクタスイッチ

- その他

- マニュアル

- プラットフォーム別

- 固定翼機

- 回転翼航空機

- 無人航空機(UAV)

- エンドユーザー別

- OEM

- アフターマーケット

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- その他南米

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- その他中東

- アフリカ

- 南アフリカ

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Safran SA

- Honeywell International Inc.

- Eaton Corporation plc

- TE Connectivity Corporation

- RTX Corporation

- AMETEK, Inc.

- ITT Inc.

- CandK COMPONENTS LLC

- Electro-Mech Components, Inc.

- Unison Industries, LLC.

- Hydra-Electric Company

- Sensata Technologies, Inc.

- Vishay Intertechnology, Inc.

- Curtiss-Wright Corporation

- Schurter Holding AG

- Cygnet Aerospace Corp.

- Barantech

- Pressure Controls, Inc.

- AstroNova, Inc.