|

市場調査レポート

商品コード

1405348

航空機用インターフェースデバイス(AID):市場シェア分析、産業動向・統計、成長予測、2024年~2029年Aircraft Interface Devices Aid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空機用インターフェースデバイス(AID):市場シェア分析、産業動向・統計、成長予測、2024年~2029年 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 92 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

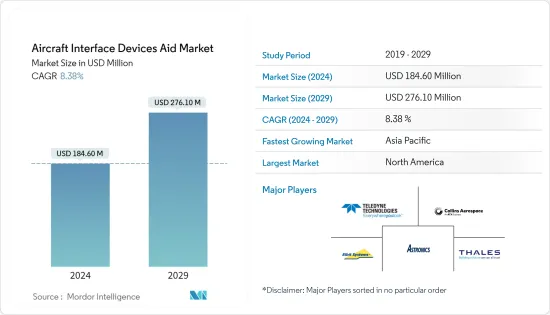

航空機用インターフェースデバイス(AID)市場規模は2024年に1億8,460万米ドルと推定され、2029年には2億7,610万米ドルに達すると予測され、予測期間中(2024-2029年)のCAGRは8.38%で成長する見込みです。

現在、商用航空部門と一般航空部門における航空機調達の増加が市場収益を牽引しています。健全性管理システムの発展と予知保全の重要性の高まりにより、航空機用インターフェースデバイス(AID)市場の成長が促進される可能性があります。また、航空機の安全性と効率性を向上させる必要性も、航空機用インターフェースデバイス(AID)の利用が拡大するもう1つの理由です。

主なハイライト

- いくつかの制約が航空機用インターフェースデバイス(AID)産業の発展を妨げる可能性があります。ハードウェア、ソフトウェア、設置、統合の価格を含む、航空機用インターフェースデバイス(AID)システム展開の初期コストの高さは、1つの大きな障壁です。リソースの限られた中小企業にとって、これは容易ではないかもしれないです。さらに、厳格な航空規則や基準を遵守する必要があるAIDの難しい認証プロセスは、AIDシステムの展開に課題を与え、遅れをもたらす可能性があります。

航空機用インターフェースデバイス(AID)の市場動向

予測期間中、商用航空機セグメントが最大の市場シェアを占める

- 予測期間中、商用航空機セグメントが現在市場を独占しています。さらに、新世代の航空機に対する需要の増加が市場を後押ししており、航空機用インターフェースデバイス(AID)は最新の商用航空機モデルでより重要な役割を果たしています。商用航空機セグメントでは、これらのデバイスは、従来の紙ベースのチャートに代わって、コックピット内のポータブルスクリーンの使用を拡大することにより、航空会社やMROステーションを支援します。これにより、パイロットは航空機データへのアクセスが容易になり、商用航空機整備業者は、これらの機器を通じて利用可能なリアルタイムデータからますます多くの利益を得ることができます。

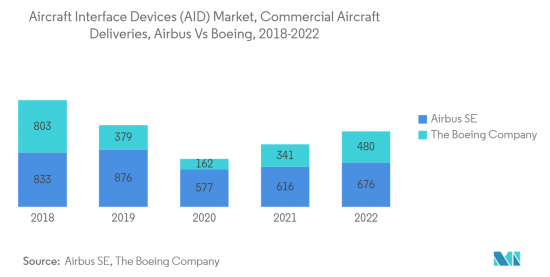

- さらに、リアルタイムのデータが利用可能になることで、航空会社はさまざまな性能パラメーターをモニターできるようになり、より良いフライトプランニングと運航コストの削減が可能になります。例えば、2023年5月、欧州の格安航空会社であるライアンエアーは、ボーイング社との間で、B737 MAX 10を150機購入する契約を締結し、さらに150機のオプションを追加しました。GEアビエーション、コリンズ・エアロスペース、L3ハリス・テクノロジーズ・インク、ハネウェル・インターナショナル・インク、コブハム・リミテッドといった企業が、ボーイング社の商用航空機ポートフォリオ内のさまざまなモデルにアビオニクス・コンポーネントを供給しています。

- その結果、これらの航空機用インターフェースデバイス(AID)を利用する商用航空機の需要が大きく、すべての商用航空機への統合が進んでいることから、今後数年間は商用セグメントからの収益が市場を独占すると予想されます。

予測期間中、アジア太平洋地域が航空機用インターフェースデバイス(AID)の急成長市場に

- アジア太平洋地域は、予測期間中に航空機用インターフェースデバイス(AID)の市場として急成長する見込みです。この地域は、世界で最も急速に成長している航空旅客輸送量を誇っており、主に中国、インド、日本、インドネシアなどの国々が牽引しています。これらの国は、インバウンド、アウトバウンド、国内旅客の流れの主要な航空市場として台頭してくると予想されています。このような航空需要の急増は、同地域における商用航空機のニーズの高まりと一致しており、その結果、インターフェイスデバイスを含むさまざまな航空機部品の需要を牽引しています。

- ボーイング社の予測によると、今後20年間に新たに納入される航空機の約40%はアジア太平洋地域で生産されると予想されており、航空機用インターフェイスデバイスの需要がさらに高まっています。特に、エア・インディアは6月20日、エアバス機250機とボーイング機220機(700億米ドル相当)の発注を固めました。

- さらに、この地域内の国々による軍用機の大幅な調達が進行中です。この地域の急成長する経済もまた、一般航空市場において極めて重要な役割を果たすことを予見しています。これらの要因が相まって、予測期間を通じてアジア太平洋地域における航空機用インターフェースデバイス(AID)の需要が大幅に増加すると予測されます。

航空機用インターフェースデバイス(AID)の産業概要

Astronics Corporation、THALES、Collins Aerospace(RTX Corporation)、Elbit Systems Ltd.、Teledyne Technologies Incorporatedなどが、同市場の著名なプレーヤーです。市場は統合されており、ほんの一握りのプレーヤーが主要シェアを占めています。しかし、各プレイヤーは革新的な技術を導入し、既存バージョンを定期的にアップグレードすることで新規顧客の獲得に努めているため、これらのプレイヤー間の競合は激しいです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 用途

- 商用

- 軍用

- 一般航空

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- エジプト

- カタール

- その他中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Astronics Corporation

- Anuvu

- Collins Aerospace(RTX Corporation)

- Avionics Interface Technologies

- Teledyne Technologies Incorporated

- THALES

- SKYTRAC Systems Ltd.

- Elbit Systems Ltd.

- Honeywell International Inc.

- ViaSat Inc.

- SCI Technology Inc.

第7章 市場機会と今後の動向

The Aircraft Interface Devices Aid Market size is estimated at USD 184.60 million in 2024, and is expected to reach USD 276.10 million by 2029, growing at a CAGR of 8.38% during the forecast period (2024-2029).

The growing aircraft procurement in the commercial and general aviation sectors is currently driving the market revenues. Developments in aircraft health management systems and the growing emphasis on predictive maintenance may boost the growth of the aircraft interface device market. Another reason for the growth in usage of aircraft interface devices is the need to improve the safety and efficiency of the aircraft.

Key Highlights

- A few limitations can hamper the development of the aircraft interface device (AID) industry. The high initial cost of aircraft interface device (AID) system deployment, which includes the price of hardware, software, installation, and integration, is one major barrier. For small and medium-sized firms with limited resources, this might not be easy. Additionally, the difficult certification process for AIDs, which necessitates adherence to exacting aviation rules and standards, may provide challenges and cause delays in the deployment of AID systems.

Aircraft Interface Devices Aid Market Trends

Commercial Aircraft Segment to have the Largest Market Share During the Forecast Period

- The commercial aircraft segment currently dominates the market during the forecasted period. Additionally, the increasing demand for new-generation aircraft is propelling the market, as aircraft interface devices play a more prominent role in the latest commercial aircraft models. Within the commercial aircraft segment, these devices assist airlines and MRO stations by expanding the use of portable screens in cockpits, replacing conventional paper-based charts. This facilitates greater access to aircraft data for pilots while enabling commercial aircraft maintenance providers to benefit increasingly from real-time data available through these devices.

- Moreover, real-time data availability enables airlines to monitor various performance parameters, allowing for better flight planning and potential reduction of operating costs. For instance, in May 2023, Ryanair, the European low-cost airline, entered an agreement with Boeing to purchase 150 B737 MAX 10 aircraft, with an option for an additional 150 jets. Companies such as GE Aviation, Collins Aerospace, L3Harris Technologies Inc., Honeywell International Inc., and Cobham Limited supply avionic components for different models within the Boeing Company's commercial aircraft portfolio.

- Consequently, with a substantial demand for commercial aircraft utilizing these aircraft interface devices and their increasing integration across all commercial aircraft, the revenue from the commercial segment is anticipated to dominate the market in the forthcoming years.

Asia-Pacific to be the Fastest Growing Market for Aircraft Interface Devices During the Forecast Period

- The Asia-Pacific region is poised to become the fastest-growing market for aircraft interface devices during the forecasted period. This region boasts one of the world's swiftest-growing air passenger traffic, primarily driven by countries such as China, India, Japan, and Indonesia, which are anticipated to emerge as key aviation markets for inbound, outbound, and domestic passenger flows. This surge in air travel demand aligns with an increasing need for commercial aircraft in the region, consequently driving the demand for various aircraft components, including interface devices.

- According to projections by Boeing, approximately 40% of the new aircraft deliveries in the next two decades are expected to be in the Asia-Pacific region, further amplifying the requirement for aircraft interface devices. Notably, Air India solidified its order for 250 Airbus aircraft and 220 new Boeing jets valued at USD 70 billion on June 20.

- Moreover, substantial procurement of military aircraft by countries within the region is underway. The region's burgeoning economy also foresees a pivotal role in the general aviation market. These combined factors forecast a significant upsurge in demand for aircraft interface devices within the Asia-Pacific region throughout the forecast period.

Aircraft Interface Devices Aid Industry Overview

Astronics Corporation, THALES, Collins Aerospace (RTX Corporation), Elbit Systems Ltd., and Teledyne Technologies Incorporated are among the prominent players in the market. The market is consolidated, with only a handful of players controlling the major share. However, the competition among these players is intense, as each one strives to attract new customers by introducing innovative technologies and regularly upgrading their existing versions.

For instance, in May 2023, RTX Corporation installed Collins Aerospace's InteliSight Aircraft Interface Device on over 200 JetBlue Airways Airbus A320 aircraft. This device captures, records, stores, encrypts, and securely transmits aircraft data to Collins' cloud platform, GlobalConnect, for real-time access. This enables JetBlue to adjust service schedules and enhance the aircraft's sustainability. Currently, there's a need for market penetration in the military sector, presenting an opportunity for these players to secure new contracts for military aircraft. Showcasing products with groundbreaking features tailored for military applications could help them attain these contracts.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Commercial

- 5.1.2 Military

- 5.1.3 General Aviation

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 Germany

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 South Korea

- 5.2.3.5 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Mexico

- 5.2.4.3 Rest of Latin America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 United Arab Emirates

- 5.2.5.2 Saudi Arabia

- 5.2.5.3 Egypt

- 5.2.5.4 Qatar

- 5.2.5.5 Rest of Middle-East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Astronics Corporation

- 6.2.2 Anuvu

- 6.2.3 Collins Aerospace (RTX Corporation)

- 6.2.4 Avionics Interface Technologies

- 6.2.5 Teledyne Technologies Incorporated

- 6.2.6 THALES

- 6.2.7 SKYTRAC Systems Ltd.

- 6.2.8 Elbit Systems Ltd.

- 6.2.9 Honeywell International Inc.

- 6.2.10 ViaSat Inc.

- 6.2.11 SCI Technology Inc.