バイオマーカー:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

Biomarkers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1939755

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

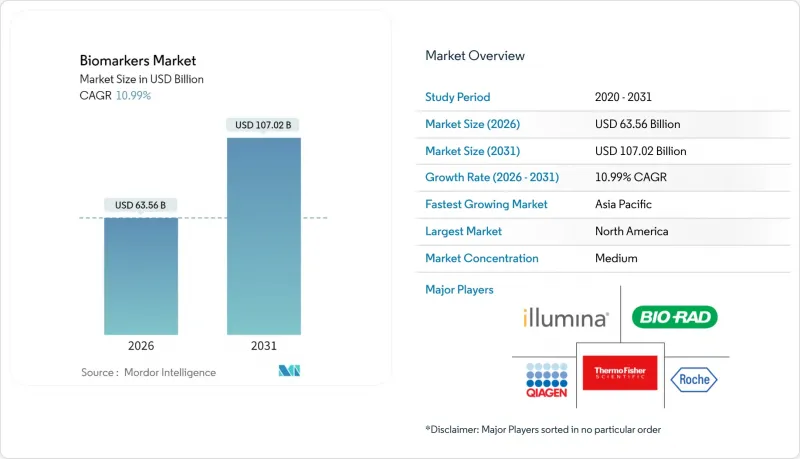

バイオマーカー市場は2025年に572億7,000万米ドルと評価され、2026年の635億6,000万米ドルから2031年までに1,070億2,000万米ドルに達すると予測されております。

予測期間(2026-2031年)におけるCAGRは10.99%と見込まれております。

この成長の勢いは、人工知能を活用した創薬パイプライン、デジタルエンドポイントに対する規制当局の広範な受容、ならびに腫瘍学、免疫学、神経学、心臓学分野における精密医療の推進を反映しています。継続的な画期的医療機器指定、拡大するマルチオミクスツールキット、および標的療法を評価する償還経路が、日常診療における検証済み検査の導入を促進しています。コンパニオン診断は現在、特に腫瘍学分野において治療決定の基盤となっており、液体生検やDNAメチル化アッセイが早期発見と治療マッチングへのアクセスを拡大しています。プロテオミクスプラットフォーム、クラウドバイオインフォマティクス、実世界エビデンスソリューションへの投資により、ベンダーは消耗品、サービス、ソフトウェアからの継続的な収益獲得が可能となります。しかしながら、複雑な償還政策とデータプライバシー規制が、短期的な導入曲線を抑制しています。

世界のバイオマーカー市場の動向と洞察

生命を脅かす疾患の増加傾向

慢性疾患および生命を脅かす疾患は、精緻化されたバイオマーカーパネルの需要を加速させています。関節リウマチは米国で年間20万件の新規症例が報告され、早期発見において感度74%、特異度90%を達成する14-3-3ηタンパク質アッセイの導入を促進しています。加齢関連疾患は低侵襲スクリーニングの必要性を高めており、アルツハイマー病では血液ベースのpTau217が最近FDAのブレークスルー指定を取得し、脳脊髄液検査を超えるアクセス性を向上させています。ヘルスケアシステムは予防医療へ軸足を移しており、がん、心臓病、神経変性疾患のマーカーを単一測定で計測可能なマルチプレックスプラットフォームが求められています。このような広範な需要が市場の堅調な成長軌道を支えています。

早期かつ正確な診断への需要拡大

早期介入戦略により、バイオマーカーは確認ツールではなく予測の要となります。マンモグラフィから5年乳がんリスクを予測するAIモデル「CLAIRITY BREAST」は、画像バイオマーカーが予防的スクリーニングを支える好例です。循環腫瘍DNAメチル化を検出する液体生検検査は、24時間以内のワークフローで肝細胞がんに対し96.67%の感度を達成しています。ウェアラブル機器は診療所外での検出を可能にし、心代謝指標の継続的モニタリングにより医師へのタイムリーなアラートを促します。人工知能強化型分析は解釈時間を短縮し、多様な医療現場への統合を容易にするとともに、バイオマーカー市場を拡大しています。

複雑な償還・規制経路

世界各国の異なる規制が商業化を遅らせています。FDAは4年間かけて検査室開発検査(LDT)に対する執行裁量権を段階的に廃止し、臨床検査室に医療機器レベルの規制を課す予定です。欧州の体外診断用医療機器規則(IVDR)はエビデンス要件を強化しましたが、アジア太平洋地域の要件は依然として不統一です。支払機関はしばしば追加の実世界エビデンスを要求するため、イノベーターの収益化が遅延し、バイオマーカー市場の拡大が若干鈍化しています。

セグメント分析

がん分野は2025年時点でバイオマーカー市場収益の45.94%を占めました。遺伝子・タンパク質マーカーへの数十年にわたる投資と、迅速承認制度によるコンパニオン診断薬の承認が主導的地位を支えています。エピジェネティックな液体生検検査では、10mlの採血から複数の腫瘍タイプを同定可能となり、早期治療へのアクセスが向上しています。

免疫疾患分野は2031年までにCAGR11.8%で拡大し、差を縮めています。自己免疫疾患の有病率上昇と、血清陰性関節リウマチにおける14-3-3ηタンパク質などのマーカーの有効性確認が新たな臨床ワークフローを開拓。サイトカインストームや治療反応を追跡可能な広範なマルチプレックスパネルが、バイオマーカー市場におけるこの分野の長期成長を牽引します。

有効性バイオマーカーは2025年の支出の57.78%を占め、進行予測、治療選択の指針、代替エンドポイントとしての活用が反映されています。腫瘍学および心臓病学の臨床試験では、確立されたマーカーを活用することで開発期間の短縮と投与量の最適化を図っています。

安全性バイオマーカーは、規制当局が市場承認前にヒト関連毒性指標を要求するため、11.67%のCAGRで最も急速に成長しています。AI搭載のin vitroモデルは数時間以内に腎臓および肝臓のストレス信号を読み取り、早期の治験中止判断を支援します。これらのパネルの拡大はリスク軽減戦略を支え、薬物監視分野におけるバイオマーカー市場規模を拡大します。

地域別分析

北米は2025年に世界収益の42.35%を占めました。これはFDAのプログラムがバイオマーカーの規制申請適格性を認定し、支払者による保険適用を効率化しているためです。堅調な償還制度と広範な病院ネットワークが検査高を維持しています。学界と産業界のコンソーシアムが研究から臨床応用への移行を加速させ、バイオマーカー市場における地域的な影響力を強化しています。

アジア太平洋地域は2031年までCAGR11.72%で拡大しています。中国の24項目にわたる規制改革により革新的医療機器の承認が加速する一方、日本の国家バイオテクノロジー計画は10年後の市場規模15兆円を目標としています。高齢化人口と液体生検の新償還コードが急速な普及を促し、アジア太平洋地域をバイオマーカー市場の主要需要拠点に位置づけています。

欧州は体外診断用医療機器規則(IVDR)の厳格なエビデンス要求のもとで着実な成長を維持しています。国境を越えた研究ネットワークにより大規模コホートが形成され、慢性疾患管理向けのデジタルバイオマーカーやマルチオミクスバイオマーカーの検証が進んでいます。中東・アフリカ・南米では、医療システムの近代化と医療観光が新興バイオマーカー市場エコシステムにおける高度診断需要を刺激し、新たな市場開拓の機会を提供しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 生命を脅かす疾患の増加傾向

- 早期かつ正確な診断に対する需要の高まり

- マルチオミクス技術の進展

- 腫瘍学分野におけるコンパニオン診断の拡大

- AIを活用したマルチモーダルバイオマーカー発見

- ウェアラブル機器によるデジタルバイオマーカーの普及

- 市場抑制要因

- 複雑な償還・規制経路

- 高コストなアッセイ開発・検証費用

- 実世界デジタルバイオマーカーにおけるデータプライバシーの課題

- 低資源研究所における検体から結果までのワークフローの変動性

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 疾患別

- がん

- 心血管疾患

- 神経疾患

- 免疫学的障害

- 腎臓疾患

- その他の疾患

- タイプ別

- 有効性バイオマーカー

- 予後バイオマーカー

- 予測バイオマーカー

- 薬理動態バイオマーカー

- 代替エンドポイントマーカー

- 安全性バイオマーカー

- バリデーションバイオマーカー

- 有効性バイオマーカー

- 機構別

- 遺伝子バイオマーカー

- エピジェネティックバイオマーカー

- プロテオミクスバイオマーカー

- 脂質バイオマーカー

- その他

- 用途別

- 臨床診断

- 創薬・医薬品開発

- 個別化医療

- 疾病リスク評価

- その他

- 製品別

- 消耗品

- 機器

- サービスおよびソフトウェア

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 市場シェア分析

- 企業プロファイル

- Abbott Laboratories

- F. Hoffmann-La Roche Ltd

- Thermo Fisher Scientific Inc.

- Qiagen N.V.

- Danaher Corp.(Beckman Coulter)

- Siemens Healthineers AG

- Bio-Rad Laboratories Inc.

- Agilent Technologies Inc.

- Illumina Inc.

- PerkinElmer Inc.

- Merck KGaA

- Becton Dickinson & Co.

- Hologic Inc.

- Sysmex Corp.

- Myriad Genetics Inc.

- Epigenomics AG

- Quanterix Corp.

- GE Healthcare

- BioMerieux SA

- Atlas Genetics Ltd

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日