|

市場調査レポート

商品コード

1642134

アプリケーションコンテナ:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Application Container - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| アプリケーションコンテナ:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 143 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

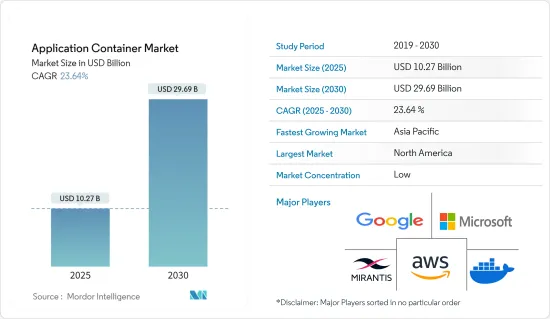

アプリケーションコンテナの市場規模は2025年に102億7,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは23.64%で、2030年には296億9,000万米ドルに達すると予測されます。

主なハイライト

- KubernetesやDockerのようなコンテナプラットフォームの登場は、ソフトウェアアプリケーションのデプロイメント、開発、管理に変革をもたらしました。企業がクラウドネイティブなアーキテクチャを採用し、ITインフラストラクチャを近代化する動きが加速する中、アプリケーションコンテナに対する需要は高まる見通しです。

- アプリケーションコンテナ市場の成長を後押しする主な要因には、AI(人工知能)などの先進技術の普及、ソフトウェア・サービスへの主な発展(特に新興国市場)、企業によるコンテナ・オーケストレーションとセキュリティ・サービスの世界展開などがあります。

- マイクロサービスアーキテクチャに不可欠なコンテナは、あらゆる規模のクラウドネイティブアプリケーションの原動力となってきました。しかし、その普及により、ランサムウェアやハッキングなどの脅威にさらされやすくなっています。ネットワーク・ポリシーの設定を誤ると、コンテナからの不正なトラフィックが許可され、セキュリティ境界が破られ、データの完全性が危険にさらされる可能性があります。

- コンテナは一時的な使用を前提に設計されているため、セキュリティ監視とインシデント対応が複雑になります。従来のセキュリティ・ツールは、コンテナの迅速な立ち上げと立ち下げが行われる環境では苦戦を強いられることが多いです。特に、コンテナがシャットダウンされると証拠が消滅する可能性があるためです。

- パンデミックの後、eコマース、オンライン・サービス、リモート・コラボレーションなど、コンテナ化に大きく依存する業界は顕著な成長を遂げました。これとは対照的に、観光業、接客業、小売業などの業界では、シャットダウンや消費者需要の減少に悩まされ、コンテナの採用が抑制された可能性があります。それでも、パンデミックの動向を反映したクラウド・コンピューティングとデータ変換アプリケーションの需要急増は、コンテナ導入の増加に拍車をかけた。

アプリケーションコンテナ市場の動向

クラウド・コンピューティングの採用増加が市場成長を牽引

- 従来のデータセンター・アウトソーシング(DCO)の減少に加え、クラウド・サービスや産業化されたオファリングの重要性が増していることは、ハイブリッド・インフラ・サービスへの顕著なシフトを示しています。DCOが下火になる一方で、コロケーションやホスティング、特にユーティリティ・インフラ・サービスへの支出が大幅に増加しています。この勢いは、クラウドIaaS(Infrastructure as a Service)やホスティングへの移行をさらに加速させると予想されます。

- Flexera Softwareの2023年版レポートによると、中小企業(SMB)の47%がAWS CloudFormationテンプレートを積極的に活用しています。AWS CloudFormationは、テンプレート化メカニズムを通じて、「スタック」と呼ばれるアプリケーションやサービスのプロビジョニングを簡素化します。2023年末までに、企業の29%が年間パブリッククラウド支出を公表しており、その額は1,200万米ドルを超えています。このような多額の支出は、一般的な動向を浮き彫りにしています。企業は、包括的なデジタルトランスフォーメーションの取り組みに後押しされ、クラウドへの移行を確実に進めています。こうした移行は、当然ながらアプリケーションコンテナに対する需要を増幅させる。

- 自動スケーリング機能を備えたKubernetesによって、アプリケーションはトラフィック需要に基づいてリアルタイムでリソースを調整できます。これにより、リソースの利用が効率化されるだけでなく、最適なユーザー・エクスペリエンスが保証されます。コンテナ・オーケストレーションを可能にすることで、Kubernetesはクラウド・コンピューティングにおいて、俊敏性の向上から優れたスケーラビリティに至るまで、数多くのメリットを提供します。

- クラウドコンテナは、特定のアプリケーションを仮想化するために設計されていることを認識することが不可欠です。例えば、MySQLコンテナの主な役割は、MySQLアプリケーションの仮想インスタンスを提供することです。Amazon、Google、Microsoft、IBMといった主要なクラウドプレイヤーは、コンテナ・アズ・ア・サービスを提供しています。重要なのは、これらのコンテナが特殊なサービスに限定されていないことです。

- クラウド・コンピューティングにおける仮想マシン(VM)の実用的な代用品としてコンテナを検討する企業が増えています。ラップトップ、オンプレミスシステム、クラウド上でシームレスに機能するコンテナの能力を考えると、コンテナはクラウドプロバイダーやハイブリッドクラウド構成にとって魅力的なインフラオプションとして浮上しています。

大きな成長を遂げるアジア太平洋地域

- 急速に進化する技術環境の中で、中国はモバイルアプリ開発の主要拠点として台頭してきました。世界最大のスマートフォン市場である中国では、さまざまな分野で洗練されたモバイル・アプリケーションに対する需要が急増しています。今後は、新たなテクノロジーを活用し、革新的なソリューションを構築し、ユーザー中心の体験を優先することが重視されます。注目すべきは、中国のコンテナ・アプリケーション企業が、国のデジタル進化の舵取りにおいて重要な役割を果たしていることです。

- プログレッシブ・ポリシー・インスティテュート(PPI)によると、インドは米国を追い抜き、2024年末までに世界最大の開発者人口を抱える国になる見通しです。大規模なコーディングの専門知識への依存を軽減するローコード/ノーコードアプリ開発の台頭は、この市場の拡大をさらに推進すると予想されます。その結果、この成長は国内のアプリケーションコンテナ需要を増幅させる可能性が高いです。

- さらに、開発者はプロセスを合理化し、小規模で独立したサービスに集中することで、市場投入までの時間を大幅に短縮しています。この戦略は、テスト段階を加速するだけでなく、バグ修正も迅速化します。マイクロサービスアーキテクチャへの意欲は、特に重要なモジュールやビジネス機能で高まっています。これを受けて、インドの企業は敏捷性を高めるためにマイクロサービス開発を迅速に採用しています。

- さらに、インドのデータセンター・セクターは、デジタル時代において著しい成長を遂げています。戦略的な位置付けを持つインドは、特にクラウド・コンピューティングの世界のデータセンター・ハブとして台頭しつつあり、有望な成長軌道を誇っています。インドのクラウド・サービス・プロバイダーは、アプリケーションコンテナの需要促進に貢献しています。規模の大小にかかわらず、アプリケーションをクラウドベースのプラットフォームに移行する企業が増えているため、この動向が国内のアプリケーションコンテナに対する意欲を高めています。

- 日本国内のクラウド市場は、オンプレミスシステムからクラウドソリューションへの移行と、クラウド中心のサービスに対する需要の高まりによって、力強い成長を目の当たりにしています。この変化は、特にリモートワークの増加、テクノロジーへの依存度の増加、リモート通信やネットワークシステムの維持管理の急増など、ワークダイナミクスの変化によってさらに加速しています。さらに、日本が企業全体でクラウドファースト戦略を急速に取り入れたことで、クラウドコンピューティング分野の安定性と拡大が強化されました。

アプリケーションコンテナ業界の概要

アプリケーションコンテナ市場には、世界のプレーヤーと地域的なプレーヤーが混在して存在感を競っています。参入障壁が高いにもかかわらず、複数の新規参入企業がニッチの開拓に成功しています。この分野の主要プレイヤーには、Mirantis, Inc.、Docker, Inc.、Amazon Web Services, Inc.、Google, LLC、Microsoft Corporationなどがいます。

製品の差別化が中程度から高程度で、市場浸透が進んでいることが特徴で、この市場は激しい競争状態にあります。通常、ソリューションはバンドルされ、サービスは製品に統合されます。

費用を管理するため、多くのユーザーは年間契約を好みます。ベンダーによっては、パブリック・コンテナ・ベースのソフトウェアを契約価格モデルで提供しています。このモデルでは、ユーザーは決められたライセンス数を一括前払いで購入し、決められた期間だけソフトウェアにアクセスすることができます。このような契約により、コンテナ型ソリューションへの需要が高まり、リアルタイムのアップデートが可能になった。プロバイダーはパートナーシップやイノベーションに多額の投資を行い、競合情勢に拍車をかけています。まとめると、この市場における競争企業間の敵対関係は顕著です。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 市場に対するマクロ経済要因の評価とCOVID-19の影響

第5章 市場力学

- 市場促進要因

- クラウドベースコンピューティングの採用拡大

- 市場抑制要因

- 技術に伴うセキュリティリスク

- 市場参入戦略

- 新興企業に合わせた市場参入戦略の提案

- パートナーシップ、チャネル、マーケティング活動などの市場参入アプローチに関する洞察

- テクノロジーとイノベーションの動向

- 市場に関連する新技術やイノベーションの概要

- 市場のリスクと機会

- 新興企業にとっての未開拓の機会や市場ギャップの特定

- 消費者/企業の採用とペインポイント

- 消費者や企業が現在のテクノロジー/ソリューションで直面している課題についての洞察

- 独自の価値提案、または切迫した問題の解決

第6章 コンテナの主な使用事例

- 管理とオーケストレーション

- モニタリング

- デブオプス

- セキュリティ

- ネットワーキング

- ストレージ

第7章 市場セグメンテーション

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- スペイン

- アジア

- 中国

- インド

- 日本

- オーストラリア・ニュージーランド

- ラテンアメリカ

- ブラジル

- アルゼンチン

- メキシコ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- 北米

第8章 競合情勢

- 企業プロファイル

- Mirantis, Inc.

- Docker, Inc.

- Amazon Web Services, Inc.

- Google, LLC

- Microsoft Corporation

- Oracle Corporation

- Red Hat, Inc.

- Portainer.io. Ltd.

- Heroku Services(Salesforce.com)

第9章 比較製品分析

第10章 市場機会と今後の動向

The Application Container Market size is estimated at USD 10.27 billion in 2025, and is expected to reach USD 29.69 billion by 2030, at a CAGR of 23.64% during the forecast period (2025-2030).

Key Highlights

- The emergence of container platforms like Kubernetes and Docker has transformed the deployment, development, and management of software applications. As organizations increasingly adopt cloud-native architectures and modernize their IT infrastructures, the demand for application containers is poised to rise.

- Key factors propelling the growth of the application container market include the widespread adoption of advanced technologies, such as AI (Artificial Intelligence), increased investments in software services-particularly in developing countries-and the global rollout of container orchestration and security services by enterprises.

- Containers, integral to microservices architectures, have been the driving force behind cloud-native applications of all scales. However, their widespread adoption renders them vulnerable to threats like ransomware and hacking. Misconfigured network policies can permit unauthorized traffic from containers, breaching security perimeters and risking data integrity.

- Containers, designed for transient use, complicate security monitoring and incident response. Conventional security tools often struggle in environments where containers are swiftly spun up and down. This rapid lifecycle makes it challenging to detect and analyze security incidents, especially since evidence can dissipate once a container is shut down.

- In the wake of the pandemic, industries such as e-commerce, online services, and remote collaboration - heavily reliant on containerization-experienced notable growth. In contrast, sectors like tourism, hospitality, and retail grappled with shutdowns and dwindling consumer demand, which may have tempered their adoption of containers. Still, the surging demand for cloud computing and data transformation applications, mirroring the pandemic's trends, spurred an increase in container adoption.

Application Container Market Trends

Increased Adoption of Cloud-based Computing to Drive the Market Growth

- The growing prominence of cloud services and industrialized offerings, alongside a decline in traditional data center outsourcing (DCO), indicates a marked shift towards hybrid infrastructure services. While DCO experiences a downturn, spending on colocation and hosting, particularly in conjunction with utility infrastructure services, is witnessing a significant rise. This momentum is anticipated to further accelerate the transition towards cloud Infrastructure as a Service (IaaS) and hosting.

- According to the 2023 Flexera Software report, 47% of small and medium-sized businesses (SMBs) actively utilized AWS CloudFormation templates. AWS CloudFormation simplifies the provisioning of applications or services, referred to as "stacks," through its templating mechanism. By the end of 2023, 29% of enterprises disclosed annual public cloud spending, surpassing USD 12 million. Such substantial expenditure highlights a prevailing trend: organizations are unwaveringly transitioning to the cloud, propelled by comprehensive digital transformation initiatives. These transitions naturally amplify the demand for application containers.

- Kubernetes, with its auto-scaling feature, allows applications to adjust resources in real time based on traffic demands. This not only streamlines resource use but also guarantees an optimal user experience. By enabling container orchestration, Kubernetes offers numerous benefits in cloud computing, ranging from enhanced agility to superior scalability.

- It's essential to recognize that cloud containers are designed to virtualize specific applications. For example, a MySQL container's primary role is to provide a virtual instance of the MySQL application. Major cloud players like Amazon, Google, Microsoft, and IBM offer containers-as-a-service. Importantly, these containers aren't confined to specialized services; they can function on both public and private cloud platforms.

- More organizations are considering containers as practical substitutes for virtual machines (VMs) in cloud computing. Given their ability to function seamlessly on laptops, on-premises systems, and in the cloud, containers emerge as a compelling infrastructure option for cloud providers and hybrid cloud configurations.

Asia Pacific to Register Major Growth

- In the rapidly evolving tech landscape, China has emerged as a leading hub for mobile app development. As the world's largest smartphone market, China witnesses a significant surge in demand for sophisticated mobile applications across diverse sectors. Moving forward, the emphasis will be on harnessing emerging technologies, crafting innovative solutions, and prioritizing user-centric experiences. Notably, Chinese container application firms play a crucial role in steering the nation's digital evolution.

- As per the Progressive Policy Institute (PPI), India is on track to eclipse the US, positioning itself as the home to the world's largest developer population by the end of 2024. The ascent of low-code/no-code app development, which reduces the reliance on extensive coding expertise, is anticipated to propel this market's expansion further. Consequently, this growth is likely to amplify the demand for application containers in the country.

- Furthermore, developers are streamlining their processes, leading to a notable reduction in time-to-market by focusing on smaller, independent services. This strategy not only accelerates the testing phase but also expedites bug-fixing. The appetite for microservices architecture is growing, especially for critical modules and business functions. In response, Indian businesses are swiftly adopting microservices development to boost their agility.

- Moreover, India's data center sector is witnessing a significant upswing in the digital era. With its strategic positioning, the nation is set to emerge as a global data center hub, particularly for cloud computing, and boasts a promising growth trajectory. Cloud service providers in India are instrumental in propelling the demand for application containers. As more organizations, regardless of size, pivot to cloud-based platforms for their applications, this trend amplifies the nation's appetite for application containers.

- Japan's domestic cloud market is witnessing vigorous growth, spurred by a transition from on-premise systems to cloud solutions and an escalating demand for cloud-centric services. This shift is further catalyzed by changing work dynamics, especially the rise of remote work, increased reliance on technology, and a surge in remote communications and network system upkeep. Additionally, Japan's rapid embrace of a cloud-first strategy across its enterprises has fortified the stability and expansion of its cloud computing sector.

Application Container Industry Overview

The application container market features a mix of global and regional players competing for prominence. Despite high entry barriers, several newcomers have successfully carved out a niche. Key players in this arena include Mirantis, Inc., Docker, Inc., Amazon Web Services, Inc., Google, LLC, and Microsoft Corporation.

Characterized by moderate to high product differentiation and increasing market penetration, this market is fiercely competitive. Typically, solutions are bundled, integrating the service into the product offering.

To manage expenses, many users prefer annual contracts. Some vendors provide public container-based software with a contract pricing model. This model allows users to make a one-time upfront payment for a set number of licenses, granting access to the software for a chosen duration. Such arrangements have spurred demand for containerized solutions, enabling real-time updates. Providers are heavily investing in partnerships and innovations, fueling the competitive landscape. In summary, the competitive rivalry in this market is pronounced.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of Macroeconomic Factors on the Market and Impact of COVID-19

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increased Adoption of Cloud-based Computing

- 5.2 Market Restraints

- 5.2.1 Security Risks Associated With the Technology

- 5.3 Market Entry Strategies

- 5.3.1 Recommendations for Market Entry Strategies Tailored for a Startup

- 5.3.2 Insights into Go-to-Market Approaches, including Partnerships, Channels, and Marketing Efforts

- 5.4 Technology and Innovation Trends

- 5.4.1 Overview of Emerging Technologies or Innovations Relevant to the Market

- 5.5 Market Risks and Opportunities

- 5.5.1 Identification of Untapped Opportunities or Market Gaps for a Startup

- 5.6 Consumer/Enterprise Adoption and Pain Points

- 5.6.1 Insights into Challenges Faced by Consumers or Businesses with Current Technologies/Solutions

- 5.6.2 Unique Value Proposition or Solve a Pressing Problem

6 MAJOR CONTAINER USE-CASE AREAS

- 6.1 Management and Orchestration

- 6.2 Monitoring

- 6.3 DevOps

- 6.4 Security

- 6.5 Networking

- 6.6 Storage

7 MARKET SEGMENTATION

- 7.1 By Geography

- 7.1.1 North America

- 7.1.1.1 United States

- 7.1.1.2 Canada

- 7.1.2 Europe

- 7.1.2.1 United Kingdom

- 7.1.2.2 Germany

- 7.1.2.3 France

- 7.1.2.4 Spain

- 7.1.3 Asia

- 7.1.3.1 China

- 7.1.3.2 India

- 7.1.3.3 Japan

- 7.1.4 Australia and New Zealand

- 7.1.5 Latin America

- 7.1.5.1 Brazil

- 7.1.5.2 Argentina

- 7.1.5.3 Mexico

- 7.1.6 Middle East and Africa

- 7.1.6.1 United Arab Emirates

- 7.1.6.2 Saudi Arabia

- 7.1.6.3 South Africa

- 7.1.1 North America

8 COMPETITIVE LANDSCAPE

- 8.1 Company Profiles

- 8.1.1 Mirantis, Inc.

- 8.1.2 Docker, Inc.

- 8.1.3 Amazon Web Services, Inc.

- 8.1.4 Google, LLC

- 8.1.5 Microsoft Corporation

- 8.1.6 Oracle Corporation

- 8.1.7 Red Hat, Inc.

- 8.1.8 Portainer.io. Ltd.

- 8.1.9 Heroku Services (Salesforce.com)