MEMS:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

MEMS - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 2100618

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

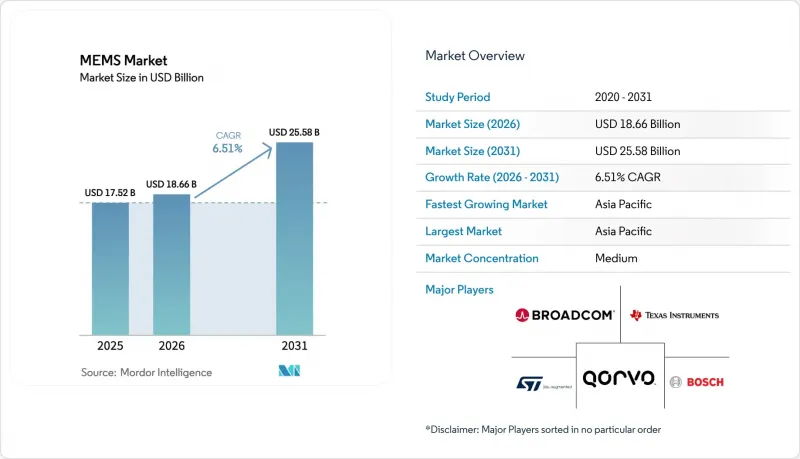

Mordor Intelligenceによると、MEMS市場の規模は、2025年の175億2,000万米ドルから2026年には186億6,000万米ドルへと拡大し、2026年から2031年にかけてCAGR6.51%で推移し、2031年には255億8,000万米ドルに達すると予測されています。

本レポートは、デバイスカテゴリー(センサー、アクチュエータなど)、センサー/アクチュエータの種類(慣性、圧力など)、用途(民生用電子機器、自動車など)、製造プロセス(バルク、表面など)、材料(シリコン、ポリマー、圧電体、金属など)、および地域(北米、南米、欧州など)ごとに分類されています。市場予測は金額(米ドル)ベースで提示されています。

世界のMEMS市場の動向と洞察

IoTエッジノードにおけるセンサーの普及

エッジゲートウェイには、わずか3年前には2~3個だったMEMSデバイスが、現在では5~8個組み込まれており、デバイス上での振動分析、ガス検知、温度監視が可能になっています。クアルコムの2025年向けIoTサービススイートでは、MEMS加速度計と機械学習モデルを組み合わせることで、誤警報を40%削減しています。RISC-Vマイクロコントローラを中核とした20米ドル未満のセンサーノードは、導入のハードルを下げています。スマート農業への導入事例では、土壌水分や気象センサーがフィルタリングされたデータをクラウドにアップロードする前にローカルで中継することで、スケールメリットが実証されています。ファームウェア規格のばらつきは依然としてシステム統合を遅らせ、製品認定サイクルを長期化させています。

ADASの安全性向上のためのEV 1台あたりのMEMS搭載数の拡大

レベル3の自動運転セダンには、ISO 26262の機能安全要件に準拠するため、従来の自動車の12個から増加し、現在18~22個のMEMSデバイスが組み込まれています。TDKのIAM-20685モジュールには、10ミリ秒以内にドリフトを検知する自己診断回路が組み込まれており、ティア1のフェイルオペレーショナル要件を満たしています。電気機械式ブレーキ・バイ・ワイヤ・システムには、1 kHzでサンプリングを行う高精度圧力センサーが必要とされます。一方、中国で2026年に施行されるタイヤ空気圧規制により、年間2,500万個の需要が追加される見込みです。しかし、製造拠点がドイツや日本に集中していることから、自動車メーカーはサプライチェーンの混乱にさらされるリスクがあります。

特殊プロセスラインへの多額の初期設備投資

2025年、Rogue Valley Microdevices社は、200mmベイ1基に深反応性イオンエッチング装置およびウエハーボンディング装置を導入するために、1億8,000万米ドルを投じました。多様なチップに費用を分散できるCMOSファブとは異なり、MEMSラインは限られた製品ファミリーのみに対応するため、多角化が制限されます。「CHIPS法」や「欧州チップ法」は、既存の主要企業に補助金を配分していますが、スタートアップ企業は依然として8桁の参入コストに直面しています。自動車用や医療用プロセスの再認定には18ヶ月を要する場合があるため、ファウンダリは変更に消極的であり、それがイノベーションの鈍化につながっています。

セグメント分析

2025年には、スマートフォンや自動車向けに10億個単位で出荷された慣性センサーモジュールにより、センサーがMEMS市場の61.43%を占め、市場を席巻しました。マイクロ流体チップは、7.23%という最も高いCAGRを牽引しています。これは、分散型診断が、検査サイクルを数日から数分に短縮する使い捨てカートリッジに依存しているためです。単位あたりの経済性はセンサーの大量生産に有利ですが、ラボ・オン・チップ用消耗品の利益率は依然として高く、多角化を図るサプライヤーがマイクロ流体ファウンダリの生産能力を増強する誘因となっています。インクジェットヘッドなどのアクチュエータは、交換サイクルが成熟しており成長が制限されていますが、MEMS発振器は5Gのタイミング同期要件の恩恵を受けています。新興のパワーハーベスターは、変換効率が10%未満であるためニッチな存在にとどまっていますが、バッテリー交換にコストがかかる遠隔地の産業拠点では採用が進んでいます。

拡大するマイクロ流体分野は、対象となるヘルスケア顧客基盤を広げます。救急部門でベッドサイドでの血液ガス検査が導入される中、アボット社のイリノイ州施設の拡張は、カートリッジ需要の高まりを裏付けています。FDA 510(k)認可に基づく規制経路により、増分型バイオMEMSの市場投入までの期間が短縮され、既存企業の優位性がさらに強まっています。一方、コモディティ化の圧力にさらされているセンサー分野では、ベンダー各社が価格設定を正当化するために、オンチップ融合や機械学習への移行を迫られています。この対照的な状況は、MEMS市場が「量産型センサー」と「高利益率の特定用途向けマイクロ流体」の2つに分岐しており、それぞれが異なる製造ロードマップを必要としていることを示しています。

2025年には、加速度計やジャイロスコープがスマートフォンの画面回転、フィットネス追跡、自動車の安定性制御を支えることから、慣性センサーのシェアは42.53%を占めました。音声アシスタントがフラッグシップモデルからミッドレンジデバイスへと移行するにつれ、MEMSマイクロフォンはCAGR8.31%を記録すると予測されており、70 dBの信号対雑音比により遠距離からの音声コマンドが可能になります。圧力センサーは、タイヤ空気圧監視システムや人工呼吸器向けの需要が堅調に推移しており、一方、RF-MEMS部品は5Gの普及に伴い需要が拡大し続けていますが、依然としてコストへの敏感さが残っています。光学MEMSは、プロジェクションやLiDARといったニッチ市場に対応しており、性能面での優位性が販売数量の少なさを補っています。

GoerTekは2025年に12億個のマイクロフォンを出荷し、コストと小型化の面でKnowlesに課題があります。民生用加速度計の平均販売価格は0.50米ドルを下回り、サプライヤーは差別化を図るためセンサーフュージョンエンジンの組み込みを進めています。RF-MEMSサプライヤーは、QorvoやBroadcomが特許ポートフォリオを擁護する中でロイヤリティの累積に直面しており、新規参入の障壁が高まっています。汎用慣性デバイスと高付加価値のマイクロフォンの混在は、MEMS市場の市場セグメンテーションと、分野ごとに異なるイノベーションの原動力を浮き彫りにしています。

地域別分析

アジア太平洋地域は2025年の売上高の52.31%を占めて首位に立ち、2031年までCAGR7.13%で成長を続ける見込みです。中国におけるタイヤ空気圧監視システムの義務化により、年間2,500万個の圧力センサー需要が追加される一方、日本と台湾は、それぞれ圧電薄膜および28 nm MEMSロジックの共集積化を専門としています。韓国は、世界のスマートフォンブランド向けに垂直統合型のマイクロフォン供給を行っており、これによりリードタイムを短縮し、地域での優位性を強めています。インドおよび東南アジアは、急成長している価格に敏感な市場であり、慣性センサーを搭載したミッドレンジ端末の採用は増加しているもの、常時オン状態の音声起動機能などのプレミアム機能の導入は先送りされています。

北米は、自動車、防衛、医療の各クラスターに支えられ、2025年の売上高の約23%を占めました。「CHIPS法」による520億米ドルの補助金は、国内のMEMS生産ライン向けに割り当てられており、Rogue Valley Microdevices社はオレゴン州の生産能力拡大のために7,500万米ドルの資金を確保しました。FDAの510(k)承認プロセスにより、医療用MEMSの商用化サイクルは12ヶ月が可能となり、収益の見通しが加速しています。人件費の高さから、大量生産されるスマートフォン用センサーは依然として海外生産が主流ですが、特殊デバイスや防衛用慣性計測ユニットは、セキュリティ上の理由から国内生産が維持されています。

欧州は約18%のシェアを占めており、ドイツの自動車用センサー大手であるボッシュ、インフィニオン、コンチネンタルの3社を中核としています。430億ユーロ規模の「欧州チップ法」は、X-FABにおける300mmプロセスへのアップグレードに資金を提供し、ADAS向け加速度計の単価2米ドル未満という目標を支援しています。フランスのSTマイクロエレクトロニクスは、世界中のウェアラブル機器向けにマルチセンサーモジュールを供給しており、一方、英国のケンブリッジ・クラスターでは、LiDARや拡張現実(AR)ディスプレイ向けの光学MEMSスタートアップ企業の育成が行われています。RoHSやREACHに基づく規制枠組みにより、鉛系および特定のポリマー材料の認定基準が厳格化され、サプライヤーの材料ロードマップに影響を与えています。南米、中東・アフリカの合計シェアは7%未満ですが、ブラジルの自動車需要、UAEのスマートシティプロジェクト、南アフリカの鉱業用センサーが牽引役となっています。しかし、輸入関税やインフラの不足により、成長は制約されています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストによるサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- IoTエッジノードにおけるセンサーの普及

- ADASの安全性を高めるため、EV1台あたりのMEMS搭載量の拡大

- 5Gの普及がRF-MEMSフィルターおよびスイッチの需要を押し上げている

- 300 mmウエハーレベルMEMS製造への移行

- ポイント・オブ・ケア診断向けマイクロ流体バイオMEMSの成長

- ヒアラブル向け超低消費電力ピエゾMEMSスピーカー

- 市場抑制要因

- 特殊プロセスラインにおける初期設備投資の高さ

- ファウンダリグレードの設計ルールおよび規格の欠如

- ScドープAlNおよびその他のニッチ材料の供給リスク

- RF-MEMSの知的財産権の複雑化がロイヤリティ費用の増加を招いています

- 業界バリューチェーン分析

- 規制情勢

- 技術展望

- マクロ経済要因が市場に与える影響

- ポーターのファイブフォース分析

第5章 市場規模と成長予測

- デバイスカテゴリ別

- センサー

- アクチュエーター

- 発振器およびタイミング

- マイクロ流体チップ

- 電源/モーション用マイクロ発電機

- センサー/アクチュエータの種類別

- 慣性センサー

- 圧力センサー

- RF MEMS

- 光学MEMS

- 環境センサー

- MEMSマイクロフォン

- マイクロボロメーターおよび赤外線検出器

- インクジェットヘッド

- その他のセンサー/アクチュエータの種類

- 用途別

- 家庭用電子機器

- 自動車

- 産業用およびロボット分野

- ヘルスケアおよび医療機器

- 通信インフラ

- 航空宇宙・防衛

- その他の用途

- 製造プロセス別

- バルク・マイクロマシニング

- 表面マイクロマシニング

- 深反応性イオンエッチング(DRIE)

- 絶縁膜上シリコン(SOI)MEMS

- LIGA/X線リソグラフィー

- 高度な3DプリントMEMS

- 素材別

- シリコン

- ポリマー

- 圧電材料(AlN、PZT)

- 金属

- 化合物半導体

- 石英およびガラス

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他の南米諸国

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他の欧州諸国

- アジア太平洋

- 中国

- 日本

- 韓国

- インド

- オーストラリア

- ニュージーランド

- その他のアジア太平洋諸国

- 中東

- アラブ首長国連邦

- サウジアラビア

- トルコ

- その他の中東諸国

- アフリカ

- 南アフリカ

- ナイジェリア

- ケニア

- その他のアフリカ諸国

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Robert Bosch GmbH

- Broadcom Inc.

- STMicroelectronics N.V.

- Texas Instruments Inc.

- Qorvo Inc.

- TDK Corporation(InvenSense)

- Infineon Technologies AG

- NXP Semiconductors N.V.

- Knowles Electronics LLC

- Panasonic Corporation

- GoerTek Inc.

- Honeywell International Inc.

- Murata Manufacturing Co., Ltd.

- Analog Devices Inc.

- Alps Alpine Co., Ltd.

- Omron Corporation

- Sensata Technologies

- Silex Microsystems AB

- Teledyne MEMS

- Rogue Valley Microdevices Inc.

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日