|

市場調査レポート

商品コード

1939749

サイバー戦争:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Cyber Warfare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| サイバー戦争:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 127 Pages

納期: 2~3営業日

|

概要

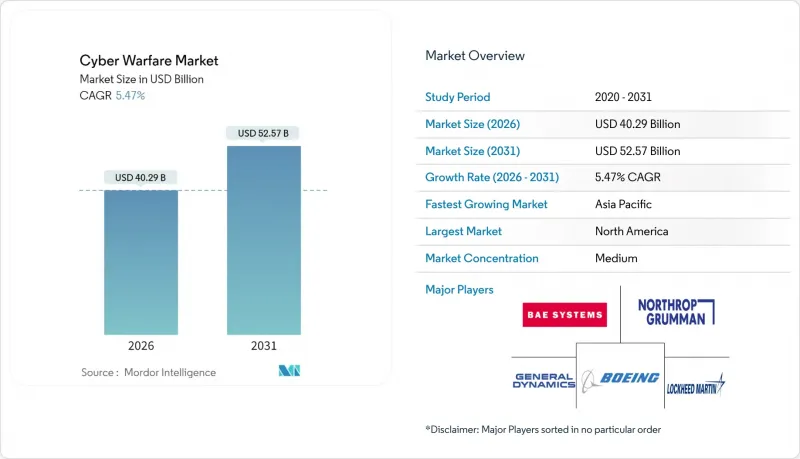

サイバー戦争市場は2025年に382億米ドルと評価され、2026年の402億9,000万米ドルから2031年までに525億7,000万米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは5.47%と見込まれます。

国家主体の攻撃の激化、軍事C4ISRネットワークの急速なデジタル化、自律型ツールの普及により、サイバー空間の戦略的価値は高まり続けており、各国防衛省はこの領域における保護と戦力投射を推進しています。北米は技術的優位性を維持する一方、重要インフラへの攻撃が激化しており、アジア太平洋地域では地域緊張の高まりが調達サイクルを加速させ、最も成長の速い市場となっています。かつて周辺領域であった医療分野では、病院グループが軍事レベルの防御策を採用せざるを得ない高度なランサムウェアが脅威となっています。一方、防衛主要企業とサイバーセキュリティ専門企業間の買収主導型統合は、人工知能と自律対応エンジンを融合した統合型攻防ソリューションへの移行を示唆しています。

世界のサイバー戦争市場の動向と洞察

国家が支援するサイバー諜報活動の激化

サイバー作戦は断続的な諜報活動から継続的な「持続的関与」へと移行し、軍隊は攻撃的ハンティングチームと強靭な防御態勢への投資を迫られています。米国サイバーコマンドの2024年先行ハンティング作戦は、抑止力が敵対者ネットワーク内への事前配置に依存するようになったことを明確にしました。中国の戦略支援部隊も同様のアプローチを採用しており、これに対抗する地域諸国はマルウェア開発、ゼロデイ攻撃の備蓄、欺瞞ツールの予算拡大を進めています。攻撃の帰属が不明確であるため、否定可能な攻撃が可能となり、エスカレーションのリスクが高まり、サイバー戦争市場全体の需要が持続しています。脅威インテリジェンスと自動応答機能をパッケージ化したベンダーが支持を集めています。これは、政府が機密性を損なうことなく意思決定サイクルを短縮する圧力に直面しているためです。

軍事C4ISRネットワークの急速なデジタル化

同盟軍は、センサー、射撃装置、意思決定ノードを相互接続する統合全領域指揮フレームワークへ移行中です。デジタル化は作戦上の機敏性をもたらす一方、敵対者がゼロデイアクセスを狙う攻撃対象領域を拡大します。AI支援計画ツールが現在ミッションクリティカルなネットワーク内に存在し、分析上の利点と並行して新たな脆弱性を生み出しています。その結果、調達プログラムではエンドポイント検知、ゼロトラストアーキテクチャ、クロスドメインゲートウェイを統合し、データフローの保護を図っています。強化された通信システムへの継続的な資金投入は、多国籍任務部隊間での相互運用性を認証できるサイバー戦争市場ベンダーにとって、長期的な成長を約束するものです。

機密扱いのサイバー戦争要員の深刻な不足

最高機密扱いの認可を受けたオペレーター職の欠員は2024年に急増し、審査待ち期間は18ヶ月にまで延びました。指揮官は人材確保にプログラム予算を割り当てるため、新規ツールの調達予算が圧迫されています。サイバーレンジやAIベースの指導により、実務を通じた学習が加速され、スキルギャップは部分的に解消されました。しかしながら、機密取扱許可の審査遅延が戦力生成プロセスを遅らせています。この制約により、各機関が新たな攻撃プラットフォームを運用開始できる速度は制限され、サイバー戦争市場の長期的な成長は抑制される見込みです。

セグメント分析

防衛・航空宇宙分野は2025年時点でサイバー戦争市場シェアの32.08%を占め、攻撃的エクスプロイトと多層防御を組み合わせた機密予算が牽引しています。医療分野は絶対額では小規模ながら、ランサムウェア組織が医療の緊急性を悪用して支払いを強要するため、6.83%という最速のCAGRを記録しています。BFSI(銀行・金融・保険)分野のサイバー戦争市場規模は安定しています。規制当局が多層的な安全対策を義務付ける一方、国家レベルの脅威アクターがサプライチェーン侵入へ移行する中、企業セクターは軍事レベルのソリューションへ移行しているためです。公益事業・エネルギー事業者は調達を産業安全規制と連動させ、ITとOTのセキュリティを統合プラットフォームを重視する形で融合させています。防衛以外の政府民間機関は、有権者データや公共サービスポータルの保護を目的とした脅威ハンティング契約を追求しています。港湾閉鎖といった注目を集める事件を受け、運輸企業も調達リストに名を連ね、エンドポイント隔離や暗号化テレメトリーの需要が高まっています。業界横断的な融合が進む中、ベンダーは製品群のモジュール化を推進し、企業ITからミッションクリティカルシステムへコードベースの分岐を必要とせずシームレスに拡張可能なツールを実現しています。この汎用性により、従来は民生用サイバーセキュリティツールを購入していた顧客層においても、サイバー戦争市場の拡大が促進されています。

成長のダイナミクスは、軍事サイバー戦略を参照する傾向が強まる業界固有の規制や保険条項の影響を受けています。防衛主要企業は、長年にわたる関係を活用して分析機能の拡張を民間産業にアップセルし、収益源を拡大しています。医療コンソーシアムは情報共有同盟を形成し、脅威インテリジェンスを防衛研究所へフィードバックすることで、パッチ適用サイクルを加速させております。銀行は、国家戦略を検知する防衛由来のテレメトリーフィードを購読することで、状況認識能力を高めております。このようなクロスオーバーは、ある分野のデータが別の分野のセキュリティ成果を強化するサイバー戦争産業のエコシステムを強化し、複数セグメントの拡大を持続させる正のネットワーク効果を生み出しております。

地域別分析

2025年時点で北米はサイバー戦争市場の31.18%を占め、米国が主導しています。同国の防衛支出は攻撃的侵入部隊と大規模サイバー演習場の双方を資金面で支えています。ファイブ・アイズ情報ネットワークはプラットフォーム需要を拡大させており、カナダ、英国、オーストラリア、ニュージーランドが相互運用可能なソリューションを調達し、テレメトリーデータをリアルタイムで共有しているためです。米国の先制攻撃戦略は、エンドポイントテレメトリー、欺瞞グリッド、継続的関与サイクルを支えるミッション特化型エクスプロイトチェーンへの支出を定着させています。カナダは重要鉱物サプライチェーン保護のため調達を拡大し、メキシコは国境を越えた貿易回廊を保護するため選択的に投資しています。

アジア太平洋地域は2031年までCAGR6.98%で拡大すると予測されており、南シナ海における戦略的対立や台湾周辺で激化するサイバー偵察活動を反映しています。中国の戦略支援部隊が地域投資を促進。日本はサイバー部隊の人員を倍増、韓国はAI対応防御ラティスに資金投入、オーストラリアは米国インド太平洋軍との合同レッドチーム演習を調整。インドは「デジタル・バーラト・シャクティ」政策下で国産プラットフォームを推進し、輸入依存度を低減するとともに地域ベンダーエコシステムを育成。シンガポールやベトナムを含む東南アジア諸国は、デジタル貿易の拡大に伴う脅威環境の変化を受け、SOC(セキュリティオペレーションセンター)の近代化を優先課題としています。

欧州ではNATOの教義が調達を統一し、EUサイバー連帯法が共同防衛プロジェクトの資金調達を効率化することで着実な拡大が見られます。ドイツとフランスは自律型攻撃プラットフォームに新規資金を配分し、北欧の公益事業者は電力網妨害対策として耐寒性防御システムを調達しています。ロシアのハイブリッド戦術を警戒する東欧諸国は、国境防衛計画に機動型インシデント対応部隊を統合中です。中東諸国はエネルギー収益をサイバー兵器庫に投入し、地域紛争における非対称的優位性を確立しています。アフリカおよび南米の軍隊は海底ケーブルや衛星ノードを保護するパイロットプロジェクトを開始しており、世界のサイバー戦争市場規模を拡大する新たな機会が生まれつつあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 国家が支援するサイバー諜報活動の激化

- 軍事C4ISR*ネットワークの急速なデジタル化

- 重要インフラ攻撃の急増が防衛予算の拡大を促す

- NATO「サイバー領域」戦略と加盟国の調達サイクル

- AI搭載自律型攻撃ツールの拡散

- 商用衛星インターネットが新たな攻撃対象領域を創出

- 市場抑制要因

- 機密取扱許可を有するサイバー戦要員の深刻な不足

- 帰属の複雑さが比例応答を制限している

- 攻撃的サイバー作戦に関する国際法の断片化

- オープンソースおよびCOTSコンポーネントにおけるサプライチェーンの信頼性ギャップ

- マクロ経済要因の影響

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- エンドユーザー業界別

- 防衛・航空宇宙

- BFSI

- 企業向け

- 電力・公益事業

- 政府

- ヘルスケア

- 運輸・物流

- その他のエンドユーザー産業

- 展開モード別

- オンプレミス

- クラウドベース

- ハイブリッド

- ソリューションタイプ別

- 攻撃プラットフォームおよびエクスプロイト

- 防御プラットフォーム(SOC、SIEM、EDR)

- 訓練、シミュレーション、サイバーレンジ

- アドバイザリー、監査およびレッドチームサービス

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- 東南アジア

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- BAE Systems plc

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- General Dynamics Corporation

- The Boeing Company

- L3Harris Technologies, Inc.

- Leonardo S.p.A.

- Airbus Defence and Space SAS

- Thales Group

- Booz Allen Hamilton Holding Corporation

- Science Applications International Corporation(SAIC)

- Palantir Technologies Inc.

- CrowdStrike Holdings, Inc.

- Check Point Software Technologies Ltd.

- Darktrace plc

- Elbit Systems Ltd.

- Kaspersky Lab JSC

- Trend Micro Incorporated

- Fortinet, Inc.

- Parsons Corporation

- FireEye Government Solutions LLC

- NCC Group plc

- CyberArk Software Ltd.