|

市場調査レポート

商品コード

1910604

エッジAIハードウェア:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Edge AI Hardware - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| エッジAIハードウェア:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 163 Pages

納期: 2~3営業日

|

概要

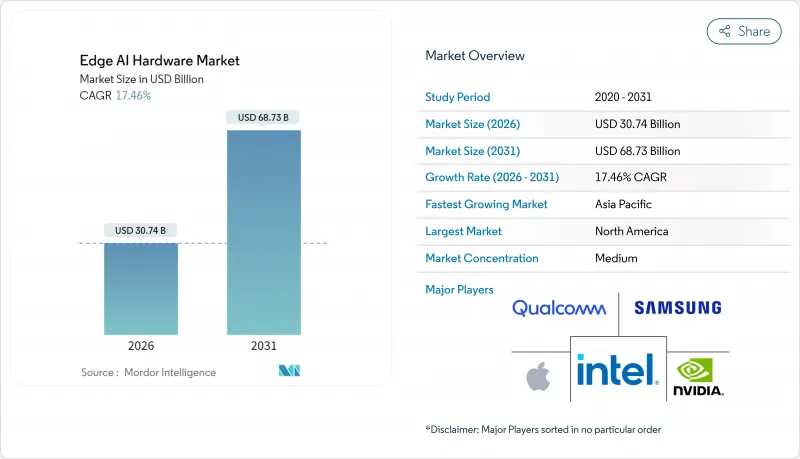

エッジAIハードウェア市場は、2025年に261億7,000万米ドルと評価され、2026年の307億4,000万米ドルから2031年までに687億3,000万米ドルに達すると予測されています。

予測期間(2026年~2031年)におけるCAGRは17.46%と見込まれます。

この成長の勢いは、遅延を削減し、データの主権を保護し、エネルギー消費を低減するオンデバイス推論への需要増加に起因しています。プレミアムクラスのスマートフォン、AI対応パーソナルコンピュータ、および必須の自動車安全システムが、短期的な成長を支えています。CHIPS and Science Act(チップス・アンド・サイエンス法)などの政府の奨励策は国内生産能力を促進し、5Gを活用したマルチアクセスエッジコンピューティング(MEC)は対応可能なワークロードを拡大しています。競合の激しさは中程度であり、多様な半導体大手企業が、ワット当たりの性能を最適化する特定用途向けチップサプライヤーに対してシェアを守っています。先進ファウンドリにおけるサプライチェーンの集中化と輸出規制の拡大は地域的な複雑さを増す一方、自国での代替技術開発を促進しています。

世界のエッジAIハードウェア市場の動向と洞察

AI対応パーソナルコンピューティングの台頭がプロセッサアーキテクチャを変革

最新ノートPCチップに搭載された専用ニューラルプロセッシングユニット(NPU)は、ローカルAIスループットで40~50TOPSを達成し、大規模言語モデルや生成ワークロードをオフラインで即時応答時間にて実行可能にします。Microsoft Copilot+PCによる新たな設計基準は、全てのOEMメーカーに同様のアクセラレーション統合を促し、汎用コアではなくヘテロジニアスコンピューティングへのロードマップを導いています。2030年までの半導体ロードマップは推論最適化タイルを優先し、エッジ中心ノードへの持続的な需要を牽引しています。

スマートフォンAI機能によるプレミアムセグメントの刷新サイクル

フラッグシップモバイルプロセッサは45~50 TOPSの推論性能を実現し、AIタスクを専用エンジンに割り当てることでバッテリー寿命を延長します。デバイス内翻訳、生成型画像処理、パーソナルアシスタント機能は、プレミアム層全体で明確なアップグレード動機を生み出し、買い替えサイクルを短縮します。ミッドレンジ設計は前年のフラッグシップ機能を継承し、専用AIシリコンの大量出荷を拡大します。

先進ノード製造コストが市場参入を制限

3nmデバイスの開発には、マスク代として1億米ドル以上、ウェハー1枚あたり2万米ドル以上のコストがかかり、新規参入者の参入を制限しています。小規模企業が規模拡大やニッチ分野での差別化を図る中、業界再編が加速しています。ノード最適化設計とチップレット分割によりコストは一部相殺されますが、既存の供給契約を持つ既存企業の優位性はさらに強化されます。

セグメント分析

GPUデバイスは、成熟したソフトウェアスタックと高い並列スループットにより、2025年にエッジAIハードウェア市場シェアの50.12%を占めました。予測期間中、設計者がワット当たりの性能を重視するにつれ、ASICとNPUは18.74%のCAGRで成長すると見込まれます。自動車および産業分野の買い手が決定論的レイテンシと機能安全を優先するため、ASIC向けエッジAIハードウェア市場規模は急激に拡大すると予想されます。CPUは、汎用リソースを必要とする混合ワークロードにおいて価値を維持し、FPGAは通信および防衛分野における再構成可能な役割で成長を続けます。

チップレットパッケージングはCPU、GPU、NPUタイルを共通基板上に統合し、各ダイを異なるタスクに最適化しつつメモリインターフェースを共有します。ベンダー各社はシリコン層でセキュリティエンクレーブと機能安全モニターを統合し、医療・自動車分野の規制要件を満たします。複数ファウンドリ戦略は地政学的リスクを軽減しますが、先進ノードへの依存は主要ファブとの交渉力を維持します。

2025年時点のエッジAIハードウェア市場規模において、スマートフォンは年間更新サイクルと大量生産を背景に39.25%を占めました。しかしながら、自律航行や視覚解析が低遅延推論を必要とするロボット・ドローン分野が最も急速に成長し、19.32%のCAGRで拡大しています。専用エッジボードは視覚プロセッサと深度センサーを組み合わせ、ミリ秒単位の障害物回避を実現します。

カメラはエッジAIを統合し、筐体内でリアルタイム検知を実行。これにより小売分析やスマートシティにおける映像バックホールコストを削減します。ウェアラブル機器は超低消費電力ニューラルエンジンを採用し、限られたバッテリー予算下でも継続的に健康データを抽出します。スマートスピーカーは音声キャプチャ、ビームフォーミング、NLP推論を単一チップに集約。部品点数を削減し、音声をローカルに保持することでプライバシーを強化します。

地域別分析

北米は2025年に520億米ドルのCHIPSインセンティブと、自動車・小売・医療分野における企業パイロット事業の先行展開を背景に、38.92%の収益シェアを占めました。スタートアップ企業はベンチャーキャピタルの集積を活用し、特定分野向けアクセラレーターの商用化を推進しています。輸出管理政策により海外販売は制約される一方、国内の防衛・航空宇宙需要は確保されています。

アジア太平洋地域は19.27%のCAGRで成長し、他地域を凌駕しています。中国は輸入規制回避のため国産GPU・NPUベンチャーを支援し、韓国は国家AIチップラインに70億米ドルを投入。日本のSociety 5.0構想は、決定論的エッジコンピューティングを必要とするスマート工場改造を促進しています。

欧州は430億ユーロの「チップ法」のもと、主権確保の目標と予算の現実とのバランスを図っています。ドイツとフランスの自動車産業拠点では機能安全対応のエッジ推論を優先し、GDPR準拠がオンプレミス分析を促進しています。イスラエルの活気あるスタートアップエコシステムは防衛・医療画像分野の使用事例をターゲットとし、EMEA全域へボードを輸出しています。

ラテンアメリカでは農業用ドローンやスマートシティ監視システムへの早期導入が進んでいます。中東では物流・エネルギーインフラ向けAIをホストするため、エッジゲートウェイを組み合わせた主権データセンターへの投資が加速しています。アフリカは発展途上ながら、衛星バックホールと連携したモバイルファースト展開により、従来の技術基盤を飛び越える進化を遂げています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- AI搭載パーソナルコンピューティング(AI PC)の台頭

- スマートフォンにおけるAI搭載に向けたアップグレードサイクル

- 5Gおよび6GによるMEC導入の遅延低減効果

- 自動車向けL2-L4 ADASエッジ推論需要

- 省エネルギー型アナログおよびPIMアクセラレータ

- 政府によるCHIPS法スタイルのインセンティブ

- 市場抑制要因

- 先進ノードにおける初期開発費用(NRE)の高騰

- 断片化されたツールチェーンとソフトウェアのロックイン

- エッジ指向の機械学習およびシリコン分野における人材不足

- サプライチェーンの地政学的輸出規制

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- マクロ経済要因の影響

第5章 市場規模と成長予測

- プロセッサー別

- CPU

- GPU

- FPGA

- ASICおよびNPU

- デバイス別

- スマートフォン

- カメラおよびスマートビジョンセンサー

- ロボットとドローン

- ウェアラブル機器

- スマートスピーカーおよびホームハブ

- その他のエッジデバイス

- エンドユーザー業界別

- 民生用電子機器

- 自動車・輸送機器

- 製造業および産業用IoT

- ヘルスケア

- 政府および公共安全

- その他のエンドユーザー産業

- 導入場所別

- デバイスエッジ

- ニアエッジサーバー

- ファーエッジ/MEC

- クラウド支援型ハイブリッド

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- 韓国

- インド

- シンガポール

- オーストラリア

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- エジプト

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- NVIDIA Corporation

- Intel Corporation

- Qualcomm Incorporated

- Samsung Electronics Co., Ltd.

- Apple Inc.

- Advanced Micro Devices, Inc.

- Huawei Technologies Co., Ltd.

- Alphabet Inc.(Google LLC)

- Amazon.com, Inc.

- Alibaba Group Holding Limited

- Baidu, Inc.

- Continental AG

- DENSO Corporation

- Robert Bosch GmbH

- Kalray S.A.

- MediaTek Inc.

- Imagination Technologies Limited

- Hailo Technologies Ltd.

- SiMa.ai, Inc.

- BrainChip Holdings Ltd.

- Syntiant Corp.

- Mythic, Inc.

- Gyrfalcon Technology Inc.