|

市場調査レポート

商品コード

1438434

小型スポーツ航空機:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Light-Sport Aircraft - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 小型スポーツ航空機:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 75 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

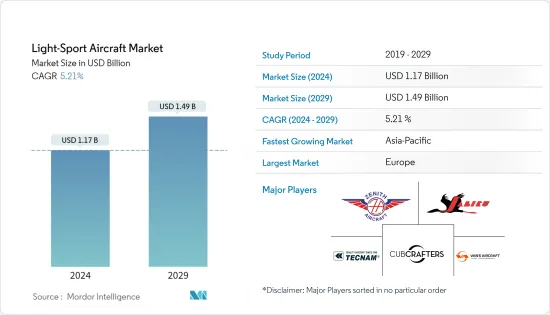

小型スポーツ航空機の市場規模は、2024年に11億7,000万米ドルと推定され、2029年までに14億9,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に5.21%のCAGRで成長します。

2020年は、新型コロナウイルス感染症(COVID-19)のパンデミックにより、LSAに関連するスポーツ活動に対する民間需要が混乱しました。ウイルスの蔓延を抑えるために課されたロックダウンにより、観光客の流入が減少しました。COVID-19感染症のパンデミックにより、世界中でいくつかのLSA運営施設が一時閉鎖を余儀なくされ、多くの新規開発プロジェクトが経済低迷と慎重な投資家によって打撃を受けています。それにもかかわらず、世界の旅行・観光産業が徐々に回復しており、LSA活動の需要が増加すると予想されているため、需要低迷は短期間にとどまると予想されます。

スポーツやレクリエーション活動でのLSAの使用は、旅行および観光部門の成長と愛好家の数の増加により増加しています。世界中でパイロットを訓練する必要性が高まっていることから、LSA訓練も重要性を増しています。一方で、主要な航空規制機関は、業界の成長を支援し、新たなLSA調達を促進するために、新しい規制要件の導入と既存の規制要件の修正に取り組んでいます。これも市場の成長を促進すると予想されます。

小型スポーツ航空機市場動向

2020年に最大の市場シェアを占めたのは航空機セグメント

現在、調査対象となっている市場では航空機セグメントが最も高いシェアを占めています。 LSAの飛行機カテゴリは市場で最も一般的で比較的安価であるため、レクリエーション活動、熱心な飛行、新しいパイロットの訓練に適しています。北米、欧州、中東の一部などの地域におけるアドベンチャースポーツの成長が、航空機部門の成長の主な理由です。一方で、航空会社、訓練機関、航空当局はパイロットの訓練と資格取得のコストを削減しようと努めています。この点において、LSAは、従来使用されていたピストンまたはターボプロップエンジンを動力とする一般航空航空機よりも調達およびメンテナンスのコストが低く、燃料消費も少ないため、LSAの採用が増加しています。

工場で製造された航空機の需要がキットで製造された航空機よりも大きいことが観察されました。しかし、キットから航空機を組み立てることが容易になり、情報が入手できるようになったことで、この傾向は急速に変化しています。 2020年には、工場で製造されたものと比較して、キットで製造された製品の登録数が増加しました。軽飛行機の需要の高まりに伴い、いくつかのメーカーが新世代の航空機を導入しています。たとえば、2021年の初めに、Terrafugiaは、FAAがライトスポーツカテゴリー(S-LSA)での移行走行可能な航空機を認定するための特別な耐空性証明書を付与し、この航空機が飛行可能になると発表しました。 Terrafugiaは、初期の飛行専用バージョンを製造および販売する予定であり、2022年までに航空機を商業化するために設計をさらに開発する予定です。このような開発は、予測期間中に市場の成長を促進すると予想されます。

欧州は予測期間中に最大の市場になると予想されます

現在、欧州は最も高い市場シェア収益を持っており、予測期間中もその優位性が続くと予想されます。この地域には、いくつかの観光スポットと、軽スポーツ機のアクティビティに適した地理的特徴があります。これらの航空機の採用の増加に伴い、この地域の航空規制機関は業界の成長を支援し、新しいLSAの調達と運用を促進するために新しい規制を導入しています。 2020年、EASA(欧州安全庁)は、米国のLSAに相当する600 kgの超軽量製品を欧州で許可し始めました。

より低いMTOW制限で飛行するウルトラライトは、再認定された場合にのみ重量クラスをアップグレードできます。ただし、2021年半ばの時点で、欧州の一部の国家規制当局はこの再認定を許可していませんでしたが、他の規制当局はこの変更を歓迎していました。その一方で、EASAはPPL SEP(およびLAPLライセンス)更新に向けて超軽量(およびセイルプレーン)の使用を許可するという譲歩も行った。これは、主に超軽量航空機を操縦するパイロットを助けることが期待されています。過去10年間に、いくつかの新しい航空機メーカーがこの地域で操業を開始しました。したがって、需要の増加に応えるために、最近多くの新しいLSAモデルがリリースされています。これを踏まえ、Flight Design General Aviation GmbHは2020年 4月にCTLS 2020 Sport Editionを発売しました。CTLS 2020は、改良された外装と内装を提供しながら、技術的および空力的なアップグレードを特徴としています。このような発展は、予測期間中にこの地域の市場の成長を促進すると予想されます。

小型スポーツ航空機業界の概要

小型スポーツ航空機市場は細分化されており、レジャーや飛行訓練市場向けに小型スポーツ航空機モデルを提供する多くの地元および地域の航空機メーカーが存在します。小型スポーツ航空機市場における著名なプレーヤーには、Costruzioni Aeronautiche Tecnam SpA(Tecnam)、Cub Crafters Inc.、Jabiru Aircraft Pty Ltd、Zenith Aircraft Company、およびVan's Aircraft Inc.などがあります。市場のプレーヤーは新しい航空機モデルを投入しています。これらは、地理的存在と販売を拡大するために、連邦航空局と欧州連合航空安全局から認定を受けています。たとえば、Tecnamは、2020年 2月と2020年 11月に、それぞれP2002 Sierra MkIIとP92 Echo MkII軽飛行機に対して、ドイツの新しい600kg規則に基づく認証を取得しました。ドイツの型式承認は他の欧州諸国でも認められています。その一方で、企業は市場での存在感をさらに高めるために、ハイブリッド電気推進システムなどの最新の推進技術を搭載した新しい航空機の開発にも投資しています。このような発展により、今後数年間で市場の競争力がさらに高まることが予想されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

- USDの通貨換算レート

第2章 調査手法

第3章 エグゼクティブサマリー

- 市場規模と予測、世界、2018~2027年

- タイプ別の市場シェア、2021年

- 地域別市場シェア、2021年

- 市場の構造と主要参入企業

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション(金額別の市場規模と予測、2018~2027年)

- タイプ

- 飛行機

- 水上飛行機

- 地域

- 北米

- 欧州

- アジア太平洋

- 世界のその他の地域

第6章 競合情勢

- ベンダーの市場シェア

- 企業プロファイル

- Costruzioni Aeronautiche TECNAM SpA

- Pipistrel doo

- ICON Aircraft

- Cub Crafters Inc.

- Czech Aircraft Group SRO

- Paradise Aero Industry

- Van's Aircraft Inc.

- Flight Design General Aviation GmbH

- JMB Aircraft sro

- Jabiru Aircraft Pty Ltd

- TL-ULTRALIGHT sro

- American Legend Aircraft Company

- Stemme Production GmbH

- Aeropro sro

- Zenith Aircraft Company

第7章 市場機会と将来の動向

The Light-Sport Aircraft Market size is estimated at USD 1.17 billion in 2024, and is expected to reach USD 1.49 billion by 2029, growing at a CAGR of 5.21% during the forecast period (2024-2029).

The COVID-19 pandemic disrupted the civilian demand for sporting activities related to LSA in 2020. The lockdowns imposed to curb the virus' spread reduced the tourist inflow. Due to the COVID-19 pandemic, several LSA operating facilities around the world have been forced to close temporarily, and many new development projects have been hammered by tanking economies and cautious investors. Nevertheless, the demand slump is expected to remain short-lived, as the global travel and tourism industry is slowly rebounding, which is anticipated to increase the demand for LSA activities.

The usage of LSA for sporting and recreational activities has witnessed growth due to the growth in the travel and tourism sector and the increase in the number of enthusiasts. LSA training is also gaining significance, with the growing need for training pilots globally. On the other hand, major aviation regulatory bodies are working on introducing new regulatory requirements and modifying the existing ones to support the industry's growth and encourage new LSA procurements. This is also expected to drive market growth.

Light-sport Aircraft Market Trends

The Airplane Segment Accounted for the Largest Market Share in 2020

Currently, the airplane segment of the market studied has the highest share. The airplane category of LSAs is the most common in the market and is comparatively cheap, thus making them more preferable for recreational activities, enthusiastic flyers, and training new pilots. The growth of adventure sports in regions like North America, Europe, and some parts of the Middle East, is the primary reason for the growth of the airplane segment. On the other hand, the airlines, training institutes, and aviation authorities have been trying to bring the pilot training and certification costs down. In this regard, the adoption of LSAs is increasing, as they offer a lower cost of procurement and maintenance and lower fuel burn than conventionally used piston or turboprop engine-powered general aviation aircraft.

It was observed that the demand for factory-built aircraft was greater than the kit-built ones. However, with the growing ease of building aircraft from kits and the information availability, this trend is fast-changing. In 2020, kit-built experienced higher registrations compared to factory-built ones. With the growing demand for light airplanes, several manufacturers are introducing newer generation aircraft. For instance, at the start of 2021, Terrafugia announced that FAA granted a special airworthiness certificate to certify its transition roadable airplane in the light-sport category (S-LSA), making the vehicle legal for flight. Terrafugia plans to produce and sell initial flight-only versions and will further develop the design to commercialize the aircraft by 2022. Such developments are expected to drive market growth during the forecast period.

Europe is Expected to be the Largest Market During the Forecast Period

Currently, Europe has the highest market share revenue, and it is expected to continue its domination during the forecast period. The region features several tourist spots and favorable geographies for light-sport aircraft activities. With the growing adoption of these aircraft, aviation regulatory bodies in the region are introducing new regulations to support the industry's growth and encourage new LSA procurements and operations. In 2020, EASA (the European Safety Agency) started allowing 600 kg ultralights, equivalent to US LSAs in Europe.

Ultralights flying at lower MTOW restrictions will only be able to upgrade their weight class if they are recertified. However, as of mid-2021, some national regulators in Europe were not allowing this recertification, while others welcomed the change. On the other hand, EASA has also made a concession to allow ultralight (and sailplane) to be used toward PPL SEP (and LAPL license) renewals. This is expected to help the pilots who predominantly fly ultralight aircraft. Several new aircraft manufacturers have initiated operations during the last decade in the region. Hence, many new LSA models have been released recently to cater to the increasing demand. On this note, Flight Design General Aviation GmbH launched the CTLS 2020 Sport Edition in April 2020. The CTLS 2020 features technical and aerodynamic upgrades while offering improved exteriors and interiors. Such developments are expected to drive market growth in the region during the forecast period.

Light-sport Aircraft Industry Overview

The light-sport aircraft market is fragmented, with the presence of many local and regional aircraft manufacturers that provide light-sport aircraft models for leisure and flight training markets. Some prominent players in the light sport aircraft market are Costruzioni Aeronautiche Tecnam SpA (Tecnam), Cub Crafters Inc., Jabiru Aircraft Pty Ltd, Zenith Aircraft Company, and Van's Aircraft Inc. The players in the market are introducing new aircraft models. They are being certified by the Federal Aviation Administration and the European Union Aviation Safety Agency to expand their geographic presence and sales. For instance, Tecnam received certification under the new German 600kg rules for its P2002 Sierra MkII and P92 Echo MkII light aircraft in February 2020 and November 2020, respectively. The German Type approval is also recognized in other European countries. On the other hand, companies are also investing in developing new aircraft with the latest propulsion technologies, like hybrid-electric propulsion systems, to enhance their presence in the market further. Such developments are expected to make the market more competitive in the years to come.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of Study

- 1.3 Currency Conversion Rates for USD

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

- 3.1 Market Size and Forecast, Global, 2018-2027

- 3.2 Market Share by Type, 2021

- 3.3 Market Share by Geography, 2021

- 3.4 Structure of the Market and Key Participants

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size and Forecast by Value - USD million, 2018-2027)

- 5.1 Type

- 5.1.1 Airplane

- 5.1.2 Seaplane

- 5.2 Geography

- 5.2.1 North America

- 5.2.2 Europe

- 5.2.3 Asia-Pacific

- 5.2.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Costruzioni Aeronautiche TECNAM SpA

- 6.2.2 Pipistrel d.o.o

- 6.2.3 ICON Aircraft

- 6.2.4 Cub Crafters Inc.

- 6.2.5 Czech Aircraft Group SRO

- 6.2.6 Paradise Aero Industry

- 6.2.7 Van's Aircraft Inc.

- 6.2.8 Flight Design General Aviation GmbH

- 6.2.9 JMB Aircraft s.r.o.

- 6.2.10 Jabiru Aircraft Pty Ltd

- 6.2.11 TL-ULTRALIGHT s.r.o.

- 6.2.12 American Legend Aircraft Company

- 6.2.13 Stemme Production GmbH

- 6.2.14 Aeropro s.r.o.

- 6.2.15 Zenith Aircraft Company