アンチドローン:市場シェア分析、産業動向・統計データ、成長予測(2026年~2031年)

Anti-Drone - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

- 発行日

- ページ情報

- 英文 155 Pages

- 納期

- 2~3営業日

- 商品コード

- 2035101

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

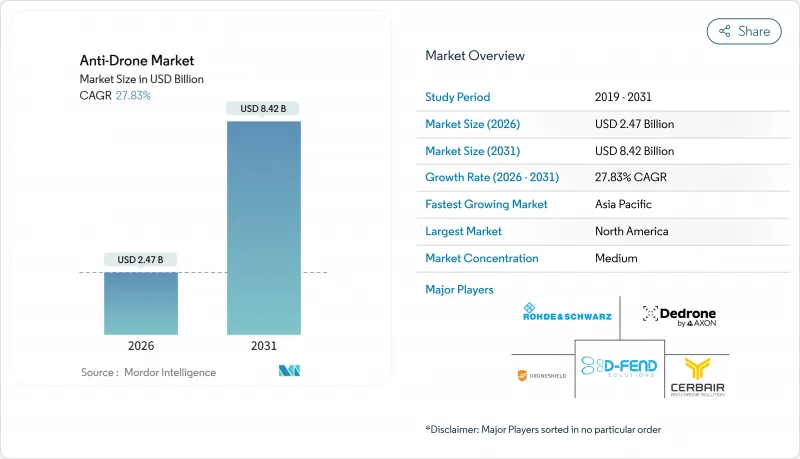

アンチドローン(ドローン対策)の市場規模は2026年に24億7,000万米ドルと評価され、商業事業者、重要インフラ管理者、および国土安全保障機関が小型無人航空システムの急速な普及に対抗する動きを進める中、CAGR27.83%で拡大し、2031年までに84億2,000万米ドルに達すると予測されています。

需要の勢いは、規制要件の統合、空域への侵入の急増、そして誤報率を低減しつつ検知範囲の識別精度を向上させるAI搭載のセンサーフュージョンの成熟に起因しています。検知および対策機能をソフトウェア定義型のサービスベースのソリューションに統合したベンダーは、スタジアム、刑務所、一時的な会場において、長年の課題であった資本予算の障壁に対処し、調達サイクルを短縮しています。同時に、特に東欧や中東における地政学的リスクの高まりが公共部門の支出拡大を促しており、これが民間施設への技術普及を加速させています。全体として、アンチドローン市場は、規制、脅威の深刻化、技術の融合からなる多層的な成長エンジンの恩恵を受けており、これにより、裁量的なセキュリティ予算が削減された場合でも、構造的な強靭性が確保されています。

世界のアンチドローン市場の動向と洞察

民間資産を脅かす低価格商用ドローンの普及

500米ドル未満の民生用ドローンは、現在4K動画の撮影や30分間の飛行が可能となっており、悪意のある者がわずかな技術で情報を収集したり、物資を投下したりできるようになっています。2024年のFAA(米連邦航空局)の月次インシデント記録では、空港でのドローン発見件数が100件を超え、前年比40%増となりました。また、2025年9月には、コペンハーゲン空港で正体不明のクアッドコプターが敷地内に侵入したため、90分間にわたり運航が停止されました。英国の刑務所では2024年に、密輸品を運ぶドローンの侵入が347件記録され、これを受けて法務省は2026年半ばまでに、すべてのカテゴリーA施設に固定式の対UAS(無人航空機システム)設備を設置するよう命令を出しました。その不均衡は顕著です。400米ドルのドローンが数百万米ドル規模の施設を機能停止に追い込み、運営者に多層的な検知・対策体制の導入を余儀なくさせているのです。保険引受会社は2025年、標準的な財産保険からドローン関連の損害を除外し始めました。これにより、リスクにさらされている施設は、保険適用を維持するために対UAS技術への投資を事実上義務付けられることになりました。

ドローン検知に関するFAAおよびEUのU-Space規制の強化

2024年3月から施行されているFAAの「リモートID規則」では、重量250グラムを超えるドローンに対し識別データの送信を義務付けており、これにより空港や重要インフラの所有者には、コンプライアンスをリアルタイムで監視する暗黙の義務が生じています。EUでは、規則2021/664により、加盟国は2026年までに、協調型および非協調型の交通検知機能を統合したU-Space回廊を整備することが義務付けられています。これらの政策により責任の所在が変化しています。侵入を検知できなかったオペレーターは、免許更新のリスクや保険料の値上げに直面することになります。各国の航空当局は現在、運用許可を実証済みのアンチドローン能力と結びつけることを常態化しており、これにより調達スケジュールが短縮され、ソフトウェア定義型で更新対応可能なプラットフォームを提供するベンダーが優遇されるようになっています。

RFジャミングおよび物理的排除の法的な曖昧さ

米国の法律では、連邦政府以外の主体によるRFジャマーの使用が禁止されています。しかし、国土安全保障省(DHS)の監督下にある連邦通信委員会(FCC)が発行する実験用ライセンスにより、限定的な使用が許可されています。この手続きには1年を要する場合があります。EUの無線機器指令も意図的な干渉を制限しており、商業施設はサイバーによる制御奪取や、安全性や不法行為責任に関する懸念を招く物理的排除手段へと向かっています。ネット捕獲型ドローンや迎撃弾は第三者への被害リスクを伴いますが、免責特例を認める法域はほとんどありません。このような法規制のばらつきは、無力化技術の商業的導入を妨げ、差し迫った脅威を解決できない「検知のみ」のシステムへの資本流入を招いています。

セグメント分析

無力化システムは、2026年から2031年にかけてCAGR27.65%で拡大すると予測されており、2025年の収益の53.95%を占めた検知のみのソリューションの優位性を徐々に侵食していく見込みです。航空および通信規制当局が、サイバー乗っ取りや付随的被害の少ない物理的迎撃システムに対する条件付き承認を与え始めたことで、この移行は加速しています。Anduril社の再利用型迎撃機「Roadrunner」は、米国陸軍の試験において95%の撃墜確率を実証し、使い捨て型のネット捕獲ソリューションと比較して、1回の交戦あたりのコストを1万米ドル未満に削減しました。D-Fend Solutions社の「EnforceAir2」は、GPSスプーフィングを用いて不正ドローンを安全着陸ゾーンへ誘導し、欧州の管轄区域におけるRFジャミング禁止規制を回避しています。検知機能は依然として重要ですが、保険会社は2025年より、自律的な対策を実証した施設に対して保険料を10%から15%引き下げるようになり、資本配分の決定が無力化能力へと傾きつつあります。

検知ベンダー各社は、ハードウェアの増設ではなく、分析機能や機械学習(ML)分類器を組み込むことでこれに対応しています。Dedrone社のRF-EO融合センサーはVerizonのプライベートLTEコアに統合され、初期投資を相殺するサブスクリプション方式の価格設定を可能にしています。Epirus社の20kWマイクロ波エフェクターのような指向性エネルギーシステムは、防衛分野の顧客を惹きつけていますが、30kVAの電力要件と200万米ドルの単価のため、民間市場では依然としてニッチな存在にとどまっています。2026年から2031年にかけて、アンチドローン市場は管轄区域によって二極化すると予想されます。規制の厳しい地域では検知機能のみが採用され、法的責任の枠組みが法改正よりも急速に進化する地域では、検知と無力化を統合したパッケージが採用されるでしょう。

2025年には、空港、原子力発電所、石油精製所などがセンサー領域の重複による24時間365日の監視を必要としているため、据置型プラットフォームが売上高の39.85%を占めました。それでも、イベント主導型のセキュリティ契約の増加を反映して、ポータブルシステムのCAGRは28.59%に達すると予測されています。DroneShield社の「DroneSentry-X Mk2」は、重量35kgで15分以内に展開可能であり、2024年パリオリンピックおよび2025年世界経済フォーラムで警備を担当しました。

レンタル経済性はポータブル型システムの普及を後押ししています。オペレーターは、固定式アレイの導入に50万米ドルの初期費用を支払うのに対し、ポータブル型なら週1万~2万米ドルで済むため、これは「C-UAS-as-a-Service(サービスとしてのUAS対策)」というパラダイムに沿ったものです。重要な施設におけるアンチドローン市場の規模では、依然として固定式設置が主流です。これは、タレスの「Falcon Shield」が提供するような10kmのレーダー探知範囲が、混雑した飛行場では不可欠であるためです。モジュール式設計は両者の境界を曖昧にしています。サーブの「Giraffe 1X」はISOコンテナで出荷され、屋上やトラックの荷台にボルトで固定できるため、半恒久的な使用事例を満たします。

地域別分析

北米は2025年に世界売上高の40.55%を占め、これは米国国土安全保障省(DHS)の契約および連邦航空局(FAA)によるリモートIDの施行に牽引されたものです。同地域は2031年までCAGR25.8%を記録すると予測されていますが、早期導入者が新規設置からソフトウェアアップグレードへと移行するにつれ、世界平均をわずかに下回る見込みです。米国の原子力発電所は、NRC(米原子力規制委員会)の指針に基づき、2027年までに周辺検知システムを設置する必要があります。一方、GAO(米政府監査院)が検証した空港のパイロットプロジェクトでは、電波が密集した環境における誤検知を減らすマルチセンサーアーキテクチャが強化されています。カナダの動きは緩やかですが、カナダ運輸省(Transport Canada)の2025年草案では、対UAS(無人航空機システム)対策の適用範囲がバンクーバー、トロント、モントリオールの各空港に拡大されています。メキシコではまだ導入初期段階ですが、カルテルによるドローン事件を契機に、2024年後半にグアダラハラとティフアナでパイロット導入が開始されました。

アジア太平洋は、2026年から2031年にかけてCAGR27.11%という最も高い成長率を示すと予想されています。これは、インドの「デジタル・スカイ」プラットフォームによるドローン登録の義務化、中国によるスマートシティ監視の拡大、そして日本による物理的迎撃システムの規制緩和によるものです。インドは2024年、商用対UASシステムの設置に関する事前承認のボトルネックを解消し、プロジェクトのスケジュールを加速させました。中国の国有空港運営会社は、現在50以上の主要ハブ空港でRF-EO融合システムが稼働していることを明らかにしました。これらは主にCETCを含む国内ベンダーから調達されたものです。日本は2024年、成田空港向けに三菱電機に契約を授与し、レーダー、EO、およびネット迎撃システムを統合しました。韓国における全国的な5Gの展開はRF検知を複雑にしていますが、仁川空港でのAIの再学習により、2025年の試験運用において誤警報率は10%未満に低減されました。

欧州は2025年の売上高の約28%を占めており、主にU-spaceへの準拠や、2025年のコペンハーゲンでの空港閉鎖といった注目度の高い事件を背景に、2031年までCAGR26.5%で成長すると予想されています。英国は導入をリードしており、年間旅客数500万人を超える空港は24時間365日のカバレッジを維持しなければならず、カテゴリーAの刑務所は2026年半ばまでにシステムを導入する必要があります。ドイツは2025年、製油所を対象としたRF妨害の適用除外措置を設け、EU全体の規制緩和につながる可能性があります。フランスは2024年パリオリンピック期間中にC-UAS-as-a-Service(サービスとしての対UASシステム)の実証を行い、迅速な再配備能力をアピールしたタレス社とドローンシールド社に契約を授与しました。中東およびアフリカ地域は、サウジアラビアのNEOMやUAEがスマートシティの青写真に検知層を統合し、さらに2024年のGACA規則によりすべての商業空港でのシステム導入が義務付けられたことを受け、CAGR26.8%で拡大すると予想されています。南米は依然として市場規模が最も小さいもの、ブラジルの2025年ANACガイドラインがサンパウロのグアルーリョス空港を筆頭とする調達ブームを引き起こしたことで、勢いを見せています。

その他の特典:

- Excel形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 分析の前提条件と市場の定義

- 分析範囲

第2章 分析手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 民間資産を脅かす低コスト商用ドローンの普及

- ドローン検知に関するFAAおよびEUのU-space規制の厳格化

- 重要インフラ(エネルギー、空港)へのドローンの侵入

- AIを活用したマルチセンサー融合により、検知精度が向上します

- C-UAS-as-a-Serviceは会場運営者の設備投資(CapEx)を削減します

- プライベート5Gキャンパスネットワークは、パッシブRF検知を可能にします

- 市場抑制要因

- RFジャミング・物理的排除の法的曖昧さ

- 5Gが密集した都市部における高い誤報率

- 広域音響・EO監視に関するプライバシーの懸念

- ドローンとサイト運営者間の責任の分散

- バリューチェーン分析

- 規制とテクノロジーの展望

- ポーターのファイブフォース分析

- サプライヤーの交渉力

- バイヤーの交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の競合関係

第5章 市場規模と成長予測

- 技術別

- 検知システム

- 無力化・対策システム

- プラットフォームの種類別

- 据置型

- 携帯型

- 最終用途別

- 民間

- 国土安全保障・法執行機関

- 運用範囲別

- 短距離(1 km未満)

- 中距離(1~5 km)

- 長距離(5 km超)

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- フランス

- ドイツ

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋

- 南米

- ブラジル

- その他南米

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- その他中東

- アフリカ

- 南アフリカ

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Dedrone Holdings, Inc.

- CERBAIR

- D-Fend Solutions AD Ltd.

- DroneShield Group Pty Ltd.

- Rohde & Schwarz GmbH & Co. KG

- Thales Group

- QinetiQ Group

- Saab AB

- Anduril Industries, Inc.

- SRC Inc.

- DeTect, Inc.

- CACI International Inc.

- Honeywell International Inc.

- Meteksan Defence Industry Inc.

- OpenWorks Engineering Ltd.

- Rheinmetall AG

- Northrop Grumman Corporation

- Leonardo S.p.A.

- Terma Group

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 155 Pages

- 納期

- 2~3営業日