|

市場調査レポート

商品コード

1851567

eクリニカルソリューション:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)EClinical Solutions - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| eクリニカルソリューション:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月28日

発行: Mordor Intelligence

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

概要

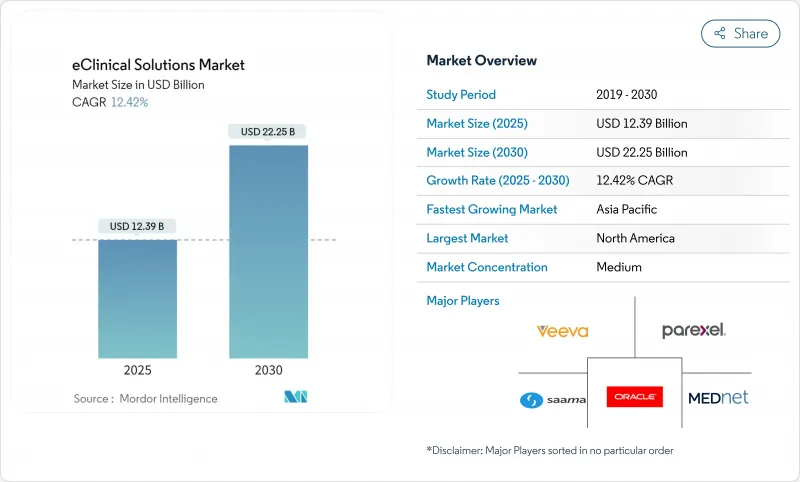

eクリニカルソリューション市場は、2025年に123億9,000万米ドルに達し、2030年には222億5,000万米ドルに達する見込みです。

このランレートは、完全なデジタル治験の実施が、オプション的な効率化から競合薬開発の中核要件へと変化したことを示しています。スポンサーは現在、より大規模なマルチモーダルデータセットをよりグローバルな施設に送信し、より厳しい情報開示期限に直面しているため、高度なキャプチャー、モニタリング、分析システムが不可欠となっています。分散型臨床試験やハイブリッド臨床試験が緊急回避策から主流設計に移行し、参加者、モニター、統計担当者、規制当局をつなぐ統合プラットフォームへの需要が加速する中、ほぼリアルタイムの接続性はさらに価値を増しています。Tier-1ベンダーは、電子データ収集(EDC)、電子臨床転帰評価(eCOA)、無作為化および治験薬供給管理(RTSM)、安全性報告を単一の契約にバンドルしているため、価格決定ダイナミクスは、試験のライフサイクルに適合し、よりスリムなバイオテクノロジー予算をサポートするサブスクリプションモデルを支持しています。

世界のeクリニカルソリューション市場の動向と洞察

ヘルスケア業界の膨大なデータ量

臨床試験データの量は急増し、スポンサーは自動品質チェック、自然言語処理、予測分析をコアEDCプラットフォームに直接組み込むようになっています。IQVIAの報告によると、AIによる非構造化ソースのレビューにより、監査対応能力を維持しながらデータクリーニングサイクルを半減できます。その結果、データサイエンスチームは、単に最初の患者が入ってきた後ではなく、プロトコルの構築中に関与するようになり、下流の相互運用性が確保されるようになりました。クラウドストレージの予算は、弾力的な容量がハードウェアの購入サイクルを上回るにつれて、オンプレミスの支出を上回っています。かつてはニッチであった解析のフレームワークが、今では炎症や代謝のパイプライン全体で再現されるようになっています。被験者一人当たりのデータが増加するにつれて、eクリニカルソリューション市場は治療領域の焦点に依存しない安定した追い風を得る。

臨床試験におけるソフトウェア・ソリューションの採用拡大

スポンサーは日常的に1つの治験につき3つ以上の個別のeクリニカルアプリケーションを使い分けていますが、断片的なログインと同期されていないデータフローが明確なボトルネックになっています。Veevaの2025年ロードマップでは、開始、モニタリング、申請ワークフローを統合するシングルサインオン環境に対する需要の高まりを紹介しています。早期導入企業では、モジュール間の重複データ入力がなくなり、検証コストも削減できるため、プロトコルの最終化サイクルが大幅に短縮されると報告しています。統合されたスイートは現在、ベスト・オブ・ブリードの購買を凌駕しており、ガバナンスチームは手作業によるクエリーから高度な統計プログラミングに人員をシフトすることができます。その結果、プラットフォームの複数年契約が増加し、eクリニカルソリューション市場において、散発的なライセンス費用が予測可能なSaaS収益に変換されるようになりました。

高い導入コスト

包括的なプラットフォームのロールアウトには、検証、統合、マルチユーザートレーニングを考慮すると、7桁を超える予算が必要になることが多いです。Merativeのベンチマークによると、資金繰りの厳しいスポンサーは段階的な導入を採用しており、まずコアとなるEDCを導入し、後からRTSMやeTMFをレイヤー化しています。段階的な導入は初期費用を抑えることができる反面、プロジェクトのスケジュールを延ばし、完全なスイートがもたらす生産性の向上を遅らせることになります。そのため、柔軟性の高い消費ベースの価格設定を提供するベンダーは、デジタル化を先延ばしにしていた顧客を獲得することができます。とはいえ、参入コストの高さは依然として中小のバイオテクノロジー企業や学術スポンサーに重くのしかかり、リソースに制約のある環境におけるeクリニカルソリューション市場の成長を抑制しています。

セグメント分析

2024年のeクリニカルソリューション市場規模は、電子データ収集および臨床データ管理システムが最大で、試験開始時の普遍的な展開により総売上の33.13%を占めています。スポンサーがシステムに慣れ親しみ、中間解析の前に異常を知らせるリスクベースの統合モニタリングダッシュボードを高く評価しているため、ライセンス更新は依然として高い水準にあります。市場は現在、基本的なデータ入力よりも組み込まれた予測クエリーに価値を置いており、プレミアム価格を要求するAIを組み込んだアップグレードへのシフトを生み出しています。EDCをRTSMや安全性モジュールと事前に統合しているベンダーは、スイッチングコストをさらに引き上げ、リーダーとしての地位を固めています。

電子臨床転帰評価プラットフォームは、最も急速に拡大しているサブセグメントであり、患者中心主義がレトリックから要件に移行するにつれて、2030年までのCAGRは15.24%になると予想されます。Medableの機器ビルダーは、心理測定ツールやQOLツールをドラッグ・アンド・ドロップで作成でき、手作業でマッピングすることなくEDCのテーブルに直接入力できます。スポンサーは、シームレスなハンドオフを高く評価しています。これは、調整サイクルを数週間短縮し、リアルタイムのダッシュボードレビューをサポートするためです。分散型臨床試験が普及するにつれ、eCOA機能がプラットフォーム選択全体の決め手となることが多く、eクリニカルソリューション市場内のフルスイートベンダーの収益増を後押ししています。

クラウドベースの導入は、2024年のデリバリーモード別eクリニカルソリューション市場シェアで48.62%と最大を占め、2030年までのCAGRは14.58%と予測されます。マルチテナントのSaaSモデルは、即時の拡張性、自動バージョンアップ、監査ログを提供し、規制当局はオンプレミスの管理と同等とみなすようになってきています。自社所有のハードウェアから移行するスポンサーは、メンテナンス時間を2桁削減し、ITチームを分析業務に振り向けることができます。参入コストの低減は、小規模なバイオテクノロジー・スポンサーが試験のマイルストーンに合わせてキャッシュ・バーンを維持するのにも役立ち、クラウドの牽引力を強めています。

ウェブホストのシングルテナント環境は、30%半ばのシェアを維持し、マルチテナント・アーキテクチャへの移行に消極的な組織の移行オプションとして機能しています。このような環境は、インフラ所有の負担を軽減しながらも、リスク回避を好む品質グループに好まれる隔離性を提供します。しかし、最近のテナントレベルの暗号化と専用キー管理の進歩は、ウェブホスト型とSaaSのセキュリティギャップを縮めています。今後、マルチテナント型への移行が進むと予想されるが、保守的なスポンサーは、eクリニカルソリューション市場においてウェブホスティング型ベンダーを維持するニッチを維持すると思われます。

地域分析

北米は2024年に最大のeクリニカルソリューション市場規模を維持し、世界売上高の49.11%に寄与しています。その理由は、豊富な資本プール、デジタル署名の早期規制受け入れ、経験豊富な治験施設の密集にあります。ベンダーは、米国とカナダで新しいAIモジュールを最初に発売することが多いです。これは、現地のデータ・ガバナンス規範が迅速な反復をサポートしているためです。市場が成熟しているにもかかわらず、スポンサーが従来のオンプレミス導入をSaaSに移行し、検査準備を迅速化する高度なアナリティクスを追求しているため、2桁台の更新成長が続いています。

アジア太平洋地域は最も速い成長軌道を示し、2030年までのCAGRは14.84%になると予想されます。これは、世界のスポンサーが大規模な患者プールとコスト効率の高い施設ネットワークへのアクセスを求めて、募集を東にシフトしているためです。中国、韓国、インドの政府は、国内のバイオファーマを積極的に支援し、導入のハードルを下げるクラウドインフラの助成金を提供しています。各地域のベンダーは現地の言語や個人情報保護法に合わせてインターフェイスを微調整し、欧米の既存ベンダーに対する競合圧力を高め、eクリニカルソリューション市場内のサプライヤー基盤を多様化しています。

欧州は世界売上高の約4分の1を占め、EU臨床試験規則によるハーモナイゼーションの恩恵を受け、複数国への申請が効率化されています。この地域の厳格なデータプライバシー規則は、後にグローバルに展開されるセキュリティ機能の実験場として機能しています。ドイツ、北欧、オランダでは、電子患者日誌やeConsentの採用が増加しており、患者向けテクノロジーに対する文化的受容性を示しています。規制当局の監視が厳しいと、販売サイクルが長くなる一方で、スポンサーがプラットフォームのスコープにコンプライアンスに関するコミットメントを組み込むため、長期的な契約価値が高まる。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- ヘルスケア業界からの膨大なデータ収集

- スケーラブルなクラウドプラットフォームを必要とするAPACにおけるフェーズII/IIIオンコロジー試験の急増

- 臨床試験におけるソフトウェアソリューションの導入拡大

- 拡大するバイオ医薬品の研究開発投資

- 患者中心・分散型モデルへの急速なシフト

- グローバルな臨床試験活動の拡大

- 市場抑制要因

- 高い導入コスト

- レガシーモジュールと最新eクリニカルモジュール間のデータ相互運用性のギャップ

- 新興市場における認定クリニカルデータマネージャーの不足

- 高まるサイバーセキュリティと患者データ漏洩の懸念

- バリューチェーン分析

- 規制と技術的展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力/消費者

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品別

- 電子データ収集(EDC)と臨床データ管理システム(CDMS)

- 臨床試験管理システム(CTMS)

- 無作為化・治験薬供給管理(IRT/RTSM)

- 電子臨床アウトカム評価(eCOA/ePRO)

- 臨床分析&データ統合プラットフォーム

- 安全性&ファーマコビジランス・ソリューション

- 電子治験マスターファイル(eTMF)

- その他の製品

- 配送方法別

- クラウドベース(SaaS)

- ウェブホスティング(オンデマンド)

- オンプレミス

- 臨床試験フェーズ別

- 第1フェーズ

- 第2フェーズ

- 第3フェーズ

- 第4フェーズ

- エンドユーザー別

- 製薬・バイオテクノロジー企業

- 開発業務受託機関(CRO)

- 医療機器メーカー

- 学術・研究機関

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 中東

- GCC

- 南アフリカ

- その他中東

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 市場シェア分析

- 企業プロファイル

- Oracle Corporation

- Dassault Systemes(Medidata Solutions)

- Veeva Systems

- Clario(BioClinica)

- IQVIA Holdings Inc.

- PAREXEL International(Calyx)

- Covance(Labcorp Drug Development)

- Signant Health

- eClinical Solutions LLC

- Saama Technologies, Inc.

- Datatrak International Inc.

- Medrio, Inc.

- Castor EDC

- Mednet Solutions

- ArisGlobal

- Anju Software Inc.

- MasterControl, Inc.

- OpenClinica, LLC

- ClinCapture, Inc.

- Medable Inc.

- TransPerfect Life Sciencesー