ロボット用センサー:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

Robotic Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)- 発行日

- ページ情報

- 英文 136 Pages

- 納期

- 2~3営業日

- 商品コード

- 1910597

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

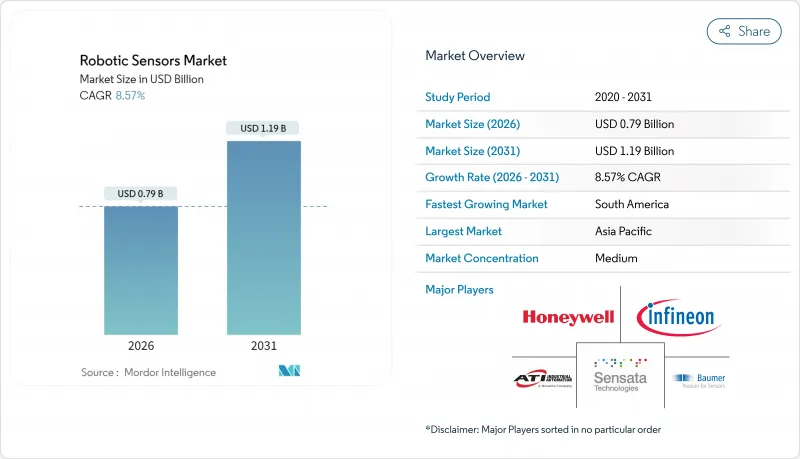

ロボット用センサー市場は、2025年の7億3,000万米ドルから2026年には7億9,000万米ドルへ成長し、2026年から2031年にかけてCAGR8.57%で推移し、2031年までに11億9,000万米ドルに達すると予測されております。

この成長は、産業用ロボットの導入台数が過去最高を記録していること、協働ロボットおよびヒューマノイドプラットフォームの急速な普及、そして知覚精度と応答時間を向上させるエッジAIモジュールの着実な導入に起因しています。力・トルクデバイスは精密組立ラインを支え、一方、ビジョンシステムは深層学習モデルがクラウドからロボットアームへ移行するにつれて加速しています。半導体メーカーは現在、センシング、処理、安全ロジックを単一チップに統合しており、これにより工場は低遅延化と優れたサイバーフィジカルレジリエンスを実現しています。自動車、電気自動車、医療分野のエンドユーザーは、歩留まり、トレーサビリティ、人と機械の協働を改善するため、マルチモーダルセンシングへの投資を強化しています。地域別では、アジア太平洋地域の密集した製造拠点と政策インセンティブが規模の経済を支える一方、南米の自動化追いつき需要が高成長の基盤を提供しています。

世界のロボットセンサー市場の動向と洞察

産業用ロボットの設置台数が過去最高を記録

2024年に世界の稼働台数が400万台を突破したことで、メーカーはエンコーダを超え、ビジョン、力覚、触覚モダリティまでを含む高度なセンシングスイートの採用を迫られています。ファナックの500i-A CNC制御装置(CPUスループット2.7倍)は、高速なオンボードコンピューティングが複雑なセンサーストリームをリアルタイムで処理する実例を示しています。協働セルは冗長安全センシングの需要を拡大させており、デルタのD-Botコボットは積載量に特化したプラグアンドプレイ式センサーパッケージにより統合を簡素化しています。設置台数の増加は高度な知覚技術の投資回収期間を短縮し、ロボットセンサー市場全体で受注を確保しています。

センサー搭載自律移動ロボット(AMR)に対するEC物流需要

堅調なオンライン小売により、2024年の世界の移動ロボット市場規模は45億米ドルに達し、動的な倉庫内における広角知覚、マッピング、およびパッケージ品質評価の必要性を促進しています。Sonair社などの低コスト3D超音波アレイは180×180度のカバレッジを実現し、LiDARを最大80%下回る価格設定により、中規模フルフィルメントセンターの資本障壁を低減します。AI強化ビジョンはパレットラック、フォークリフト、従業員の服装を識別可能となり、稼働時間とスループットを向上させます。タッチ対応グリッパーにより、AMR(自律移動ロボット)が壊れやすいSKU(在庫管理単位)を扱えるようになり、使用事例が拡大し、センサーの需要量が増加しています。

MEMSの供給網における継続的な変動性

ガリウムとアンチモンの貿易制限に加え、アジアのファウンダリにおける自然災害リスクがリードタイムを圧迫し、ダイレベルのコストを押し上げております。Sourceability社は2026年までウエハースタートのボトルネックが継続すると予測しており、高ピン数センサーASICの供給が逼迫する見込みです。労働力不足も不確実性を増大させており、一部のOEMメーカーはデュアルソーシングやバックエンドパッケージングの移転を検討しておりますが、こうした動きは資本集約度と運用上の複雑性を高める結果となっております。

セグメント分析

ビジョンセンサーは2026年から2031年にかけて13.27%のCAGRを記録し、他の全カテゴリーを上回る見込みです。一方、フォース・トルクデバイスは2025年時点でロボットセンサー市場の27.62%のシェアを維持しました。高速視覚検査やピックアンドプレース作業の普及により、推論遅延を30ミリ秒未満に圧縮するオンボードGPUやASICへの投資が正当化されています。カメラ価格の低下に伴い、中堅OEMメーカーでも深度推定に対応するためデュアルセンサーステレオ装置を採用する動きが見られます。力センシングは、プレスフィット、バリ取り、電子コネクタ組立において依然として不可欠であり、サブニュートン単位の精度が歩留まりを保証します。コグネックス社の2023年売上高8億3,750万米ドルは、設備投資が回復する際に、機械視覚ハードウェアに対する周期的な需要が依然として堅調であることを示しています。

センサーの小型化により、近接・温度・ビジョンモジュールをロボットの狭い手首部に集約でき、配線と電磁ノイズを削減できます。XELA Robotics社のuSkinのような0.1グラムフォース感度を持つ触覚アレイはグリッパーの器用さを向上させますが、ロボットセンサー市場では依然として「その他」カテゴリーに位置付けられています。ステレオビジョン、IMU、力ベクトルの融合は、不規則な部品の組立工程におけるコンプライアンス制御を強化します。この機能は、ウェアラブルデバイス生産ラインやカスタム整形外科機器において高く評価されています。標準化されたM12コネクタとPower-over-Ethernet(PoE)は設置を効率化し、中小企業の参入障壁を低減します。予測期間において、モジュール式でAI対応のビジョンスイートを提供するサプライヤーは、このセグメントにおけるロボットセンサー市場の増加分において、相対的に大きなシェアを獲得すると見込まれます。

産業用ロボットは従来から需要の基盤となっており、2025年のロボットセンサー市場規模の54.62%を占めます。溶接、塗装、電子機器組立における確固たる役割が、安定した更新サイクルを保証しています。しかしながら、ヒューマノイドプラットフォームは、持続的なベンチャーキャピタル流入と部品コストの低下に後押しされ、2031年までCAGR36.7%で成長を牽引すると予測されます。Tacta Systems社の資金調達は、安全性と器用さが人間並みに達した時点で、ヒューマノイドが物流、小売、高齢者介護の課題を解決できるという確信を裏付けています。

協働ロボットは、柔軟なライン変更を必要とし、大規模な防護設備を導入できない中規模工場での採用を拡大し続けております。エッジAIサブシステムにより「ゼロプログラミング」ティーチモードが実現され、技術的ハードルが低下し、対象ユーザー層が拡大しております。病院や空港では、感染管理や旅客サービス業務に信頼性の高い知覚能力と繊細な操作が求められるため、業務用サービスロボットの導入が急増しています。安川電機「MOTOMAN NEXT」シリーズが実証する自己最適化動作計画は、状況認識能力の向上を目指すプラットフォームにおいてセンサー数を増加させる動向を示しています。将来的には、ヒューマノイドロボットの普及加速がロボットセンサー市場のさらなる多様化を促し、従来の産業用オートメーションを超えた新たな供給先市場を創出するでしょう。

地域別分析

2025年にはアジア太平洋地域が34.72%の収益シェアで首位を占めました。これは中国の産業高度化補助金、日本のSociety 5.0構想、韓国のメモリチップ投資ブームに支えられたものです。オムロンの8,761億円の純売上高は、センサー駆動型自動化に対する同地域の堅調な需要を裏付けています。MEMSファブへの近接性はリードタイムを短縮し、現地の一流自動車メーカーや電子機器大手が基盤需要を保証しています。ただし、チップ輸出規制をめぐる地政学的摩擦により、サプライチェーンの再構築と追加コストが発生する可能性があります。

欧州市場はドイツのインダストリー4.0ロードマップと厳格な安全基準に支えられ、認証済みセンシングシステムの需要が高まっています。SICK社の2024年売上高23億700万ユーロは、特に自動車・物流拠点における健全な成長勢いを示しています。南欧ではファナックのイベリア地域拡大に代表される協働ロボットの普及が進み、市場規模が拡大しています。北欧企業は洋上風力発電や鉱業分野で限界突破的な応用を推進しており、防塵防滴仕様で耐振動性に優れたセンサーが主流となっています。

北米はイノベーション中心地であり、米国研究所ではエッジAI知覚技術の精緻化が進み、カナダ鉱山では自律搬送用頑丈センサーが採用されています。メキシコのニアショアリング動向により生産ラインがバヒオ回廊に集積し、コスト効率の高いセンシング需要を牽引しています。南米は設置ベースこそ小さいもの、ブラジル自動車メーカー、アルゼンチン穀物取扱業者、チリリチウム精製業者が労働力不足の解消とESG監査対応のために自動化を進めることで、10.45%という最速のCAGRを達成する見込みです。地域開発銀行と多国籍企業が共同でパイロットプロジェクトを資金援助し、ロボットセンサー市場全体に長期的なセンサー需要の種を蒔いています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストサポート(3ヶ月間)

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 産業用ロボットの設置台数が過去最高水準に達しました

- センサー搭載自律移動ロボット(AMR)に対する電子商取引物流需要

- 六軸力・トルクセンサーの急激な価格下落

- 人間とロボットの協働に関する規制上の優遇措置

- ヒューマノイドロボット向けエッジAIセンサー融合モジュール

- オープンソースROS2ハードウェアリファレンスデザイン

- 市場抑制要因

- 持続的なMEMSサプライチェーンの変動性

- 新興市場における中小企業の設備投資障壁

- スマートセンサー向けサイバーセキュリティ認証費用

- 高度な触覚ICに対する輸出管理上の制限

- バリュー/サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- センサータイプ別

- 力およびトルクセンサー

- ビジョンセンサー

- 近接センサー

- 位置/エンコーダー

- 温度センサー

- 圧力センサー

- その他(触覚式、LiDAR、超音波式)

- ロボットタイプ別

- 産業用ロボット

- 協働ロボット(コボット)

- サービスロボット- プロフェッショナル向け

- サービスロボット- 家庭用

- ヒューマノイドロボット

- エンドユーザー業界別

- 自動車および電気自動車(EV)

- 電子機器および半導体

- 物流・倉庫業

- 食品・飲料

- 医療・医療機器

- その他産業(金属、プラスチックなど)

- 検知技術別

- ひずみゲージ

- 容量式

- 光学式(CMOS、LiDAR)

- 磁気及びホール効果

- 圧電

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 中東

- イスラエル

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- その他アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- ATI Industrial Automation(Novanta Inc.)

- Bota Systems AG

- Baumer Group

- FANUC Corporation

- FUTEK Advanced Sensor Technology, Inc.

- Honeywell International Inc.

- Infineon Technologies AG

- OMRON Corporation

- Sensata Technologies Holding plc

- TE Connectivity Ltd.

- Tekscan, Inc.

- Sick AG

- Keyence Corporation

- Cognex Corporation

- Epson Robotics(Seiko Epson Corp.)

- Yaskawa Electric Corporation

- Delta Electronics, Inc.

- DENSO Wave Incorporated

- Bosch Rexroth AG

- Rockwell Automation, Inc.

- Schunk GmbH and Co. KG

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 136 Pages

- 納期

- 2~3営業日