|

市場調査レポート

商品コード

1433795

特殊シリカ:市場シェア分析、産業動向・統計、成長予測(2024~2029年)Specialty Silica - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 特殊シリカ:市場シェア分析、産業動向・統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

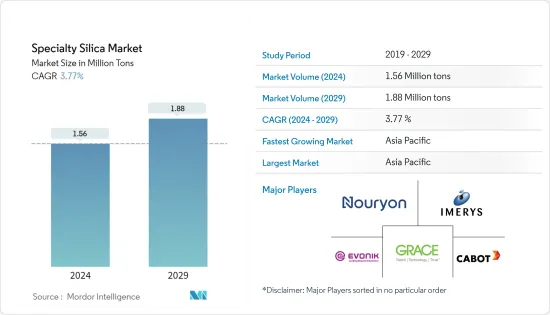

世界の特殊シリカの市場規模は、2024年に156万トンに達し、2024~2029年の予測期間中にCAGR 3.77%で成長し、2029年には188万トン達すると予測されています。

COVID-19は市場にマイナスの影響を与えました。パンデミックのシナリオのため、世界中のさまざまな政府がウイルスの蔓延を防ぐために封鎖措置を設けた。数多くの企業や工場が閉鎖され、世界の供給網が混乱しました。しかし、市場はCOVID-19の流行から回復し、急速に成長しています。

主なハイライト

- ゴム業界からの需要拡大が市場成長を牽引しています。さらに、パーソナルケア製品における特殊シリカの利用拡大も市場を押し上げています。

- しかし、特殊シリカの高価な性質と代替製品の入手可能性が市場成長の妨げになると予想されます。

- それでも、グリーンタイヤの台頭の高まりは、今後の市場にとって好機となると予測されます。

- アジア太平洋は、予測期間中、特殊シリカの最大かつ最も急成長している市場になると予想されます。

特殊シリカの市場動向

ゴム業界からの需要の増加

- 特殊シリカは一般的に液状シリコーンゴム(LSR)や高温加硫ゴム(HTV)に使用され、高い機械的強度と良好な電気絶縁性が要求されます。

- 工業用ゴム製品では、特殊シリカはコンベアベルトのヒステリシスロスを低減したり、着色ゴム粒子や接触性の良い製品の活性充填剤として使用されます。

- 米国経済分析局によると、2022年中の国別ゴム製品(プラスチック製品を含む)の付加価値は3,820億米ドル以上で、前年の付加価値を約11%上回りました。

- 特殊シリカは、純度が極めて高く吸湿性が低いため、主にタイヤ製造用ゴムに使用されています。ゴム製品よりも優れた電気特性を持っています。

- 北米では、OICA(Organisation Internationale des Constructeurs d'Automobiles)によると、2022年の自動車生産台数は1,480万台で、1,340万台と報告された2021年の生産台数に比べ9.88%増加しました。

- さらにOICAによると、2022年のドイツの自動車生産台数は370万台で、2021年同時期の330万台に比べて11%増加しました。

- Modern Tire Dealerによると、2022年の米国タイヤの総出荷量は約3億3,500万本でした。2022年に出荷されたタイヤの大半は交換用の乗用車用タイヤで、約2億2200万本でした。タイヤ業界の増加は、最終的にゴム業界からの需要を高め、それによって特殊シリカ市場に利益をもたらすと思われます。

- したがって、前述のすべての要因が予測期間中の世界市場を牽引すると予想されます。

アジア太平洋が市場を独占する

- 予測期間中、アジア太平洋が特殊シリカ市場を独占すると予想されます。中国、インド、日本などの国々では、タイヤ製造、工業用ゴム製造、塗料・コーティング、パーソナルケア業界などの用途からの需要が増加しているためです。

- 世界塗料・コーティング工業会によると、2022年のアジア太平洋の塗料・コーティング業界は630億米ドル規模になると推定されています。中国がこの地域の市場を独占し、CAGR 5.8%で成長しています。2022年には、中国市場は5.7%成長すると予想されています。現在の動向によると、中国の塗料・コーティングの総売上高は2022年に450億米ドルを超えます。東アジアでは、同国の市場シェアは78%と最大です。

- インドは2022年時点で世界第4位のゴム消費国です。インドの国民一人当たりのゴム使用量は現在1.2キログラムで、世界全体では3.2キログラムです。インドのゴム業界は約1万2,000インドルピー(~14億米ドル)の収益を上げています。タイヤ部門はインドのゴム生産量の大半を消費しており、国全体の生産量の半分以上を占めています。

- 同国におけるゴム業界の成長を受け、Japanese Yokohama Rubber CompanyであるYokohamaは2023年、8,200万米ドル(~679億インドルピー)を投資し、現地市場の需要増加に対応するため、インドにおける乗用車用タイヤの生産能力を拡大すると発表しました。Visakhapatnamの生産施設は2024年末までに完成し、操業を開始する予定です。

- さらに、中国は最大の自動車生産国であり消費国でもあります。 China Association of Automobile Manufacturers (CAAM)の報告によると、2022年の中国の自動車生産台数は前年比で約3.4%増加しました。2021年の自動車生産台数が2,608万台であったのに対し、2022年には約2,702万台が生産されました。この増加はタイヤ需要の増加につながり、特殊シリカ市場に影響を与えます。

- インドでは、ゴムの約12%が履物の生産に使用されています。インドのフットウェア業界は、今後数年間で4.5%の成長を遂げると推定されています。スポーツシューズのカテゴリーでは、ランニングシューズが最も消費されており、前年比1.5倍の急増となっています。マレーシアを代表するフットウェアブランドであるBataは、2023年末までにフランチャイズ店を500店舗オープンする計画を打ち出しています。

- Malaysian Rubber Boardによると、マレーシアのタイヤ製品の輸出は、2022年上半期に8億3,280万MYR(~1億8,890万米ドル)から8億8,320万MYR(~2億3,039万米ドル)へと6%の増加を記録しており、成長の余地があります。同協議会は、同国の輸出を促進するため、新たな投資、技術の進歩、より環境に優しい製品に一層注力しようとしています。

- したがって、このような市場動向はすべて、予測期間中に同地域の特殊シリカ市場の需要を促進すると予想されます。

特殊シリカ業界の概要

特殊シリカ市場は細分化されています。市場シェアの面では、現在少数の大手企業が市場を独占しています。特殊シリカ市場の主要企業には、W. R. Grace &Co.、Cabot Corporation、Imerys、Evonik Industries AG、Nouryonなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- ゴム業界からの需要拡大

- パーソナルケア製品における特殊シリカの利用の増加

- その他の促進要因

- 抑制要因

- 特殊シリカの高価な性質

- 市場における代替製品の入手可能性

- 業界バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション:市場規模(数量ベース)

- タイプ

- 沈殿シリカ

- シリカゲル

- ヒュームドシリカ

- コロイダルシリカ

- 溶融シリカ

- 用途

- ゴム

- パーソナルケア

- 食品・飼料

- 化学品

- プラスチック

- 塗料、コーティング剤、インク

- 金属・耐火物

- その他の用途

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- 3M(Ceradyne Inc.)

- Cabot Corporation

- Clariant

- Denka Company Limited

- Evonik Industries AG

- Fuji Silysia Chemical

- Fuso Chemical Co. Ltd

- Glassven C.A.

- Imerys

- Merck KGaA

- Nouryon

- Orisil

- Tata Chemicals

- W. R. Grace & Co.

- Wacker Chemie AG

第7章 市場機会と今後の動向

- グリーンタイヤの台頭

- その他の機会

The Specialty Silica Market size is estimated at 1.56 Million tons in 2024, and is expected to reach 1.88 Million tons by 2029, growing at a CAGR of 3.77% during the forecast period (2024-2029).

COVID-19 had a negative influence on the market. Because of the pandemic scenario, various governments around the world established lockdowns to prevent the virus from spreading. Numerous companies and factory closures had disrupted global supply networks. However, the market has recovered from the COVID-19 outbreak and is growing rapidly.

Key Highlights

- The growing demand from the rubber industry is notably driving market growth. Moreover, the increasing utilization of specialty silica in personal care products is also pushing the market forward.

- However, the expensive nature of specialized silica and the availability of substitute products is expected to hinder market growth.

- Nevertheless, the growing emergence of green tires is projected to act as an opportunity for the market in the future.

- The Asia-Pacific region is expected to be the largest and fastest-growing market for specialty silica during the forecast period.

Specialty Silica Market Trends

Increasing Demand from the Rubber Industry

- Specialty silica is commonly used in Liquid Silicone Rubber (LSR) and High-Temperature Vulcanized (HTV) rubber, which requires high mechanical strength and good electrical insulation.

- In industrial rubber goods, specialty silica is used for reducing hysteresis loss in conveyor belts or as an active filler in colored rubber particles or in products with good contact.

- According to the United States Bureau of Economic Analysis, the value added by rubber products (plastic products included) in the country during 2022 was more than USD 382 billion, approximately 11% more than the value added during the previous year.

- Specialty Silica is mainly used in rubber for tire production due to its extremely high purity and low moisture absorption. It has superior electrical properties to rubber products.

- In North America, according to the Organisation Internationale des Constructeurs d'Automobiles (OICA), automotive production in 2022 accounted for 14.8 million units, an increase of 9.88% compared to the production in 2021, which was reported to be 13.4 million units.

- Further, OICA also stated that, in 2022, Germany produced 3.7 million vehicles which increased by 11% compared to 3.3 million vehicles in the same period in 2021, thereby indicating an increased demand for tires from the automotive industry.

- According to the Modern Tire Dealer, in 2022, overall shipments of United States tires amounted to around 335 million units. The majority of tire units shipped in 2022 were replacement passenger tires, with some 222 million units. The increasing tire industry would eventually enhance the demand from the rubber industry, thereby benefiting the specialty silica market.

- Therefore, all the aforementioned factors are expected to drive the global market during the forecast period.

Asia-Pacific to Dominate the Market

- The Asia-Pacific region is expected to dominate the market for specialty silica during the forecast period. In countries like China, India, and Japan, owing to the increasing demand from applications such as tire manufacturing, industrial rubber manufacturing, paints and coatings, and the personal care industry.

- In 2022, according to the World Paint & Coatings Industry Association, the Asia-Pacific paints and coatings industry was estimated to be worth USD 63 billion. China dominated the region's market, which is growing at a CAGR of 5.8%. In 2022, the Chinese market is expected to have grown by 5.7%. According to current trends, China's total sales of paints and coatings exceeded USD 45 billion in 2022. In East Asia, the country had the largest market share of 78%.

- India is the fourth-largest consumer of rubber in the world as of 2022. Rubber usage per capita in India is currently 1.2 kilograms, compared to 3.2 kilograms globally. The rubber industry in India generates revenue of approximately INR 12 thousand crores (~USD 1.4 billion). The tire sector consumes the majority of India's rubber production, accounting for over half of the country's total output.

- Owing to the growing rubber industry in the country, in 2023, Yokohama, the Indian arm of the Japanese Yokohama Rubber Company, announced that it would invest USD 82 million (~INR 679 crore) to expand its passenger car tire production capacity in India to meet the rising demands from the local market. The production facility at Visakhapatnam will be completed and start operations by the end of 2024.

- Moreover, China is the largest producer and consumer of automotive vehicles. The China Association of Automobile Manufacturers (CAAM) reported that, compared to the prior year, China's automobile production increased by about 3.4% in 2022. In comparison to the 26.08 million automobiles produced in the year 2021, around 27.02 million were produced in 2022. This increase would lead to growth in the demand for tires in the industry thereby impacting the specialty silica market.

- In India, about 12% of rubber is used to produce footwear. The Indian footwear industry is estimated to grow at 4.5% in the coming years. Under the sports footwear category, running shoes are the most consumed category, with a 1.5X spike compared to the previous year. Bata, one of the leading footwear brands in the country, has set out a plan to open 500 new franchise stores by the end of the year 2023.

- According to the Malaysian Rubber Board, Malaysia's exports have room for growth in terms of tire products as they registered a 6% increase from MYR 832.8 million (~USD 188.9 million) to MYR 883.2 million (~USD 200.39 million) during the first half of 2022. The council is trying to focus more on new investments, technological advances, and greener products to boost the country's exports.

- Hence, all such market trends are expected to drive the demand for the specialty silica market in the region during the forecast period.

Specialty Silica Industry Overview

The specialty silica market is fragmented in nature. In terms of market share, few of the major players currently dominate the market. Some of the key players in the specialty silica market include W. R. Grace & Co., Cabot Corporation, Imerys, Evonik Industries AG, and Nouryon, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Demand from the Rubber Industry

- 4.1.2 Increasing Utilization of Specialty Silica in Personal Care Products

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Expensive Nature of Specialized Silica

- 4.2.2 Availability of Substitute Products in the Market

- 4.3 Industry Value-Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Type

- 5.1.1 Precipitated Silica

- 5.1.2 Silica Gel

- 5.1.3 Fumed Silica

- 5.1.4 Colloidal Silica

- 5.1.5 Fused Silica

- 5.2 Application

- 5.2.1 Rubber

- 5.2.2 Personal Care

- 5.2.3 Food and Feed

- 5.2.4 Chemicals

- 5.2.5 Plastics

- 5.2.6 Paints, Coatings and Inks

- 5.2.7 Metal and Refractories

- 5.2.8 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers & Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M (Ceradyne Inc.)

- 6.4.2 Cabot Corporation

- 6.4.3 Clariant

- 6.4.4 Denka Company Limited

- 6.4.5 Evonik Industries AG

- 6.4.6 Fuji Silysia Chemical

- 6.4.7 Fuso Chemical Co. Ltd

- 6.4.8 Glassven C.A.

- 6.4.9 Imerys

- 6.4.10 Merck KGaA

- 6.4.11 Nouryon

- 6.4.12 Orisil

- 6.4.13 Tata Chemicals

- 6.4.14 W. R. Grace & Co.

- 6.4.15 Wacker Chemie AG

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Emergence of Green Tires

- 7.2 Other Opportunities