|

市場調査レポート

商品コード

1404503

海軍船舶用プロペラ:市場シェア分析、産業動向・統計、成長予測、2024~2029年Naval Ship Propeller - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 海軍船舶用プロペラ:市場シェア分析、産業動向・統計、成長予測、2024~2029年 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

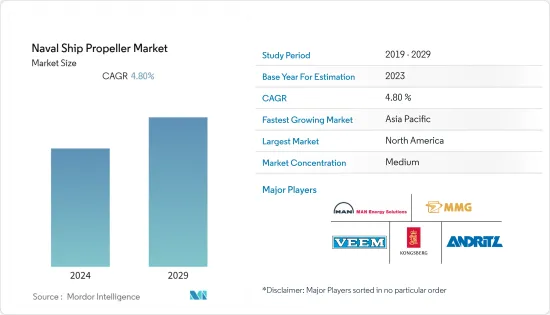

海軍船舶用プロペラ市場は、2024年に48億9,000万米ドルと推定・予測され、2029年には61億8,000万米ドルに達し、予測期間(2024-2029年)のCAGRは4.8%を記録すると予測されています。

造船業界における電気推進技術に対する需要の増加が、海軍船舶用プロペラ市場を牽引すると予想されます。この電気推進技術方式による推進では、クラッチや歯車装置が不要になります。この技術は、従来のシステムに比べていくつかの利点があります。機械部品が柔軟に配置されるため、高い冗長性、強化された機動性、積載量の増加、さらに少ない排出量と燃料消費を実現します。

軍が直面しているさまざまな海洋問題のために、海軍船舶の調達は年々増加しています。これが今後数年間、海軍船舶用プロペラ市場を牽引する可能性があります。海上貿易と安全保障への関心の高まりも市場を強化します。さらに、世界の海軍近代化計画の高まりは、プロペラメーカーにチャンスをもたらします。

しかし、市場は、生産コストに影響を与える原材料価格の変動などの課題に直面しています。市場は防衛予算と地政学的緊張に大きく左右されます。

海軍船舶用プロペラの市場動向

固定ピッチプロペラセグメントが市場で上位を占める

固定ピッチプロペラセグメントが市場で最も高いシェアを占めています。固定ピッチプロペラは、制御ピッチプロペラのような機械・油圧サブシステムが組み込まれていないため、堅牢で信頼性が高いです。さらに、製造、設置、運用コストが他のタイプのプロペラよりも低いです。そのため、現在では海軍船舶に広く使用されています。固定ピッチプロペラは、小型船や接近性が重要な用途に適しています。さらに、さまざまな環境条件や運用要件において安定した性能を発揮することから、市場での地位はさらに強固なものとなっています。

アジア太平洋地域は予測期間中に目覚ましい成長を示す見込み

アジア太平洋地域は、予測期間中に最も高いCAGRで推移すると予想されます。同地域における海軍船舶の調達は、インドや中国といったアジア太平洋地域の新興経済国による高い軍事費によって推進されています。さらに、アラビア海、インド洋、南シナ海での紛争が、海軍の海上能力強化を後押ししています。

この地域の造船業の成長と地政学的緊張が艦艇の需要をさらに押し上げ、プロペラを含む先進推進システムの採用を促進する可能性があります。これらすべての要因が艦艇の調達を後押しし、海軍船舶用プロペラ市場の成長を支えています。例えば、2022年8月、BAEシステムズ・オーストラリアは、OEMのコングスベルグ・マリタイムの監督の下、オーストラリアのハンター級フリゲート艦用の2つのプロトタイププロペラブレードとプロペラハブを建設するために、VEEM社に176万米ドルの契約を付与しました。これは、VEEM社がハンターの厳格な基準に沿って製造する能力の最終テストです。これはVEEM社にとって、ハンタープログラム用の軍艦プロペラメーカーとして国防資格を得るための重要なマイルストーンとなります。

軍艦プロペラ業界の概要

海軍船舶用プロペラ市場は適度に統合されており、少数のプレーヤーが市場で大きなシェアを占めています。地元企業やサプライチェーン企業の買収は、同市場での存在感をさらに高めるのに役立っています。獲得する契約は海軍艦船であるため、多くの規範や規制要件を満たす必要があります。さらに、新規参入企業にとっては、海軍船舶用プロペラのサイズと複雑さが小型ボート用プロペラに比べてはるかに高いため、投資コストが高くなることが予想されます。材料や設計の面での研究開発への投資は、今後数年間、プレーヤーを助けるかもしれないです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手/消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- プロペラの種類

- 固定ピッチプロペラ

- 可変ピッチプロペラ

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- ロシア

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他アジア太平洋地域

- ラテンアメリカ

- メキシコ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- トルコ

- エジプト

- 南アフリカ

- その他中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Kongsberg Gruppen ASA

- MAN Energy Solutions SE

- VEEM Ltd

- ANDRITZ AG

- Mecklenburger Metallguss GmbH

- Bruntons Propellers Ltd

- SCHOTTEL GmbH

- Michigan Wheel

- AB Volvo

- Caterpillar Inc.

- Wartsila Corporation

- HD Hyundai Heavy Industries Co., Ltd.

- ABB Ltd

- Kawasaki Heavy Industries, Ltd.

第7章 市場機会と今後の動向

The naval ship propeller market is estimated at USD 4.89 billion in 2024 and is expected to reach USD 6.18 billion by 2029, registering a CAGR of 4.8% during the forecast period (2024-2029).

An increasing demand for electric propulsion technology in the shipbuilding industry is anticipated to drive the naval ship propeller market. This propulsion in electric propulsion technology method eliminates the need for clutches and gearing devices. This technology provides several advantages over the traditional system. Because of the flexible arrangement of mechanical components, it provides high redundancy, enhanced mobility, and increased payload, as well as fewer emissions and fuel consumption.

Procurements of naval ships are increasing every year due to various maritime issues that the military is facing. It may drive the market for naval ship propellers in the years to come. Growing maritime trade and security concerns also bolster the market. Additionally, rising naval modernization programs worldwide create opportunities for propeller manufacturers.

However, the market faces challenges such as fluctuating raw material prices, which impact production costs. The market is majorly dependent on defense budgets and geopolitical tensions.

Naval Ship Propeller Market Trends

The Fixed Pitch Propellers Segment Holds Highest Shares in the Market

The fixed-pitch propellers segment holds the highest market share in the market. Fixed pitch propellers are robust and reliable, as the system does not incorporate any mechanical and hydraulic subsystems as in the controlled pitch propellers. Moreover, the manufacturing, installation, and operational costs are lower than the other types of propellers. Thus, they are now widely used in naval ships. The fixed-pitch propellers are well suited for smaller vessels and applications where accessibility is crucial. Furthermore, their consistent performance in various environmental conditions and operational requirements further strengthens their position in the market. For instance, in April 2021, Rolls-Royce reached an agreement with Fincantieri Marinette Marine to design and manufacture up to 40 fixed-pitch propellers for the US Navy's Constellation-class (FFG-62) guided missile frigate program.

Asia-Pacific Region Will Showcase Remarkable Growth During the Forecast Period

Asia-Pacific is expected to register the highest CAGR during the forecast period. Procurements of naval ships in the region are driven by the high military expenditure by the emerging economies in the Asia-Pacific region, such as India and China. Additionally, the disputes in the Arabian Sea, Indian Ocean, and the South China Sea are propelling the navies to further strengthen their sea-based capabilities.

The region's growing shipbuilding industry and geopolitical tensions may further boost the demand for naval vessels, driving the adoption of advanced propulsion systems, including propellers. All these factors are helping the procurement of naval ships, thereby supporting the growth of the naval ship propeller market. For instance, in August 2022, BAE Systems Australia granted a USD 1.76 million contract to VEEM Ltd to construct two prototype propeller blades and a propeller hub for Australia's Hunter class frigates under the supervision of OEM Kongsberg Maritime. It is the final test of VEEM's capacity to manufacture to the Hunter's strict criteria. It represents a critical milestone for VEEM Ltd as it strives to become a defence-qualified warship propeller maker for the Hunter program.

Naval Ship Propeller Industry Overview

The naval ship propeller market is moderately consolidated in nature, with a presence of few players holding significant shares in the market. Kongsberg Gruppen AS, VEEM Ltd, MAN Energy Solutions SE, Mecklenburger Metallguss GmbH, and ANDRITZ AG are some of the prominent players in the market. Acquisitions of local players and companies in the supply chain help the players further strengthen their presence in the market. As the contracts to be gained are for naval ships, many norms and regulatory requirements should be met. Moreover, for new players, the investment costs are expected to be high, as the size and complexity of the propellers for naval ships are far higher compared to those for smaller boats. Investments in R&D, in terms of materials and designs, may help the players in the years to come.

For instance, in March 2023, Kongsberg Maritime and Hyundai Heavy Industries partnered to supply controllable pitch propellers for the Philippine Navy's future offshore patrol vessels. Under the terms of the agreement, Kongsberg will supply a propellor set for each of Hyundai's six new vessels. Each propellor set comes with two Kamewa 86 A/5 D-B waterjet propulsions, as well as operational panels, shat lines, hydraulic power units, and other accessories. Similarly, in January 2021, Naval Group, a defense contractor, created a fully 3D-printed propeller for a French Navy ship. The propeller, which contains a 2.5 m span and five individual 200 kg blades, is reputedly the largest of its kind to be 3D printed and the first to be created using Naval Group's method.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Propeller Type

- 5.1.1 Fixed-Pitch Propeller

- 5.1.2 Controllable-Pitch Propeller

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 Germany

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Russia

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 South Korea

- 5.2.3.5 Australia

- 5.2.3.6 Rest of Asia-Pacific

- 5.2.4 Latin America

- 5.2.4.1 Mexico

- 5.2.4.2 Brazil

- 5.2.4.3 Rest of Latin America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 United Arab Emirates

- 5.2.5.2 Saudi Arabia

- 5.2.5.3 Turkey

- 5.2.5.4 Egypt

- 5.2.5.5 South Africa

- 5.2.5.6 Rest of Middle-East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Kongsberg Gruppen ASA

- 6.2.2 MAN Energy Solutions SE

- 6.2.3 VEEM Ltd

- 6.2.4 ANDRITZ AG

- 6.2.5 Mecklenburger Metallguss GmbH

- 6.2.6 Bruntons Propellers Ltd

- 6.2.7 SCHOTTEL GmbH

- 6.2.8 Michigan Wheel

- 6.2.9 AB Volvo

- 6.2.10 Caterpillar Inc.

- 6.2.11 Wartsila Corporation

- 6.2.12 HD Hyundai Heavy Industries Co., Ltd.

- 6.2.13 ABB Ltd

- 6.2.14 Kawasaki Heavy Industries, Ltd.