|

市場調査レポート

商品コード

1687816

航空機シートアクチュエーションシステム:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Aircraft Seat Actuation Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空機シートアクチュエーションシステム:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

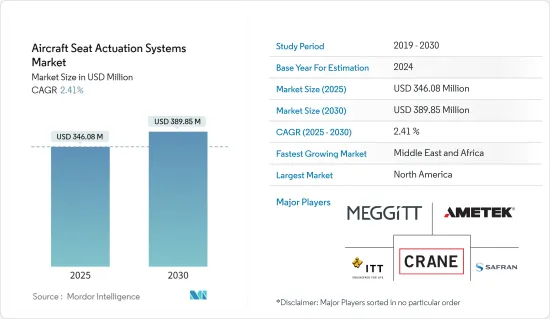

航空機シートアクチュエーションシステム市場規模は、2025年に3億4,608万米ドルと推定され、予測期間(2025-2030年)のCAGRは2.41%で、2030年には3億8,985万米ドルに達すると予測されます。

2020年のCOVID-19パンデミックの発生は、航空業界全体に深刻な影響を与えました。その結果、いくつかの航空機運航会社が破産を申請し、短期的には航空機の需要や航空機の座席作動システムに影響を与えました。しかし、2021年には、前年に比べ航空機納入が増加したため、市場は徐々に回復しました。同様の動向は、軍用機や一般航空分野にも反映されています。

各国でのワクチン接種の増加に伴い、航空旅客に対する規制が緩和され、航空旅客数は徐々に増加しています。このような旅客輸送量の緩やかな回復は、航空会社や航空機運航会社が機体の近代化や目的地拡大のために新しい航空機の調達に投資することを後押ししています。これが予測期間中の市場成長を大きく後押ししています。

航空機内での乗客体験を向上させるための航空会社や航空機運航会社による客室近代化のための投資の増加や、より高いレベルの乗客の快適性を提供するためのシートメーカーによるシート設計の革新は、今後数年間の航空機シート作動システム市場の需要を促進すると予想されます。

薄型ダウンパネルやその他のシートコンポーネントを製造するための積層造形などの技術への投資により、コンポーネントの全体的な重量と製造コストが削減され、軽量シートアクチュエータとモーターの開発が促進されると予想されます。

航空機シートアクチュエーションシステム市場動向

固定翼機セグメントが2021年の主要収益シェアを占める

現在、固定翼機セグメントが市場を独占しています。回転翼機よりも納入数が多く、シート要件も高いことから、今後も市場の優位性が続くと予測されます。2021年の新規航空機納入数は、旅客輸送量と航空事業が徐々に増加したため、2020年に比べて改善しました。2021年には、エアバスが611機の民間航空機を納入(2020年は566機)、ボーイングが340機の民間航空機を納入(2020年は157機)、ATRが31機を納入(2020年は10機)しました。民間航空やビジネス・プライベート航空に対する需要が徐々に回復していることが、新型機の調達をさらに後押ししています。

同様に、サプライチェーンの問題が沈静化するにつれて、軍事部門における固定翼航空機の納入が伸びています。例えば、ロッキード・マーチンは142機のF-35戦闘機を納入し(2020年の納入数は123機)、ダッソー・アビエーションは25機のラファール戦闘機を輸出した(2020年の納入数は13機)。航空機納入数の増加は、予測期間中の市場の成長を促進すると予想されます。また、航空機運航会社と協力して、航空機シートメーカーは新たな顧客を獲得するためにデザインの強化に取り組んでいます。このような客室内装や座席モジュールの革新は、今後数年間、このセグメントの成長を促進すると予想されます。

中東・アフリカ地域が予測期間中に最も高い成長を遂げる見込み

航空機シートアクチュエーションシステム市場の需要は、大手航空会社によるワイドボディ航空機の需要や、非公開会社やチャーター会社による大型航空機の需要により、中東・アフリカ地域で最も高くなると予想されます。例えば、エティハド航空とエミレーツ航空は、ボーイング777X、エアバスA350ファミリー、A380、ボーイング787ファミリーを含む270機以上の航空機を受注している(2022年1月現在)。同様に、中東地域における航空需要の増加に伴い、中東地域の航空会社や航空機運航会社は、同地域に新たな航空機路線を導入するため、航空機保有数の拡大に投資しています。

同様に、この地域におけるテロの増加により、これらの国々は軍用機の調達に多額の支出を行っています。カタール首長国空軍(QEAF)は2021年8月、湾岸諸国と提携して米国とボーイングが製造した新世代のF-15戦闘機の最初のバッチを受領しました。この航空機は、2017年に同国がF-15QA戦闘機36機を調達するために締結した発注に基づいて納入されたもので、36機の追加オプションがあります。エジプト、ヨルダン、モロッコ、アルジェリア、イスラエルの空軍からの同様の航空機発注は、予測期間中にシートアクチュエーションシステム市場の成長を加速すると予想されます。

航空機シートアクチュエーションシステム産業概要

航空機シートアクチュエーションシステム市場は、多くのコンポーネントプロバイダーが市場に存在しているにもかかわらず、非常に少数のプレーヤーが市場の大半のシェアを占めており、高度に統合された市場です。航空機シートアクチュエーションシステム市場の著名なプレーヤーとしては、Safran SA、Meggit PLC、Crane Co.、AMETEK Inc.、ITT Inc.などが挙げられます。需要は堅調に推移し、軍事用途の景気低迷やCOVID-19パンデミックによる市場の変動はないと予想されます。したがって、メーカーは収益源を安定させ確保するために、このセグメントに焦点を当てるべきです。アジア太平洋地域と中東・アフリカ地域は、現在、航空産業で需要が発生しているが、現在、迅速な供給を行うための十分なインフラと製品の在庫が不足しています。そのため、先発者としての優位性が得られ、また、契約義務の一部として世界的に多くの政府が定めているオフセット条項の恩恵も受けられることから、各社は現地の未開発地域におけるプレゼンスを拡大しようとしています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

- 米ドルの通貨換算レート

第2章 調査手法

第3章 エグゼクティブサマリー

- 市場規模および予測、世界、2018年~2027年

- メカニズム別市場シェア:2021年

- 航空機タイプ別市場シェア:2021年

- 地域別市場シェア、2021年

- 市場構造と主要参入企業

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- メカニズム

- リニア

- ロータリー

- 航空機タイプ

- 固定翼機

- ヘリコプター

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- エジプト

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Lee Air Inc.

- Safran SA

- Astronics Corporation

- Crane Co.

- ITT Inc.

- CEF Industries LLC

- ElectroCraft Inc.

- NOOK Industries Inc.

- Rollon SpA

- Buhler Motor GmbH

- AMETEK Inc.

- Kyntronics

- Meggitt PLC

- OTM Servo Mechanisms Limited

第7章 市場機会と今後の動向

The Aircraft Seat Actuation Systems Market size is estimated at USD 346.08 million in 2025, and is expected to reach USD 389.85 million by 2030, at a CAGR of 2.41% during the forecast period (2025-2030).

The outbreak of the COVID-19 pandemic in 2020 severely impacted the entire aviation industry. It has resulted in several aircraft operators filing for bankruptcy, which affected the demand for aircraft in the short term and aircraft seat actuation systems. However, the market gradually recovered in 2021 due to the increasing aircraft deliveries compared to the previous year. A similar trend has been reflected in the military and general aviation sectors.

With the increasing vaccination in various countries, the air passenger traffic is gradually increasing as the regulations for air travel are alleviating. This gradual recovery in passenger traffic supports the airlines and aircraft operators to invest in the procurement of new aircraft for fleet modernization and destination expansion. This is majorly driving the growth of the market during the forecast period.

Growing investment for cabin modernization by airlines and aircraft operators to enhance passenger experience onboard aircraft and innovation in seat designs by the seat manufacturers for offering a higher level of passenger comfort is anticipated to propel the demand for the aircraft seat actuation systems market in the coming years.

The investments into technologies like additive manufacturing for manufacturing thin down panels and other seat components to reduce the overall weight and cost of manufacturing components are anticipated to promote the development of lightweight seat actuators and motors.

Aircraft Seat Actuation Systems Market Trends

The Fixed-wing Aircraft Segment Accounted for Major Revenue Share in 2021

The fixed-wing aircraft segment currently dominates the market. It is anticipated to continue its dominance over the market due to its higher deliveries and seat requirements than the rotary-wing aircraft. New aircraft deliveries improved in 2021 compared to 2020 due to gradual growth in passenger traffic and airline operations. In 2021, Airbus delivered 611 commercial aircraft (566 deliveries in 2020), Boeing delivered 340 commercial aircraft (157 deliveries in 2020), and ATR delivered 31 aircraft (10 deliveries in 2020). The gradual recovery in demand for commercial aviation and business and private aviation is further propelling the procurement of new aircraft.

Similarly, as the supply chain issues subsided, the fixed-wing aircraft deliveries in the military sector have witnessed growth. For instance, Lockheed Martin delivered 142 F-35 fighter aircraft (compared to 123 deliveries in 2020), and Dassault Aviation exported 25 Rafale fighter jets (compared to 13 deliveries in 2020). The growth in aircraft deliveries is anticipated to propel the market's growth during the forecast period. Also, in collaboration with aircraft operators, the aircraft seat manufacturers are working on enhancing their designs to attract new customers. Such innovation in cabin interiors and seating modules is expected to propel the segment's growth in the coming years.

The Middle-East and Africa Region Expected to Witness Highest Growth During the Forecast Period

The demand for the aircraft seat actuation systems market is anticipated to be highest in the Middle-East and African region due to demand for wide-body aircraft from major airlines and large-size aircraft demand from private and charter companies. For instance, Etihad and Emirates had an order book of more than 270 aircraft (as of January 2022), including Boeing 777X, Airbus A350 family, A380, and Boeing 787 family of aircraft. Similarly, with the growing demand for air travel in the Middle-East region, the airlines and aircraft operators in the region are investing in expanding their aircraft fleet to introduce new aircraft routes in the region.

Similarly, the growth in terrorism in this region has resulted in these countries spending a significant amount on military aircraft procurement. The Qatar Emiri Air Force (QEAF) received its first batch of the new generation F-15 combat aircraft in August 2021, produced by the United States and Boeing, in partnership with the Gulf state. The aircraft was delivered under an order signed by the country in 2017 to procure 36 F-15QA fighter aircraft with an option for an additional 36 aircraft. Similar aircraft orders from Air Forces of Egypt, Jordan, Morocco, Algeria, and Israel are anticipated to accelerate the growth of the seat actuation systems market during the forecast period.

Aircraft Seat Actuation Systems Industry Overview

The market of aircraft seat actuation systems is a highly consolidated market with very few players accounting for the majority share in the market despite the presence of the many component providers in the market. Some prominent players in the aircraft seat actuation systems market are Safran SA, Meggit PLC, Crane Co., AMETEK Inc., and ITT Inc. The demand is expected to remain robust and free from market fluctuations due to the economic downturn and COVID-19 pandemic from the military applications side. Thus manufacturers should focus on this segment to stabilize and secure their revenue sources. The Asia-Pacific and the Middle-East and Africa regions, which are currently experiencing demand in the aviation industry, presently lack adequate infrastructure and inventory of products to supply quickly. Therefore, the companies are expanding their presence in underdeveloped regions locally, as it would provide them the first-mover advantage and will also benefit from offset clauses that are being set forth by many governments globally as part of contract obligations.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of Study

- 1.3 Currency Conversion Rates for USD

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

- 3.1 Market Size and Forecast, Global, 2018 - 2027

- 3.2 Market Share by Mechanism, 2021

- 3.3 Market Share by Aircraft Type, 2021

- 3.4 Market Share by Geography, 2021

- 3.5 Structure of the Market and Key Participants

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size and Forecast by Value - USD million, 2018 - 2027)

- 5.1 Mechanism

- 5.1.1 Linear

- 5.1.2 Rotary

- 5.2 Aircraft Type

- 5.2.1 Fixed-wing Aircraft

- 5.2.2 Helicopters

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Germany

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Egypt

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Lee Air Inc.

- 6.2.2 Safran SA

- 6.2.3 Astronics Corporation

- 6.2.4 Crane Co.

- 6.2.5 ITT Inc.

- 6.2.6 CEF Industries LLC

- 6.2.7 ElectroCraft Inc.

- 6.2.8 NOOK Industries Inc.

- 6.2.9 Rollon SpA

- 6.2.10 Buhler Motor GmbH

- 6.2.11 AMETEK Inc.

- 6.2.12 Kyntronics

- 6.2.13 Meggitt PLC

- 6.2.14 OTM Servo Mechanisms Limited