|

市場調査レポート

商品コード

1687785

急性虚血性脳卒中診断:市場シェア分析、産業動向、成長予測(2025年~2030年)Acute Ischemic Stroke Diagnosis - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 急性虚血性脳卒中診断:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 137 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

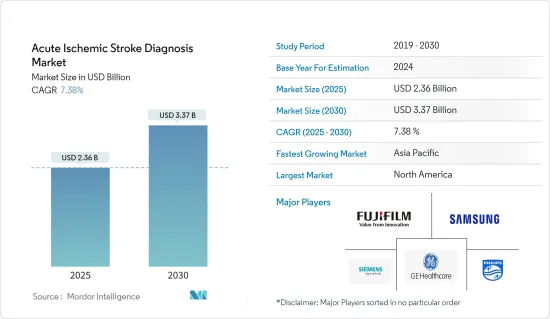

急性虚血性脳卒中診断の市場規模は、2025年に23億6,000万米ドルと推定され、予測期間中(2025年~2030年)のCAGRは7.38%で、2030年には33億7,000万米ドルに達すると予測されます。

急性虚血性脳卒中診断市場は、SARS-CoV-2ウイルス感染の拡大を抑制するために医療処置のほとんどが延期されたため、COVID-19パンデミックの発生によって大きな影響を受けたと予想されます。Julie Sandersが2021年3月にJournal of Cardiothoracic Surgery誌に発表した調査論文によると、パンデミックの間、心臓外科手術は50~75%減少し、英国では心臓外科専用の部屋とICUのベッドが50%減少しました。さらに、2021年7月にAnnals of Thoracic Surgery誌に発表された研究結果「The Effect of COVID-19 on Adult Cardiac Surgery in the United States in 717,103 Patients」によると、2020年の米国では2019年と比較して心臓手術総件数の推定53%の減少が観察され、これは主にCOVID-19パンデミックの影響によるものでした。

急性虚血性脳卒中の有病率の上昇は、急性脳卒中治療における診断と外科手術の両方に対する世界の需要を促進し、脳卒中市場と虚血性脳卒中市場の成長に寄与しています。2021年6月の世界保健機関(WHO)の統計によると、心血管疾患(CVD)は世界の死因のトップです。また、2019年には推定1,790万人が心血管疾患で死亡し、全世界の死亡者数の32%を占めるとしています。これらの死因の85%は心臓発作または脳卒中です。同出典によると、非伝染性疾患は2019年に1,700万人の早死(70歳未満)の原因となっており、心血管疾患はその38%を占めています。

外科手術の技術的進歩、高齢化人口の増加、低侵襲手術の需要増、医療費の伸びなどが、世界の脳卒中診断薬・治療薬市場の成長を促進するその他の主な要因です。米国心臓病学会が報告したデータによると、2020年11月、米国では1年間に約120万件の血管形成術が実施されました。さらに、専門クリニックと比較して、病院の高いアクセス性と手頃な価格は、多くの患者を引き付けると予想されます。

虚血性脳卒中治療のための過剰な薬物使用と外科的処置の高コストが、虚血性脳卒中治療市場の成長を妨げています。しかし、厳しい規制政策が市場の成長を制限すると予想されます。

急性虚血性脳卒中診断市場の動向

予測期間中、コンピュータ断層撮影(CT)セグメントが世界市場を牽引

脳卒中診断では、脳損傷の程度を評価し、虚血性欠損の原因となる血管病変を特定するために、急性脳卒中患者の出血を検出する画像検査が行われます。

CTやMRIの先端技術の中には、脳梗塞の診断に貢献する不可逆的梗塞と、救命可能な脳組織を区別できるものもあり、それによって治療効果が期待できる患者をより適切に選択することができます。

コンピュータ断層撮影は脳卒中画像診断の主要な診断分野です。CT技術が大きなシェアを占めているのは、アクセスが広く、撮影速度が速いためです。超急性期には通常、出血の除外または確認のために非造影CT(NCCT)検査が行われます。

さらに、新製品の発売と承認が急性虚血性脳卒中診断市場を新たな高みへと押し上げると思われます。例えば、2021年5月、フィリップスヘルスケアは米国食品医薬品局(USFDA)からコンピュータ断層撮影装置「Spectral CT 7500」の承認を取得しました。この装置は、インテリジェントなソフトウェアを使用し、特別なプロトコルを必要とせず、すべてのスキャンで100%高品質のスペクトル画像を提供します。

このように、技術的進歩や製品の発売といった前述の要因は、予測期間中に脳卒中診断市場セグメントを押し上げると予想されます。

予測期間中、北米が大きな市場シェアを占める

北米は急性虚血性脳卒中診断機器市場を独占しており、政府の積極的な取り組み、技術革新、虚血性脳卒中製品の需要増加により、急性虚血性脳卒中診断機器市場における牙城を守り続けると予測されます。さらに、同市場で事業を展開する主要企業は、世界の急性虚血性脳卒中AIS市場における製品ポートフォリオとプレゼンスを拡大するため、買収や契約などの無機的成長戦略の採用に注力しています。例えば、2020年11月、世界のサイエンス主導のバイオ医薬品企業であるアストラゼネカは、急性虚血性脳卒中または高リスクの一過性脳虚血発作(TIA)患者において、障害および死亡の世界の主要原因である脳卒中のリスクを低減するために使用される製品Brilinta(経口可逆的直接作用型P2Y12受容体拮抗薬)の発売を発表し、一過性脳虚血発作治療市場の成長に貢献しています。

さらに、北米全域で脳卒中の有病率が増加していることも、市場成長の原動力となっています。米国心臓協会2022によると、米国では2019年、心血管疾患(CVD)が死亡の根本的な原因として認識され、874,613人の死亡者を占めました。さらに、Dawn O. Kleindorferが2021年5月に米国心臓協会誌に発表した論文によると、米国では毎年795,000人が脳卒中を発症しており、その87%(690,000人)が虚血性で、185,000人が再発性です。また、毎年24万人以上が一過性脳虚血発作(TIA)に苦しんでいます。このように、国内における心血管疾患と脳卒中の有病率の増加は、脳卒中市場と一過性脳虚血発作市場を押し上げると予想されます。

このように、前述の要因は北米における予測期間中の急性虚血性脳卒中診断市場を押し上げると予想されます。

急性虚血性脳卒中診断産業の概要

急性虚血性脳卒中診断製品の主要ベンダーは、アジア諸国(インド、中国、日本、韓国)での事業拡大を図っています。世界の急性虚血性脳卒中診断市場に参入している主な企業には、富士フイルムホールディングス、サムスン電子、GEヘルスケア、日本光電工業、キヤノンメディカルシステムズ、Koninklijke Philips NVなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 急性脳卒中患者の増加

- 診断機器および手術機器における技術革新

- 市場抑制要因

- 代替治療と高コスト

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 診断タイプ

- コンピュータ断層撮影

- 磁気共鳴画像法

- 頸動脈超音波

- 脳血管撮影

- 心電図検査

- 心エコー検査

- その他の診断

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Fujifilm Holdings Corporation

- Samsung Electronics Co. Ltd

- GE Healthcare

- Nihon Kohden Corporation

- Canon Medical Systems Corporation

- Koninklijke Philips NV

- Siemens Healthineers AG

- Mindray Medical International Limited

- Nanavati Super Speciality Hospital

- F. Hoffmann-La Roche AG

- Boehringer Ingelheim

- Global Diagnostics(Integral Diagnostics Group)

- Memorial Health System(Memorial Medical Center)

第7章 市場機会と今後の動向

The Acute Ischemic Stroke Diagnosis Market size is estimated at USD 2.36 billion in 2025, and is expected to reach USD 3.37 billion by 2030, at a CAGR of 7.38% during the forecast period (2025-2030).

The Acute Ischemic Stroke Diagnostics Market is anticipated to have been significantly impacted by the outbreak of the COVID-19 pandemic, as most of the medical procedures were deferred to contain the spread of SARS-CoV-2 viral transmission. According to the research article published in the Journal of Cardiothoracic Surgery in March 2021 by Julie Sanders, cardiac surgery reduced by 50-75% during the pandemic, with a 50% reduction in dedicated cardiac theater rooms and ICU beds in the United Kingdom. Additionally, as per the study results published in the Journal of Annals of Thoracic Surgery, in July 2021, "The Effect of COVID-19 on Adult Cardiac Surgery in the United States in 717,103 Patients," an estimated 53% decrease in the total cardiac surgery volume was observed in the United States in 2020 as compared to 2019, which was majorly attributed to the impact of COVID-19 pandemic.

The rising prevalence of Acute Ischemic Stroke cases is driving the global demand for both diagnostic and surgical procedures in acute stroke treatment, contributing to the growth of the Stroke Market and the Ischemic Stroke Market. Cardiovascular Diseases (CVDs) are the leading cause of death worldwide, according to World Health Organization (WHO) statistics for June 2021. It also states that an estimated 17.9 million people died from cardiovascular diseases in 2019, accounting for 32% of all global deaths. 85% of these deaths were caused by a heart attack or a stroke. According to the same source, non-communicable diseases are responsible for 17 million premature deaths (under the age of 70) in 2019, with cardiovascular diseases accounting for 38% of these deaths.

Technological advancements in surgical procedures, a rising aging population, increased demand for minimally invasive procedures, and growth in health care spending are the other major factors driving the growth of the global Stroke Diagnostics and Therapeutics Market. As per the data reported by the American College of Cardiology, in November 2020, approximately 1.2 million angioplasties were performed in a year in the United States. Moreover, the high accessibility and affordability of hospitals, as compared to the specialty clinics, are expected to attract a large patient population.

Excessive usage of medication for the treatment of Ischemic Stroke and the high cost of surgical procedures are hindering the growth of the Ischemic Stroke Treatment Market. However, stringent regulatory policies are expected to restrict the market growth.

Acute Ischemic Stroke Diagnosis Market Trends

The Computed Tomography (CT) Segment Led the Global Market Over the Forecast Period

Imaging studies are used in Stroke Diagnosis for the detection of hemorrhage in acute stroke patients in order to assess the degree of brain injury and to identify the vascular lesion responsible for the Ischemic deficit.

Some advanced CT and MRI technologies are able to distinguish between brain tissue that is irreversibly infarcted, contributing to Cerebral Infarction Diagnosis, and that which is potentially salvageable, thereby allowing a better selection of patients likely to benefit from therapy.

Computed Tomography is the leading diagnostics segment in Stroke Diagnostic Imaging. The significant share of CT techniques is attributable to widespread access and speed of acquisition. In the hyperacute phase, a non-contrast CT (NCCT) scan is usually ordered to exclude or confirm hemorrhage; it is highly sensitive for this indication.

Additionally, new product launches and approval will push the Acute Ischemic Stroke Diagnosis Market to grow to new heights. For instance, in May 2021, Philips Healthcare received approval from the United States Food and Drug Administration (USFDA) for the computed tomography system, the Spectral CT 7500, which uses intelligent software to deliver high-quality spectral images on every scan 100% of the time without the need for special protocols.

Thus, the aforementioned factors such as technological advancement and product launches are expected to boost the Stroke Diagnostics Market segment over the forecast period.

North America Holds the Large Market Share in the Market Over the Forecast Period

North America dominates the market for Acute Ischemic Stroke Diagnosis devices, and it is estimated to continue its stronghold in the Acute Ischemic Stroke Diagnosis Market, owing to favorable government initiatives, technological innovations, and increasing demand for Ischemic Stroke products. Furthermore, key players operating in the market are focusing on the adoption of inorganic growth strategies such as acquisition and agreements in order to expand their product portfolio and presence in the global Acute Ischemic Stroke AIS Market. For instance, in November 2020, AstraZeneca, a global, science-led biopharmaceutical company, announced the launch of the product Brilinta (an oral, reversible, direct-acting P2Y12 receptor antagonist), which is used to reduce the risk of stroke, a leading global cause of disability and death, in patients with Acute Ischemic Stroke or high-risk Transient Ischemic Attack (TIA), contributing to the growth of the Transient Ischemic Attack Treatment Market.

Additionally, the increasing prevalence of stroke across North America drives market growth. According to the American Heart Association 2022, in the United States in 2019, Cardiovascular Disease (CVD) was recognized as the underlying cause of mortality, accounting for 874,613 fatalities. Additionally, according to the article published in the American Heart Association Journal in May 2021 by Dawn O. Kleindorfer, in the United States, 795,000 people have a stroke each year, with 87% (690,000) being Ischemic and 185,000 being recurrent. Each year, over 240,000 people suffer from a Transient Ischemic Attack (TIA). Thus, the increasing prevalence of Cardiovascular Diseases and stroke in the country is expected to boost the Stroke Market and the Transient Ischemic Attack Market.

Thus, the aforementioned factors are expected to boost the Acute Ischemic Stroke Diagnosis Market over the forecast period in North America.

Acute Ischemic Stroke Diagnosis Industry Overview

The leading vendors of Acute Ischemic Stroke Diagnosis products are expanding their operations in Asian countries (India, China, Japan, and South Korea), as these economies hold immense potential for Acute Ischemic Stroke Diagnosis. Major players operating in the global Acute Ischemic Stroke Diagnosis Market include Fujifilm Holdings Corporation, Samsung Electronics Co. Ltd, GE Healthcare, Nihon, Kohden Corporation, Canon Medical Systems Corporation, and Koninklijke Philips NV.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 The Rising Number of Acute Stroke Patients

- 4.2.2 Technological Innovations in Diagnostic and Surgical Devices

- 4.3 Market Restraints

- 4.3.1 Alternative Treatments and High Costs

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 Diagnostic Type

- 5.1.1 Computed Tomography

- 5.1.2 Magnetic Resonance Imaging

- 5.1.3 Carotid Ultrasound

- 5.1.4 Cerebral Angiography

- 5.1.5 Electrocardiography

- 5.1.6 Echocardiography

- 5.1.7 Other Diagnostic Types

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Australia

- 5.2.3.5 South Korea

- 5.2.3.6 Rest of Asia-Pacific

- 5.2.4 Middle-East and Africa

- 5.2.4.1 GCC

- 5.2.4.2 South Africa

- 5.2.4.3 Rest of Middle-East and Africa

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Argentina

- 5.2.5.3 Rest of South America

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Fujifilm Holdings Corporation

- 6.1.2 Samsung Electronics Co. Ltd

- 6.1.3 GE Healthcare

- 6.1.4 Nihon Kohden Corporation

- 6.1.5 Canon Medical Systems Corporation

- 6.1.6 Koninklijke Philips NV

- 6.1.7 Siemens Healthineers AG

- 6.1.8 Mindray Medical International Limited

- 6.1.9 Nanavati Super Speciality Hospital

- 6.1.10 F. Hoffmann-La Roche AG

- 6.1.11 Boehringer Ingelheim

- 6.1.12 Global Diagnostics (Integral Diagnostics Group)

- 6.1.13 Memorial Health System (Memorial Medical Center)