|

市場調査レポート

商品コード

1850164

創傷ケア管理機器:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Wound Care Management Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 創傷ケア管理機器:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月16日

発行: Mordor Intelligence

ページ情報: 英文 112 Pages

納期: 2~3営業日

|

概要

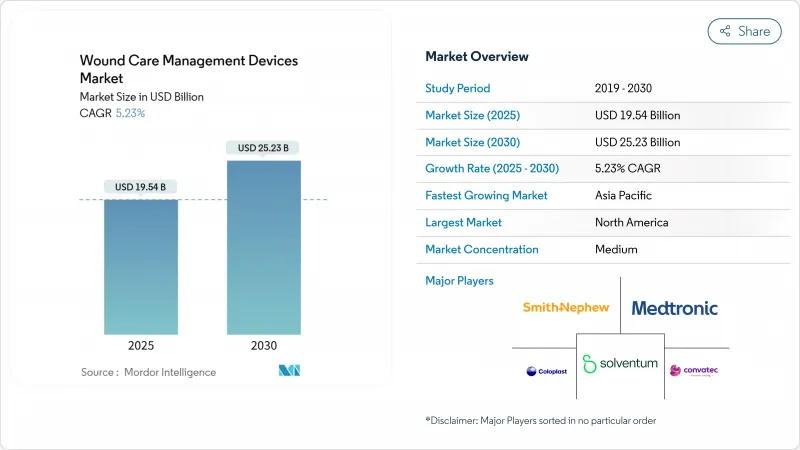

創傷ケア管理機器市場規模は2025年に195億4,000万米ドル、2030年には252億3,000万米ドルに達し、CAGR 5.23%で成長すると予測されています。

人口の高齢化、糖尿病の有病率の上昇、外科手術の着実な成長が、持続的な需要の追い風となっています。病院は再入院を抑制するために陰圧創傷治療(NPWT)やスマートドレッシングに投資しており、小売店は在宅治療を可能にする市販品を拡充しています。藻類由来の止血ゲルや生体工学的組織マトリックスなどの画期的な製品は、治癒期間を短縮し、長期的なコストを削減しています。米国と欧州連合(EU)では、クラスIの液体絆創膏やその他の低リスク器具の規制が迅速に行われるようになり、商品化が加速しています。市場の既存企業はAIの専門家と提携し、ドレッシング材やポンプにリアルタイムの画像処理と意思決定サポートを組み込むことで対応しています。

世界の創傷ケア管理機器市場の動向と洞察

慢性・糖尿病性創傷の増加

糖尿病性足潰瘍は現在、糖尿病患者の15%に影響を与えており、病院は高度なドレッシング材と継続的なグルコースモニタリングを組み合わせた集学的プログラムを採用する傾向にあります。時間ゲートの中赤外光音響センサーは、深部選択的なグルコース測定を可能にし、臨床医が合併症が起こる前に治療を調整することを可能にします。早期介入戦略は入院日数を短縮し、切断リスクを低下させています。支払者は、ドレッシング材、センサー、遠隔医療フォローアップをカバーする一括支払いで、こうした成果に報いています。そのためメーカー各社は、ドレッシング材に電子機器を組み込んで水分、pH、温度データを送信し、慢性期医療プロトコルに沿った機器設計を行うようになっています。

世界の手術件数の増加

2025年には世界的な待機手術と外傷手術が回復し、高度閉鎖ストリップ、組織シーラント、NPWTキャニスターの需要が増加しました。頭皮を対象としたモース顕微鏡手術の臨床試験で、ピンチグラフトはセカンド・インテンション・プロトコルと比較して治癒時間を短縮することが確認されました。外来手術センターは、処理能力を拡大するにつれて、即日退院モデルに適合するコンパクトなNPWTポンプを導入しています。超音波ガイド下デブリードマンは感染リスクを回避し、リアルタイムの画像診断は米国の大規模病院での再入院ペナルティを削減するのに役立ちました。これらの結果は、予算が逼迫しているにもかかわらず、調達チームが閉鎖ポートフォリオを一新することを後押ししています。

新興市場における限定的な償還

東南アジアやラテンアメリカでは、多くの公的保険会社がまだ基本的なガーゼしかカバーしていないため、NPWTや生体工学的皮膚代替物の導入が遅れています。地方の診療所ではサプライチェーンの格差に直面することが多く、アクセスがさらに制限されます。各国政府は、糖尿病性足潰瘍のための先進ドレッシング材を、一次的なドレッシング材が使用できない場合に償還する段階的な給付パッケージを試験的に導入しているが、予算の上限は依然として厳しいです。ポリウレタンフォームを国内で調達し、現場でキャニスターに充填する地元の組立業者が価格の障壁を下げているが、臨床医のトレーニングは遅れています。官民パートナーシップは、手頃な価格のギャップを埋めるために、成果ベースの資金調達とデバイスをバンドルし始めています。

セグメント分析

創傷ケア分野は2024年の売上高の62.43%を占めました。これは臨床医が複雑な症例に抗菌性フォーム、ハイドロファイバー、ポータブルNPWTシステムを好んで使用したためです。この優位性は、創傷ケア管理機器市場が感染リスクを低減し肉芽形成をサポートする製品に軸足を移し続けていることを裏付けています。創傷閉鎖用品(ステープル、接着剤、吸収性有刺縫合糸を含む)は、2030年までのCAGR見通しで5.87%を記録し、整形外科と心臓血管の数量増加に支えられました。伝統的なガーゼは、急性期が少ない環境では重要性を保っているが、術後の創傷には銀やPHMBを染み込ませたドレッシング材にシェアを譲る。

ドレッシング材にAIチップを組み込んだメーカーは、湿気の自動警告や抗菌剤の埋め込み投与を可能にし、褥瘡予防のための病院プロトコルに対応しています。一方、外用生物製剤は病院薬局から外来輸液センターへと移行し、使用範囲が拡大します。創傷ケア管理機器市場では、スマートセンサー層とハイドロゲル薬剤リザーバーを組み合わせたコンビネーション製品が見られ、新たに発行されたバンドルCPTコードによる償還をサポートしています。材料科学とデジタルモニタリングを連携させる供給企業の交渉力は、グループ購買組織による入札で優位に立ちます。

慢性創傷は2024年の売上高の58.34%を占め、糖尿病性足潰瘍、褥瘡、静脈性下腿潰瘍の資源強度を反映しています。これらの適応症では長期の治療が必要であり、再入院の減少が監査で確認されれば、支払者は高級ドレッシング材を承認します。外傷や術後の切開を含む急性創傷は、世界的な手術率の上昇によりCAGR 5.92%で拡大しています。熱傷センターでは、移植の必要性を減らすため、生合成皮膚代替物と組み合わせた酵素デブリーダが採用されています。

電子カルテに組み込まれた予測アルゴリズムが潰瘍リスクのある患者に警告を発し、オフローディングシューズや湿度管理フォームの早期適用を促します。褥瘡プロトコルは現在、マットレスのエアセルを調整して荷重を再分配する表面センサーを採用しています。糖尿病性潰瘍の管理には、灌流障害を検出するハンドヘルド画像分光計が有効であり、臨床医はケア経路の早い段階で血管介入を行うようになります。このようなワークフローの変化は、創傷ケア管理機器市場のプレミアム製品需要を強化します。

地域分析

北米が創傷ケア管理機器市場をリードし、2024年の市場売上高の40.12%を占める。洗練された保険モデルがハイエンドドレッシング、NPWT、バイオエンジニアリング組織に資金を提供しているためです。米国では、バリューベース契約による一括支払いが迅速な閉鎖と合併症の減少に報いるため、病院は次世代ハイドロゲルやセンサー付きフォームの試用を奨励しています。食品医薬品局は、リスクの低い液体包帯を510(k)クリアランスの対象から除外し、消費者向け製品の発売期間を短縮しています。カナダの単一支払い制度が在宅ケアNPWTパイロット事業に投資し、2025年までに外来診療の負担を18%削減。メキシコでは手術施設の整備が進み、中価格帯のクロージャーストリップとポリウレタンフィルムの入札が開始されます。

欧州は成熟しつつも技術革新の受け入れ態勢が整っています。各国の医療システムは、治癒サイクルの短縮を示すエビデンスがあれば、センサー付きドレッシング材をカバーする慢性創傷バンドルに資金を提供しています。ドイツの病院は、新たな褥瘡報告義務に対応するためにAIガイド付き画像診断を採用し、器具の交換を促しています。英国では、ポータブル画像タブレットを活用した地域看護師主導の糖尿病足プログラムを展開。一方、南欧州では、EU医療機器規制(MDR)文書に適合する費用対効果の高いハイドロゲルを追求し、中堅サプライヤーにニッチを創出しています。

アジア太平洋地域は、2030年までのCAGRが6.12%と、創傷ケア管理機器市場において最も勢いのある地域です。中国の集中一括調達方式にはNPWTポンプが含まれるようになり、価格上限を満たすためにキャニスターとフォームドレッシングの現地生産が推進されています。日本では、在宅ケア用ドレッシング材やセンサーパッチに払い戻しを行う高齢化対策が優先され、脆弱な皮膚に適した超薄型シリコーン接着剤の技術革新が促進されます。インドの州保険制度は、糖尿病性足潰瘍のための先進的なドレッシング材を第三次医療施設で保険適用し始め、第二級都市に浸透する販売代理店網の起爆剤となっています。東南アジアでは、民間病院が遠隔皮膚科ポータルを備えた創傷専門クリニックを開設して差別化を図り、地域市場へのリーチを広げています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 慢性創傷および糖尿病性創傷の発生率の上昇

- 世界の手術件数の増加

- 継続的な製品と材料の革新

- 在宅ケアと使い捨てNPWTデバイスへの移行

- AIを活用した創傷画像化と意思決定支援

- 成果に基づく診療報酬改革

- 市場抑制要因

- 新興市場では償還が限定的

- 先進治療の高額な総費用

- 使い捨て製品の環境負荷

- 熟練した創傷ケア看護師の不足

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品別

- 創傷ケア

- ドレッシング

- 伝統的なガーゼとテープによる包帯

- 高度なドレッシング

- 創傷ケアデバイス

- 陰圧閉鎖療法(NPWT)

- 酸素・高圧システム

- 電気刺激装置

- その他の創傷ケア機器

- 局所薬剤

- その他の創傷ケア製品

- 創傷閉鎖

- 縫合糸

- 外科用ステープラー

- 組織接着剤、ストリップ、シーラント、接着剤

- 創傷ケア

- 傷の種類別

- 慢性創傷

- 糖尿病性足潰瘍

- 褥瘡

- 静脈性下肢潰瘍

- その他の慢性創傷

- 急性創傷

- 外科的創傷/外傷

- 火傷

- その他の急性創傷

- 慢性創傷

- エンドユーザー別

- 病院および専門創傷クリニック

- 長期介護施設

- 在宅医療環境

- 購入方法別

- 機関調達

- 小売/OTCチャネル

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 市場シェア分析

- 企業プロファイル

- Solventum

- Smith & Nephew

- ConvaTec Group

- Molnlycke Health Care

- Cardinal Health

- Coloplast

- Paul Hartmann AG

- Medtronic

- B. Braun SE

- Integra LifeSciences

- Essity Medical

- Johnson & Johnson(Ethicon)

- Baxter International

- Organogenesis

- Kinetic Concepts

- Medela AG

- Medline Industries

- Lohmann & Rauscher

- Teleflex Medical

- Devon Medical