|

|

市場調査レポート

商品コード

1444145

デジタルパソロジー:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Digital Pathology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

|

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| デジタルパソロジー:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

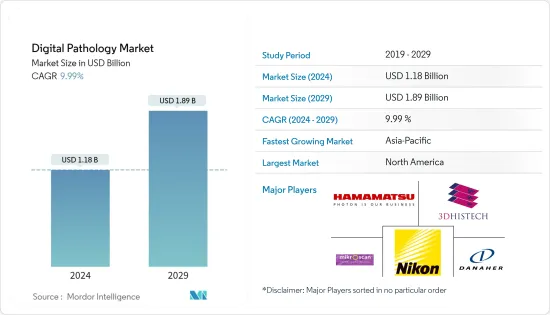

デジタルパソロジー市場規模は2024年に11億8,000万米ドルと推定され、2029年までに18億9,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に9.99%のCAGRで成長します。

COVID-19のパンデミック中、さまざまな国の政府機関、調査機関、多くのバイオテクノロジー企業や製薬企業は、COVID-19の迅速な診断と、パンデミック状況を克服するためのワクチンや新しい治療法の開発のための効果的かつ迅速な技術に焦点を当てました。多くの病理組織部門がすでに人員の減少と業務量の増加に直面していたときに、COVID-19のパンデミックが診断サービスに課題をもたらしました。また、2020年のCOVID-19のパンデミックは、日常的な病理サービスに大きな影響を与えました。デジタルパソロジーは、2020年のパンデミック中に臨床サービスと病理学に基づく調査を保護する上で重要な役割を果たしました。さらに、研究室の拡張への投資と主要メーカーの市場浸透が市場の成長を促進すると考えられます。たとえば、保健福祉省(HHS)の2022年の報告書によると、パンデミック中(2020年3月~2021年2月)の訪問者数は2,800万人を超え、パンデミック前よりも大幅に増加しています。したがって、遠隔医療相談は市場の成長を促進すると予想されます。

遠隔診療の数の増加、検査効率を高めるためのデジタルパソロジーの採用の増加、創薬およびコンパニオン診断における応用の増加が、デジタルパソロジー市場を推進しています。デジタルパソロジーとデジタルツール、バーコーディング、検体追跡、デジタルディクテーションとの統合により、疾患診断におけるデジタルパソロジーの使用も増加しています。これにより、病理検査室での病気の診断の安全性、品質、効率も向上します。たとえば、WHOが発表した記事によると、2022年には、デジタルパソロジーは使いやすさと遠隔作業が可能なため、日常的な病理学の実践をより効率的かつ正確にする大きな可能性を秘めていると予想されています。 Deontics Ltdが2022年 9月に発行したレポートによると、人工知能(AI)ベースの支援システムが診断部門における画像処理を強化しています。これらのインテリジェントAIシステムは、放射線学でも病理学でも、さまざまなアルゴリズムを採用して、臨床医や専門家がより迅速かつ安全な判断を行えるように支援します。

この市場はまた、遠隔病理学の採用の増加、先進国におけるヘルスケアへの投資の増加、発展途上地域における主要メーカーの市場浸透、創薬への注目の高まりによっても牽引されると予想されています。たとえば、2022年 4月、グラクソ・スミスクラインは、がんや非アルコール性脂肪性肝炎(NASH)の薬剤開発にデジタルパソロジー人工知能を導入するためにPathAIを採用しました。さらに、2022年のEU4Health作業プログラムには、デジタル投資のための約7,700万ユーロ(6,514万米ドル)を含む、欧州の医療システムを強化するための8億3,500万ユーロ(7億641万米ドル)以上の予算が割り当てられています。このような政府の取り組みと主要企業による取り組みは、予測期間中に市場の成長を促進する可能性があります。

したがって、遠隔診療の数の増加、検査室の効率を高めるためのデジタルパソロジーの採用の増加、創薬およびコンパニオン診断における応用の増加などの要因が総合的に、予測期間中の調査対象市場の成長を推進しています。ただし、一次診断に対する厳しい規制上の懸念やデジタルパソロジーに関する標準ガイドラインの欠如などの要因により、予測期間中の市場の成長が妨げられる可能性があります。

デジタルパソロジー市場動向

疾患診断セグメントは予測期間中に大きなシェアを占めると予想される

デジタル診断は、病気の原因を特定して理解するのに役立つため、さまざまな慢性疾患の診断において重要な役割を果たします。デジタルパソロジーは、日常診断の主流の選択肢になりつつあります。COVID-19のパンデミックとそれに伴う社会的距離の制限により、デジタルパソロジー市場が後押しされました。 2022年 1月、COVID-19の診断レポートツールを進歩させ、診断ツールの公共利用を迅速化するために、保健福祉省(HHS)は、米国国勢調査局が開発した「TOPxツールキット」を使用した2か月の急遽構築サイクルを組織しました。業界主導の15のチームで構成されています。これにより、個人や組織が陽性/陰性の検査結果を安全に報告することがより簡単になりました。

世界的に、心血管疾患、がん、糖尿病、インフルエンザ、整形外科疾患、神経疾患などの慢性疾患や感染症の負担が増大しており、障害をもたらし、人々の身体的および精神的健康に悪影響を及ぼしています。 2022年 1月に発表された英国心臓財団の統計によると、英国では心血管障害(CVD)が原因で心臓病を患っている人が約760万人います。心血管疾患の負担の増大により、心血管疾患を診断する革新的な技術に対する需要が高まっており、それによって市場の成長を推進しています。

デジタルパソロジーとデジタルツール(バーコーディング、標本追跡、デジタルディクテーション)を統合することで、病理学研究室における疾患診断の安全性、品質、効率が向上します。デジタルパソロジープラットフォームには、一度に症例ごとに入力を提供するために、スライド全体を複数の病理学者に即座に共有する機能が備わっています。たとえば、2021年 1月にロシュは、CE-IVDが各患者にとって最適な治療戦略を決定するのに役立つ、乳がん向けの自動デジタルパソロジーアルゴリズム、uPath HER2(4B5)画像解析およびuPath HER2 Dual ISH画像解析の発表を報告しました。画像分析アルゴリズムは人工知能を使用して、病理学者が患者の乳がんを迅速かつ正確に診断できるようにサポートします。したがって、疾患診断にデジタルパソロジーを使用する利点により、このセグメントは予測期間中に安定した速度で成長すると予想されます。

したがって、慢性疾患や感染症の負荷の増大やデジタルパソロジーの統合などの要因により、疾患診断セグメントは予測期間中に大幅な成長を遂げると推定されています。

予測期間中、北米がデジタルパソロジー市場を独占すると予想される

北米のデジタルパソロジー市場の成長の主な促進要因は、慢性疾患の負担の増大、慢性疾患管理におけるテクノロジーの採用の増加、投資の増加、製品発売の増加、主要な市場プレーヤーによる取り組みです。北米内の米国は調査期間中に大幅に成長すると予想されます。がんやアルツハイマー病などの慢性疾患の負担の増大により、デジタル診断市場が拡大すると予想されています。さらに、国際糖尿病連盟(IDF)は2021年12月に、2021年にはメキシコの推定成人1,400万人が糖尿病を抱えていると発表しました。また、2021年8月に発表されたカナダ政府のプレスリリースによると、糖尿病は糖尿病の一つです。カナダ人が罹患している主要な慢性疾患で、2021年8月時点で300万人以上のカナダ人または人口の8.8%が糖尿病と診断され、カナダ成人の6.1%が糖尿病を発症するリスクが高いとされています。がんによる高い負担により、医療の需要が高まると予想されています。デジタルパソロジーを抑制し、それによって市場の成長を促進します。

この地域での製品やサービスの発売も市場を大きく牽引するでしょう。

さらに、市場の主要企業によるパートナーシップの強化、拡大、投資の増加などの戦略も、この地域のイノベーションを促進し、それによってこの地域の市場を押し上げるでしょう。たとえば、2021年 10月、Neuberg Diagnosticsは米国初の研究所の1つを立ち上げ、米国地域での存在感を拡大しました。 Neuberg Center for Genomic Medicine(NCGM)は、デジタルパソロジーシステムによる次世代シーケンシング(NGS)技術に基づくゲノムおよび分子検査に重点を置いています。

したがって、慢性疾患の負担の増大、慢性疾患管理における技術の採用の増加、主要な市場プレーヤーによる取り組みなどの要因により、予測期間中に北米地域の市場の成長を推進すると予想されます。

デジタルパソロジー業界の概要

デジタルパソロジー市場は、世界的にも地域的にも事業を展開している企業がほとんどないため、本質的に統合されています。競合情勢には、市場シェアを保持しよく知られている数社の国際企業および地元企業の分析が含まれています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 電話相談件数の増加

- ラボの効率を高めるデジタルパソロジーの採用の増加

- 創薬およびコンパニオン診断における応用の増加

- 市場抑制要因

- 一次診断に対する厳しい規制上の懸念

- デジタルパソロジーの標準ガイドラインの欠如

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 製品別

- スキャナー

- ソフトウェア

- ストレージシステム

- その他

- アプリケーション別

- 疾患診断

- 創薬

- 教育・トレーニング

- エンドユーザー別

- 製薬、バイオテクノロジー、企業、CRO

- 病院・基準研究所

- その他

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- 3DHistech Ltd

- Hamamatsu Photonics KK

- Koninklijke Philips NV

- Danaher Corporation(Leica Biosystems Nussloch GmbH)

- Mikroscan Technologies Inc

- Nikon Corporation

- Olympus Corporation

- Proscia Inc.

- F. Hoffmann-La Roche Ltd(Ventana Medical Systems Inc.)

- Visiopharm A/S

- Sectra AG

- Leica Biosystems

- XIFIN, Inc.

第7章 市場機会と将来の動向

The Digital Pathology Market size is estimated at USD 1.18 billion in 2024, and is expected to reach USD 1.89 billion by 2029, growing at a CAGR of 9.99% during the forecast period (2024-2029).

During the COVID-19 pandemic, government organizations in various countries, research institutes, and many biotech and pharmaceutical firms focused on effective and rapid technologies for the fast diagnosis of COVID-19 and to develop vaccines/new therapeutics to overcome the pandemic situation. The COVID-19 pandemic challenged diagnostic services when many histopathology departments already faced a diminishing workforce and increasing workload. Also, the COVID-19 pandemic in 2020, had a profound impact on routine pathology services. Digital pathology played a key role in safeguarding clinical services and pathology-based research during the pandemic 2020. For instance, according to an article published by BMJ Publishing Group Ltd & Association of Clinical Pathologists, in September 2021, there was a large jump in the number of pathologists employing home offices. And the number of primary diagnoses and consultations done via digital pathology significantly increased. Half of the respondents agreed that digital pathology (DP) had facilitated the maintenance of diagnostic practices. Moreover, the investment in laboratory expansion and market penetration of key manufacturers are likely to propel the market growth. For instance, according to the Department of Health and Human Services (HHS) report in 2022, during the pandemic (March 2020- February 2021), there were more than 28 million visits, which is way higher than prepandemic period. Thus, telehealth consultation is expected to boost the market growth.

The increasing number of teleconsultations, rising adoption of digital pathology to enhance lab efficiency, and increasing application in drug discovery and companion diagnostics are driving the digital pathology market. The use of digital pathology in disease diagnosis is also increasing, due to the integration of digital pathology with digital tools, barcoding, specimen tracking, and digital dictation. This also improves the safety, quality, and efficiency of disease diagnoses in pathology laboratories. For instance, according to an article published by WHO, in 2022, digital pathology is expected to have enormous potential to make routine pathology practice more efficient and accurate due to ease of use and the ability to work remotely. As per the report published by Deontics Ltd, in September 2022, artificial intelligence (AI)-based assistance systems are boosting image processing in the diagnostic sectors. These intelligent AI systems can employ a variety of algorithms, whether in radiology or pathology, to assist clinicians and specialists, in making quicker and safer judgments.

The market is also expected to be driven by the increasing adoption of telepathology, rising investment in healthcare in developed countries, market penetration of key manufacturers in the developing region, and an increasing focus on drug discovery. For instance, in April 2022, GlaxoSmithKline recruited PathAI to bring digital pathology Artificial intelligence to cancer, Non-alcoholic steatohepatitis (NASH) drug development. Aditionally, the 2022 EU4Health work program has been allocated a budget of more than EUR 835 million (USD 706.41 million) to boost health systems in Europe, including around EUR 77 million (USD 65.14 million) for digital investment. The creation of the European health data space, which intends to facilitate a greater exchange and access across member states to health data is likely to receive funds from the digital strand. Such government initiatives associated with the technological advancements in the healthcare IT field along with initiatives by the key player are likely to boost the growth of the market over the forecast period.

Therefore, the factors such as increasing number of teleconsultations, rising adoption of digital pathology to enhance lab efficiency, and increasing application in drug discovery and companion diagnostics are collectively driving the studied market growth over the forecast period. However, factors such as stringent regulatory concerns for primary diagnosis and lack of standard guidelines for digital pathology may impede market growth over the forecast period.

Digital Pathology Market Trends

Disease Diagnosis Segment is Expected to Hold Significant Share Over the Forecast Period

Digital diagnosis plays a prominent role in diagnosing various chronic diseases as it helps determine and understand the cause of diseases. Digital pathology is on the verge of becoming a mainstream option for routine diagnostics. The COVID-19 pandemic and the associated social distancing restrictions boosted the digital pathology market. In January 2022, to advance the COVID-19 diagnostic reporting tools and speed up public use of diagnostic tools, Health and Human Services (HHS) organized a hurried, two-month build cycle using the "TOPx Toolkit" developed by the U.S. Census Bureau with 15 industry-led teams. This made it simpler for people and organizations to report positive/negative test results safely.

Globally, there has been an increasing burden of chronic and infectious diseases such as cardiovascular, cancer, diabetes, influenza, orthopaedic and neurology disorders, leading to disability and negatively impacting people's physical and mental well-being. According to the British Heart Foundation statistics published in January 2022, there were approximately 7.6 million people with heart disease in the United Kingdom due to cardiovascular disorders (CVDs). Due to the rising burden of cardiovascular diseases, there is an increasing demand for innovative technologies diagnosing cardiovascular diseases, thereby driving the market's growth.

The integration of digital pathology with digital tools (barcoding, specimen tracking, and digital dictation) improvises the safety, quality, and efficiency of disease diagnosis in pathology laboratories. Digital pathology platform has a provision of instant sharing of whole slides to multiple pathologists, for providing their inputs in a case at a time. For instance, in January 2021, Roche reported CE-IVD launch of its automated digital pathology algorithms, uPath HER2 (4B5) image analysis and uPath HER2 Dual ISH image analysis for breast cancer to help determine the best treatment strategy for each patient. The image analysis algorithms use artificial intelligence to support pathologists in making fast, accurate patient diagnoses of breast cancer. Hence, with the advantages of using digital pathology for disease diagnosis, the segment is expected to grow at a steady rate in the forecast period.

Hence, owing to the factors such as increasing burden of chronic and infectious diseases and integration of digital pathology, the disease diagnosis segment is estimated to witness significant growth over the forecast period.

North America is Expected to Dominate the Digital Pathology Market Over the Forecast Period

The primary driving factors for the growth of the North American digital pathology market are the growing burden of chronic diseases, rising adoption of technologies in chronic disease management, increasing investments, rising product launches, and initiatives taken by the key market players. The United States within North America is expected to grow significantly during the study period. The rising burden of chronic diseases such as cancer, Alzheimer's disease, and others is expected to boost the digital diagnostics market. For instance, the American Cancer Society, 2022 estimated that about 236,740 new cases of lung cancer will be diagnosed in the country in 2022. The same source also states that 79,000 new cases of kidney cancer will be reported in 2022 from Kidney cancer. Furthermore, the International Diabetes Federation (IDF) published in December 2021, an estimated 14 million adults in Mexico were living with diabetes in 2021. Also, as per a press release by the government of Canada published in August 2021, diabetes is one of the major chronic diseases affecting Canadians where over 3 million Canadians or 8.8% of the population were diagnosed with diabetes and 6.1% of Canadian adults were at high risk of developing diabetes as of August 2021. The high burden of cancer is expected to boost the demand for digital pathology, thereby driving the market growth.

The launch of products and services in the region will also drive the market significantly. For instance, in March 2022, Digital Diagnostics and Baxter International Inc. announced a long-term strategic partnership to help front-line care providers deliver high-quality care and improve care outcomes by offering Digital Diagnostics' IDx-DR autonomous AI software as a diagnostic service combined with the Welch Allyn RetinaVue 700 Imager. This combination can give providers a clear view of diagnostic information valuable for a treatment plan, thus driving the market.

Moreover, strategies such as rising partnerships, expansion, and increasing investments by major players in the market will also boost innovation in the region, thereby boosting the market in the region. For instance, in October 2021, Neuberg Diagnostics expanded its presence in the United States region by launching one of the first laboratory in the United States. The Neuberg Centre for Genomic Medicine (NCGM) ill focus on genomic and molecular testing based on next-generation sequencing (NGS) techniques through digital pathology systems.

Thus, owing to the factors such as growing burden of chronic diseases, rising adoption of technologies in chronic disease management, and initiatives taken by the key market players, is expected to drive market growth in North America region during the forecast period.

Digital Pathology Industry Overview

The digital pathology market is consolidated in nature due to the presence of few companies operating globally as well as regionally. The competitive landscape includes an analysis of a few international and local companies that hold the market shares and are well known, including Nikon Corporation, Danaher Corporation (Leica Biosystems Nussloch GmbH), Hamamatsu Photonics KK, Mikroscan Technologies Inc., 3DHistech Ltd, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Number of Tele-consultations

- 4.2.2 Rising Adoption of Digital Pathology to Enhance Lab Efficiency

- 4.2.3 Increasing Application in Drug Discovery and Companion Diagnostics

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Concerns for Primary Diagnosis

- 4.3.2 Lack of Standard Guidelines for Digital Pathology

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD Million)

- 5.1 By Product

- 5.1.1 Scanner

- 5.1.2 Software

- 5.1.3 Storage Systems

- 5.1.4 Other Products

- 5.2 By Application

- 5.2.1 Disease Diagnosis

- 5.2.2 Drug Discovery

- 5.2.3 Education and Training

- 5.3 By End User

- 5.3.1 Pharmaceutical, Biotechnology, Companies and CROs

- 5.3.2 Hospital and Reference Laboratories

- 5.3.3 Other End Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 3DHistech Ltd

- 6.1.2 Hamamatsu Photonics K.K.

- 6.1.3 Koninklijke Philips NV

- 6.1.4 Danaher Corporation (Leica Biosystems Nussloch GmbH)

- 6.1.5 Mikroscan Technologies Inc

- 6.1.6 Nikon Corporation

- 6.1.7 Olympus Corporation

- 6.1.8 Proscia Inc.

- 6.1.9 F. Hoffmann-La Roche Ltd (Ventana Medical Systems Inc.)

- 6.1.10 Visiopharm A/S

- 6.1.11 Sectra AG

- 6.1.12 Leica Biosystems

- 6.1.13 XIFIN, Inc.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS