固定LTE-市場シェア分析、産業動向と統計、成長予測(2025年~2030年)

Fixed LTE - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日

- 商品コード

- 1641989

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

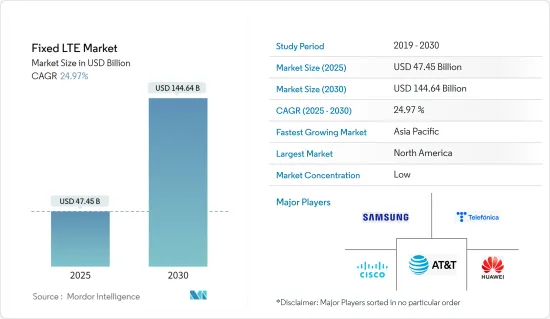

固定LTE市場規模は2025年に474億5,000万米ドル、2030年には1,446億4,000万米ドルに達すると予測、予測期間(2025~2030年)のCAGRは24.97%。

主要ハイライト

- 国際電気通信連合(UN)によると、世界で約270万人がインターネットサービスを利用したことがないといわれています。したがって、世界中の電気通信会社や政府が各家庭でインターネットを利用できるように努力していることから、成長の可能性は高いです。インターネットへのアクセスは基本的な権利であり、デジタルリテラシーは人々、企業、政府の経済的成功に役立ちます。

- 2022年12月、MicrosoftとViasatは、世界中の恵まれないコミュニティにインターネットアクセスを提供するために協力しました。Microsoft Airband Initiativeは、2025年末までに世界中で500万人がインターネットを利用できるようにします。両社は、医療、教育、経済機会の向上のために、重要な市場に接続性とデジタルリテラシーをもたらすことを計画しています。Microsoftとそのパートナーは、エアバンドとともに、すでに5,100万人以上に高速インターネットアクセスを提供しており、その中には米国の十分なサービスを受けていない農村部の400万人以上と、米国外の16の低開発国の4,700万人が含まれています。

- COVID-19の大流行は、私たちの生活、仕事、学習、ビジネスのあり方を劇的に変えました。人々は今や、サービス、サポート、機会にアクセスするために高速インターネットを必要としています。世界中の政府は、地方や遠隔地におけるブロードバンドサービスの拡大に多額の投資を行っています。

- 2022年9月、インド政府は、農村部に強固なデジタルインフラを確立し、全国のすべての村で4Gと5Gのラストマイル・ネットワークへのアクセスを保証するために300億米ドルを投資すると発表しました。高品質で高速なブロードバンド接続を全国の村々に提供し、村々を成長過程に取り込むため、政府は現在、村の起業家によるエコシステム全体を開発しています。

- 固定LTE市場の成長を妨げる大きな課題はないです。しかし、顧客構内設備(CPE)のコストが高いため、ネットワークの設置は遅れると考えられます。より多くのメーカーが市場に参入すれば、価格は低下し、固定LTEの拡大は加速すると考えられます。

固定LTE市場の動向

住宅向けユーザーが大きなシェアを占めると予想

- 住宅エリアにおける固定LTEの需要が急増した背景には、オプションやオンライン教育、ビデオストリーミング、ウェビナー、ビデオ通話など、さまざまな要因があります。サービスプロバイダーは、中断のないネットワークをユーザーに提供するための堅牢なシステムの必要性に気づいた。サービスプロバイダーは、家庭や住宅ユーザー向けの固定LTE技術に投資しており、これが予測期間中の市場成長にプラスの影響を与えると予想されます。

- 2023年1月、Consistent Infosystemsは、ローカル・イーサネット・ベースのWANとGSMネットワークで動作するワイヤレスデュアルバンド4Gルーターを発売しました。このルーターは、農場、畑、倉庫、ガレージ、テラスなどでリモート接続やモニタリングが必要だが、ローカルISPへのアクセスが必要な人や、ローカルインターネットが制限されている地方に住む人々にとって恩恵となります。

- 2022年6月、南アフリカのISP(インターネットサービスプロバイダー)であるSupersonicは、Fixed-LTE Home Solutionsを発表し、ブロードバンド・ポートフォリオを拡大しました。FLTEプランと5Gネットワーク技術により、125カ所の住民に無制限のデータ接続を記載しています。ユーザーは1つのアクセスポイントに複数のデバイスを接続できるようになります。

- 2022年10月、Bharati TelecomはインドでAlways On IoT接続ソリューションを開始しました。このソリューションにより、IoTデバイスはeSIM内の異なるモバイルネットワーク事業者のモバイルネットワークに接続し続けることができます。この接続性は、車両追跡や、遠隔地で作業する機器に汎用的な接続性が求められる場合に役立ちます。

北米が市場で大きなシェアを占める

- 北米の家庭用インターネット市場(FWA)は、T-MobileとVerisonが独占しています。T-モバイルの第3四半期決算によると、T-モバイルはホームインターネット(FWA)顧客を57万8,000人増やし、合計210万人としました。同期間中、Verisonは23万4,000人のFWAユーザーを獲得し、合計で62万人以上となりました。バージョンは企業向けにもFWAを提供しており、その顧客数は44万人を超えています。

- Ericssonは、北米のFWA接続数は2027年までに約2億3,000万になると予測しています。同じ調査で、Ericssonは世界のサービスプロバイダー311社のデータを取得しており、このうち238社がすでに固定無線アクセスを提供しています。

- Nokiaのレポートによると、米国の人口の90%がネットワークソリューションに接続しています。米国の通信事業者の固定ブロードバンド回線の50%以上は、Nokiaの固定ネットワークを利用しています。

- 2022年1月、カナダ政府は地方や遠隔地の住民を高速インターネットに接続するために多額の投資を行っていました。同政府は、オンタリオ州フランボローとライムハウス近郊の農村部の310世帯に高速インターネットを提供する2つのプロジェクトへの資金提供を発表しました。UBF(ユニバーサル・ブロードバンド基金)ラピッド・レスポンス・ストリームに27億5,000万米ドルを投資することで、カナダ政府は2030年までに100%の接続率を達成し、2026年までにカナダ国民の98%を高速インターネットに接続することを目標としています。

- 2022年4月、USCellularはQualcommとInseegoと提携し、Home Internet+ソリューションを発表しました。このソリューションは、居住者だけでなく企業にもワイヤレスで高速インターネットアクセスを記載しています。この5G mmWave高速インターネットサービスは当初、10都市の一部で提供され、最大300Mbpsの速度出力で、4G LTEの家庭用インターネット・スピードの10倍から15倍向上します。UScellularのホーム・インターネットサービスでは、1,220万世帯以上が4G、5G、5G mmWaveの家庭内接続を無制限で利用できます。

固定LTE産業概要

固定LTE市場には多くの参入企業が存在するため、競争は激しいです。AT&T、Huawei Technologies、Cisco Systems Inc.などの市場競合は常に技術革新に取り組んでおり、これが他の中小企業に対する競争優位性を生み出しています。価格競合に耐えるため、各社は定期的に料金体系を変更し、顧客のニーズに応じてカスタマイズした包装を提供しています。

- 2023年1月-バルセロナのケーブル参入企業Coxは、地方向けにモバイルサービスとシンプルな決済プランを推進。特に無制限のデータ通信プランを持たない顧客向けにPay As You Gigプランを開始。停電時の消費者セーフティネットとしてのワイヤレスの活用や、コンバージドサービスの優先的な通信速度が同社の将来展望の一部です。

- 2022年10月-Libyan Post, Telecommunication and Information Technology Company(LPTIC)はCiscoと提携し、デジタルトランスフォーメーションとデータ自動化セグメントのプロジェクトを実施します。このプロジェクトでは、スマート企業、都市、国といった将来の投資対象として有望な事業セグメントを分析します。

- 2022年10月-Vodafoneとフランスの通信事業者Alticeが、ドイツの68億米ドルのファイバー・ブロードバンド・ネットワークの構築で提携。これにより、Deutsche Telekomのような他の通信セクターのライバルを打ち負かすことになります。Alticeの産業専門知識と実績のあるFiber to the Home建設能力により、この契約はVodafoneの次世代ネットワーク拡大の一助となります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因と市場抑制要因の採用

- 市場促進要因

- 公共安全LTE採用の増加。

- 地方における高速ブロードバンド需要の高まり

- DSL、光ファイバー、ケーブルと比較した固定LTEのポジティブな展望

- 市場抑制要因

- ネットワークパフォーマンスへの懸念

- バリューチェーン分析

- 産業の魅力ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- ユーザータイプ別

- 住宅用

- 商業用

- ソリューションタイプ別

- LTEインフラ

- その他のソリューションタイプ(屋内CPE、屋外CPE)

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- その他のアジア太平洋

- ラテンアメリカ

- 中東・アフリカ

- 北米

第6章 競合情勢

- 企業プロファイル

- Huawei Technologies Co. Ltd

- Arris International PLC

- Netgear Inc.

- Sagemcom SAS

- Technicolor SA

- ZyXel Communications Corp

- ZTE Corporation

- Telenet Systems Pvt. Ltd

- Aztech Group Ltd

- Shenzhen Zoolan Technology Co. Ltd

- L-com Global Connectivity

- Samsung Group

- Motorola Solutions Inc.

- Telrad Networks Ltd

- Teltronics(Hytera)

- Telefonica SA

- AT&T Inc.

- Cisco Systems Inc.

- Datang Telecom Technology & Industry Group

第7章 投資分析

第8章 市場機会と今後の動向

目次

The Fixed LTE Market size is estimated at USD 47.45 billion in 2025, and is expected to reach USD 144.64 billion by 2030, at a CAGR of 24.97% during the forecast period (2025-2030).

Key Highlights

- According to the International Telecommunication Union the UN, around 2.7 million people worldwide have never used internet services. Therefore growth potential is high as telecom companies and Governments worldwide strive to get every house access to the internet. Internet access is a fundamental right, and digital literacy helps people, businesses, and governments succeed economically.

- In December 2022, Microsoft and Viasat collaborated to provide underprivileged communities worldwide with internet access. Microsoft Airband Initiative will increase internet availability to 5 million people worldwide by the end of 2025. The duo plans to bring connectivity and digital literacy to critical markets for improved healthcare, education, and economic opportunities. Microsoft and its partners, along with Airband, have already provided high-speed internet access to more than 51 million people, including over 4 million in underserved rural areas of the United States and an additional 47 million in 16 underdeveloped nations outside of the United States.

- The COVID-19 pandemic has drastically changed how we live, work, learn, and conduct business. People now demand high-speed internet to access services, support, and opportunities. Governments around the world are investing heavily in the expansion of broadband services in rural and remote areas.

- In September 2022, the Government of India announced an investment of USD 30 billion to establish a robust digital infrastructure in rural areas and guarantee last-mile network accessibility for 4G and 5G in every village nationwide. To bring high-quality, fast broadband connectivity to every village in the nation and to include them in the growing process, The Government is now developing an entire ecosystem of village entrepreneurs.

- No big challenge can hamper the growth of the fixed LTE market. However, the high cost of customer premises equipment (CPE) will slow the installation of networks. Once more producers join the market, prices may decrease, and the expansion of Fixed LTE will become faster.

Fixed LTE Market Trends

Residential Type of User Expected to Account for Significant Share

- The demand for fixed LTE in residential areas took a steep rise because of multiple factors like people turning to work from options, online education, video streaming, webinars, video calling, and more. The service providers realized the need for a robust system to provide users with an interruption-free network. They invested in fixed LTE technology for home or residential users, which is expected to impact the market's growth over the forecast period positively.

- In January 2023, Consistent Infosystems launched Wireless Dual Band 4G Router that works on local ethernet-based WAN and a GSM network. The router will be a boon to people who need remote connectivity or surveillance in farms, fields, warehouses, garages, terraces, etc. but need access to a local ISP or rural locations with restricted local internet.

- In June 2022, Supersonic, the South African ISP (internet service provider), expanded its broadband portfolio by launching Fixed-LTE Home Solutions. The FLTE plans and 5G network technology will serve residents in 125 locations with unlimited data connectivity. Users will be to connect multiple devices to a single access point.

- In October 2022, Bharati Telecom launched the Always On IoT connectivity solution in India, which allows an IoT device to remain connected to a mobile network from different mobile network operators in the eSIM. The connectivity will be helpful in vehicle tracking or in cases where universal connectivity is required for equipment working in remote locations.

North America Accounts for Significant Share in the Market

- T-Mobile and Verison have dominated North America's home internet market (FWA). According to the third quarter earnings of T-mobile, the telecom had added 0.578 million home internet (FWA) customers to take its total to 2.1 million. During the same period, Verison added 0.234 million FWA users to take its total to more than 0.62 million. Version also provides FWA to businesses and has more than 0.44 million customers for the same.

- Ericsson estimates that North America will have roughly 230 million FWA connections by 2027. In the same study, Ericsson captured the data for 311 global service providers, of which 238 already have a fixed wireless access offering.

- A report by Nokia states that 90% of the US population is connected to network solutions. More than 50% of the telco fixed broadband lines in the United States are powered by Nokia's fixed networks.

- In January 2022, the Government of Canada was investing heavily to connect residents of rural and distant regions to high-speed Internet. The government announced funding for two projects that will bring high-speed Internet to 310 households in rural areas near Flamborough and Limehouse, Ontario. By investing USD 2.75 billion in the UBF (Universal Broadband Fund) Rapid Response Stream, the Canadian government hopes to reach its goal of 100% connectivity by 2030 and connect 98% of Canadians to high-speed Internet by 2026.

- In April 2022, USCellular, in partnership with Qualcomm and Inseego, launched the Home Internet+ solution. The solution provides high-speed internet access wirelessly to residents as well as businesses. This 5G mmWave high-speed internet service will initially be available in parts of 10 cities with a speed output of up to 300 Mbps, a 10 to 15-fold improvement over its 4G LTE home internet speed. More than 12.2 million households can access unlimited 4G, 5G or 5G mmWave in-home connectivity with UScellular's Home Internet service.

Fixed LTE Industry Overview

The fixed LTE market is highly competitive because of many players. Market leaders like AT&T, Huawei Technologies, and Cisco Systems constantly work towards innovation, which gives with a competitive advantage over other smaller players. To withstand price competency, the companies regularly alter their pricing schemes and offer customized packages per customer needs.

- January 2023 - In Barcelona, Cox cable player promotes mobile services and simple payment plans for rural communities. It launched the Pay As You Gig plan, especially for customers without an unlimited data plan. Leveraging wireless as a consumer safety net during outages and prioritized speeds for converged services are some of the future outlooks of the company.

- October 2022 - Libyan Post, Telecommunication and Information Technology Company (LPTIC) collaborated with Cisco, intending to execute projects in the digital transformation and data automation fields. The project will analyze prospective business areas like smart companies, cities, and countries for future investment.

- October 2022 - Vodafone and French Telecom player Altice partnered to build Germany's 6.8 billion USD fiber broadband network. This will help beat the other telecom sector rivals, like Deutsche Telekom. With Altice's industrial expertise and proven fiber-to-the-home construction capabilities, the deal will help Vodafone expand its reach of the next-generation network.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Introduction to Market Drivers and Restraints

- 4.3 Market Drivers

- 4.3.1 Increased Adoption of Public Safety LTE.

- 4.3.2 Growing Demand For High Speed BroadBand In Rural Areas

- 4.3.3 Positive Outlook of Fixed LTE Compared to DSL, Fiber and Cable

- 4.4 Market Restraints

- 4.4.1 Network Performance Concerns

- 4.5 Value Chain Analysis

- 4.6 Industry Attractiveness Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Type of User

- 5.1.1 Residential

- 5.1.2 Commercial

- 5.2 By Type of Solution

- 5.2.1 LTE Infrastructure

- 5.2.2 Other Solution Types (Indoor CPE, Outdoor CPE)

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Rest of the Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Rest of the Asia Pacific

- 5.3.4 Latin America

- 5.3.5 Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Huawei Technologies Co. Ltd

- 6.1.2 Arris International PLC

- 6.1.3 Netgear Inc.

- 6.1.4 Sagemcom SAS

- 6.1.5 Technicolor SA

- 6.1.6 ZyXel Communications Corp

- 6.1.7 ZTE Corporation

- 6.1.8 Telenet Systems Pvt. Ltd

- 6.1.9 Aztech Group Ltd

- 6.1.10 Shenzhen Zoolan Technology Co. Ltd

- 6.1.11 L-com Global Connectivity

- 6.1.12 Samsung Group

- 6.1.13 Motorola Solutions Inc.

- 6.1.14 Telrad Networks Ltd

- 6.1.15 Teltronics (Hytera)

- 6.1.16 Telefonica SA

- 6.1.17 AT&T Inc.

- 6.1.18 Cisco Systems Inc.

- 6.1.19 Datang Telecom Technology & Industry Group

7 INVESTMENT ANALYSIS

8 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 100 Pages

- 納期

- 2~3営業日