|

市場調査レポート

商品コード

1445941

手術部位感染対策: 市場シェア分析、業界動向と統計、成長予測(2024~2029年)Surgical Site Infection Control - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 手術部位感染対策: 市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

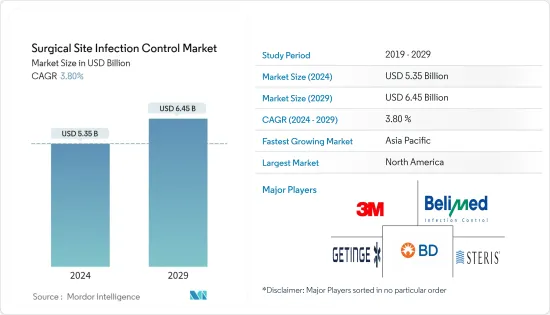

手術部位感染対策市場規模は、2024年に53億5,000万米ドルと推定され、2029年までに64億5,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に3.80%のCAGRで成長します。

COVID-19は、世界中で行われている外科手術に影響を与えました。緊急性のない手術を一切禁止するという規制当局の厳しい指導により、パンデミック期間中、手術件数は大幅に減少しました。たとえば、国立医学図書館が2021年10月に発表した研究によると、全世界で一般外科の入院数が42.8%減少しました。その結果、COVID-19のパンデミックは手術部位感染対策市場に大きな影響を与えました。しかし、COVID-19のパンデミックは、手指衛生と従来の感染制御方法の使用の重要な必要性を強調しました。さらに、待機的手術の再開とCOVID-19の症例の安定化により、市場はすぐにパンデミック前のレベルまで回復しました。

院内感染の増加は、手術総数の増加と高齢者人口の増加が原因です。 UpToDateが2022年 4月に発表した記事によると、手術部位感染(SSI)は手術後の医療関連感染症として最も一般的です。これは、重大な罹患率と死亡率、集中治療室への転送、長期入院、および再入院に関連しています。米国で毎年外科手術を受ける人の中で、2~45人がSSIを発症し、医療システムに重大な負担を与えています。手術部位感染のこのような高い負荷は、市場の成長を促進すると予想されます。

さらに、国連の「World Ageing Population 2022 highlights(2022年世界高齢化人口ハイライト)」によると、世界人口に占める65歳以上の人口の割合は、2022年の10%から2050年には16%に上昇すると予測されています。2050年までに、65歳以上の人の数は世界中の子供の数は、5歳未満の子供の数の2倍以上、12歳未満の子供の数とほぼ同じであると予測されています。したがって、年齢が上がるにつれて、人々はいくつかの慢性疾患にかかりやすくなり、外科的手段が必要となり、予測期間中に手術部位感染対策市場の成長を促進すると予想されます。さらに、保健資源サービス局が2022年3月に発表したデータによると、2021年には米国で約4万件の臓器移植が行われました。さらに、2021年には米国で2万6,670件の腎臓移植と9,236件の生体移植が行われました。したがって、臓器移植の増加により、手術部位の感染が増加し、そのような感染を制御する需要が高まることが予想されます。市場は予測期間中に急騰すると予想されます。

さらに、技術の進歩と外科手術中の手術部位感染の増加により、調査対象の市場の成長がさらに促進されます。たとえば、TELA Bioは2022年 3月に、洗い流さない抗菌ソリューションであるSiteGuardを発売しました。 SiteGuardはNext Science独自のXBIOテクノロジーを利用しており、従来の抗菌剤、消毒剤、宿主の免疫防御に対する細菌の耐性を高めるバイオフィルムに対処することで、手術部位と術後の感染制御をサポートします。

しかし、個人間のSSIに対する意識の欠如により、予測期間にわたって市場は抑制されました。

手術部位感染(SSI)対策市場の動向

表層切開セグメントは、予測期間中に高い成長率を示すと予想されます

表在性切開SSIでは、切開部の皮膚と皮下組織のみが感染します。この感染は、皮膚の切開が行われた領域でのみ発生します。

帝王切開手術の増加と慢性疾患の有病率の増加がこの分野を押し上げると予想されています。たとえば、2021年 6月の世界保健機関(WHO)の最新情報によると、帝王切開の利用は世界的に増加し続けており、出産の5件に1件以上(21%)を占めています。この傾向が続けば、2030年までに、最も高い割合は東アジア(63%)、ラテンアメリカおよびカリブ海諸国(54%)、西アジア(50%)、北アフリカ(48%)、南欧州になる可能性があります(47%)、オーストラリアとニュージーランド(45%)。したがって、そのような手術の症例が増加すると、手術部位の感染症を発症するリスクが高くなり、手術部位感染対策製品の需要が増加し、予測期間中の市場セグメントの成長を促進すると予想されます。

さらに、2021年 5月、Becton, Dickinson, and Companyは、創傷破片を機械的に緩めて除去する最初で唯一のすぐに使用できる水性ポビドンヨード(PVP-I)洗浄液であるBD Surgiphor Sterile Wound Irrigation Systemを発売しました。このような発売は市場の成長を促進すると期待されています。

したがって、手術部位の感染症や院内感染疾患の増加など、上記のすべての要因がこの部門の成長を押し上げています。

北米が大きな市場シェアを獲得し、その優位性を維持すると予想される

手術部位感染対策市場は北米が独占しており、米国が地域収益の最大のシェアを占めています。慢性疾患や手術による入院日数の増加、入院数の増加、感染を制御する機器に実装された革新的な技術と相まって院内感染の負担の増大などが、医療機器市場の成長を後押しすると予想されています。地域。

SSIは、米国の急性期病院の入院患者の間で最も一般的な医療関連感染症(HAI)です(肺炎と関連しています)。 2021年に更新されたCDCデータによると、2019年から2020年の間に中心線血流感染症(CLABSI)が約24%増加し、人工呼吸器関連イベント(VAE)が35%増加しました。このような高い手術部位感染率は、手術部位感染対策(SSIC)製品の必要性を生み出し、市場の成長を推進します。

AHAの2022年のデータによると、2022年の入院者数は約3,335万6,853人でした。これらの入院の多くは、慢性疾患や心臓バイパス手術などの重要な処置によるものでした。したがって、入院数の増加によりSSIの数も増加すると予想され、その結果、この地域の市場が押し上げられることになります。

さらに、2021年 2月、Penn Medicineは、米国フィラデルフィア南西部に最も著名な器具処理および外科用品準備施設の1つである新しいインターベンションサポートセンター(ISC)を開設しました。 ISCはペンシルベニア州で最初のこの種の施設の1つで、スタッフは毎日、基本的なハサミやクランプから高度なロボット器具に至るまで、手術や処置に備えて何千もの器具を滅菌し、梱包します。このような施設の設立も市場の成長を促進すると予想されます。

したがって、上記のすべての要因が予測期間中にこの地域の市場を押し上げると予想されます。

手術部位感染(SSI)制御業界の概要

手術部位感染対策市場は本質的に細分化されています。 3M Company、Becton, Dickinson and Company、Biomerieux SA、Getinge Group、Johnson &Johnsonは、手術部位感染対策市場における重要なプレーヤーです。世界中で絶えず製品が革新されているため、調査対象市場の競争企業間の敵対関係は激化しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 院内感染の予防と管理に関する規制ガイドラインに伴う院内感染の増加

- 手術件数の増加

- 急速に増加する高齢者人口

- 市場抑制要因

- 院内感染の予防と制御に対する認識の欠如

- 外来治療の利用増加

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 製品別

- 手動再処理装置ソリューション

- 消毒剤

- 手指消毒剤

- 皮膚消毒剤

- 外科用スクラブ

- バリカン

- 手術用ドレープ

- 外科的洗浄

- 皮膚準備液

- 医療用不織布

- 手術用手袋

- その他の製品

- 手術・処置別

- 白内障手術

- 帝王切開

- 歯科修復

- 胃バイパス

- その他の手術/処置

- 感染症の種類別

- 表層切開SSI

- 深切開SSI

- 臓器または宇宙SSI

- エンドユーザー別

- 病院

- 外来手術センター

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東およびアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- 3M

- Becton, Dickinson and Company

- Belimed AG

- Getinge Group

- Johnson &Johnson

- Kimberly-Clark Corporation

- Sotera Health

- Ansell Limited

- Steris Corporation

- Lac-Mac Limited

- Pacon Manufacturing Corp.

- American Polyfilm Inc.

第7章 市場機会と将来の動向

The Surgical Site Infection Control Market size is estimated at USD 5.35 billion in 2024, and is expected to reach USD 6.45 billion by 2029, growing at a CAGR of 3.80% during the forecast period (2024-2029).

COVID-19 had an impact on surgical operations performed globally. Due to regulatory authorities' strict guidance to prevent any non-emergent surgeries, the volume of surgeries drastically decreased throughout the pandemic. For instance, according to the study published in October 2021 by the National Library of Medicine, there was a 42.8% decrease in general surgery admissions globally. As a result, the COVID-19 pandemic substantially impacted the surgical site infection control market. However, the COVID-19 pandemic underlined the critical necessity of hand hygiene and the use of conventional infection control methods. Moreover, owing to the resumption of elective surgeries and stabilizing COVID-19 cases, the market soon bolstered to its pre-pandemic levels. For instance, in March 2022, PDI launched Sani-24 Germicidal Disposable Wipe, Sani-HyPerCide Germicidal Disposable Wipe, and Sani-HyPerCide Germicidal Spray, innovative disinfectants to help infection prevention professionals in the fight against rising healthcare-associated infections (HAIs) as well as the ongoing battle against COVID-19.

The increasing number of hospital-acquired infections is due to the rising total number of surgeries and the growing geriatric population. According to an article published in April 2022 by UpToDate, surgical site infection (SSI) is the most common healthcare-associated infection following surgery. It is associated with significant morbidity and mortality, transfer to an intensive care unit setting, prolonged hospitalizations, and hospital readmission. Among those who undergo surgical procedures annually in the United States, 2 to 45 will develop an SSI, representing a significant burden on the health care system. Such a high burden of surgical site infection is expected to drive the market's growth.

Furthermore, according to the United Nations' World Ageing Population 2022 highlights, The share of the global population aged 65 years or above is projected to rise from 10% in 2022 to 16% in 2050. By 2050, the number of persons aged 65 years or over worldwide is projected to be more than twice the number of children under 5 years and about the same that of children under 12 years. Thus, with the growing age, people are more prone to several chronic diseases and need surgical measures, which are expected to boost the growth of the surgical site infection control market over the forecast period. Moreover, as per the data published by the Health Resources and Services Administration in March 2022, about 40,000 organ transplants were performed in the United States in 2021. In addition, 26,670 kidney transplants and 9,236 live transplants were performed in 2021 in the United States. Therefore, the increased organ transplant is expected to increase surgical site infections and increase the demand for the control of such infections. The market is expected to see a surge over the forecast period.

Additionally, technological advancements, and an increase in the number of surgical site infections during surgical procedures, further drive the growth of the market studied. For instance, in March 2022, TELA Bio launched SiteGuard, a no-rinse antimicrobial solution. SiteGuard utilizes Next Science's proprietary XBIO Technology that supports surgical site and post-operative infection control by addressing the biofilms that make bacteria more resistant to traditional antimicrobial agents, disinfectants, and host immune defenses.

However, a lack of awareness about SSI among individuals restrained the market over the forecast period.

Surgical Site Infection (SSI) Control Market Trends

Superficial Incisional Segment is Expected to Exhibit Fast Growth Rate Over the Forecast Period

Only the skin and subcutaneous tissue of the incision are infected in a superficial incisional SSI. This infection occurs only in the areas where the incision was made on the skin.

The rising cesarean surgeries and increasing prevalence of chronic diseases are expected to boost the segment. For instance, According to World Health Organization (WHO) updates from June 2021, cesarean section use continues to rise globally, accounting for more than 1 in 5 (21%) childbirths. If this trend continues, by 2030, the highest rates are likely to be in Eastern Asia(63%), Latin America and the Caribbean (54%), Western Asia (50%), Northern Africa (48%), Southern Europe (47%) and Australia and Newzealand (45%). Thus, the increasing cases of such surgeries have a higher risk of developing surgical site infections, which is expected to increase the demand for surgical site infection control products and boost the market segment's growth over the forecast period.

Additionally, in May 2021, Becton, Dickinson, and Company launched BD Surgiphor Sterile Wound Irrigation System, the first and only ready-to-use aqueous povidone-iodine (PVP-I) irrigation solution that mechanically loosens and removes wound debris. Such launches are expected to propel the growth of the market.

Thus, all the factors above, such as rising surgical site infections and hospital-acquired disorders, boost the segment's growth.

North America Captured the Large Market Share and is Expected to Retain its Dominance

The surgical site infection control market has been dominated by North America, with the United States accounting for the largest share of regional revenue. The increase in hospital stays due to chronic diseases and surgeries, the rising number of hospital admissions, the increasing burden of hospital-acquired infection coupled with the innovative technologies implemented in devices that control infection, and others are expected to boost the market's growth in the region.

SSIs are the most common healthcare-associated infection (HAI) among inpatients in acute care hospitals in the United States (tied with pneumonia). According to the CDC data updated in 2021, about a 24% increase in central line bloodstream infection (CLABSI) and a 35% increase in Ventilator-Associated events (VAE) between 2019-2020. Such a high surgical site infection rate creates the need for Surgical Site Infection Control (SSIC) products and thus propels the growth of the market.

According to 2022 data from the AHA, there were approximately 33,356,853 hospital admissions in 2022. Many of these admissions were due to chronic diseases and critical procedures, like heart bypass surgery. Thus increasing number of hospital admissions is expected to have more SSIs, thereby boosting the market in the region.

Additionally, in February 2021, Penn Medicine opened its new Interventional Support Center (ISC), one of the most prominent instrument processing and surgical supply preparation facilities in Southwest Philadelphia, United States. The ISC is one of the first facilities of its kind in Pennsylvania, where staff will sterilize and package thousands of instruments each day in preparation for surgeries and procedures, from basic scissors and clamps to advanced robotic instruments. Establishing such facilities is also expected to propel the market's growth.

Thus, all factors above are expected to boost the market in the region over the forecast period.

Surgical Site Infection (SSI) Control Industry Overview

The surgical site infection control market is fragmented in nature. 3M Company, Becton, Dickinson and Company, Biomerieux SA, Getinge Group, and Johnson & Johnson are some significant players in the surgical site infection control market. The competitive rivalry of the market studied has intensified, owing to the constant product innovations worldwide.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in Hospital Acquired Infection Along with Regulatory Guidelines for Hospital Infection Prevention and Control

- 4.2.2 Increasing Number of Surgeries

- 4.2.3 Rapidly Growing Geriatric Population

- 4.3 Market Restraints

- 4.3.1 Lack of Awareness of Hospital Infection Prevention and Control

- 4.3.2 Increased Use of Outpatient Treatment

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value in USD Million)

- 5.1 By Product

- 5.1.1 Manual Reprocessors Solution

- 5.1.2 Disinfectants

- 5.1.2.1 Hand Disinfectants

- 5.1.2.2 Skin Disinfectants

- 5.1.3 Surgical Scrubs

- 5.1.4 Hair Clippers

- 5.1.5 Surgical Drapes

- 5.1.6 Surgical Irrigation

- 5.1.7 Skin Preparation Solution

- 5.1.8 Medical Nonwovens

- 5.1.9 Surgical Gloves

- 5.1.10 Other Products

- 5.2 By Surgery/Procedure

- 5.2.1 Cataract Surgery

- 5.2.2 Cesarean Section

- 5.2.3 Dental Restoration

- 5.2.4 Gastric Bypass

- 5.2.5 Other Surgeries/Procedures

- 5.3 By Type of Infection

- 5.3.1 Superficial Incisional SSI

- 5.3.2 Deep Incisional SSI

- 5.3.3 Organ or Space SSI

- 5.4 By End-User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 3M

- 6.1.2 Becton, Dickinson and Company

- 6.1.3 Belimed AG

- 6.1.4 Getinge Group

- 6.1.5 Johnson & Johnson

- 6.1.6 Kimberly-Clark Corporation

- 6.1.7 Sotera Health

- 6.1.8 Ansell Limited

- 6.1.9 Steris Corporation

- 6.1.10 Lac-Mac Limited

- 6.1.11 Pacon Manufacturing Corp.

- 6.1.12 American Polyfilm Inc.