|

市場調査レポート

商品コード

1445867

美容フィラー: 世界市場シェア分析、業界動向と統計、成長予測(2024~2029年)Global Aesthetic Fillers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 美容フィラー: 世界市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 102 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

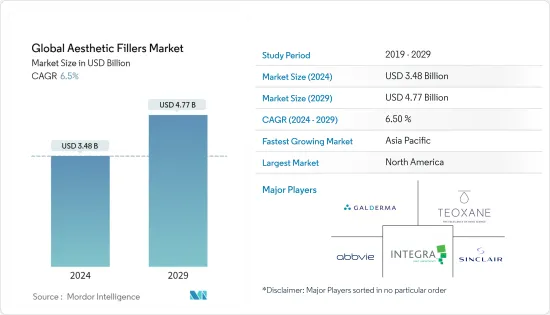

世界の美容フィラー市場規模は、2024年に34億8,000万米ドルと推定され、2029年までに47億7,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に6.5%のCAGRで成長します。

COVID-19の発生により、公衆の移動が減少し、外科的処置や検査プログラムが即時ではなく延期され、ヘルスケア業界に大きな影響を与えました。したがって、COVID-19の感染者数の増加は、美容整形の手術率に短期的な影響を与えると予想されます。外科領域に対する短期的な影響はそれほど顕著ではありません。ただし、世界経済に対するCOVID-19の悪影響は、市場の外科分野に重大な間接的な影響を与える可能性があります。 2021年10月に発表された「インドの整形手術費用」というタイトルの調査記事によると、多くの人が見た目を改善したり身体の変形を治すために美容整形や整形手術を受けることを選択しています。形成外科は一般的に美容処置とみなされているため、高額な費用がかかります。インドの美容外科医と形成外科医は、1回の施術につき10,000ルピーから200,000ルピーの料金を請求する場合があります。また、材料費、外科医の費用、部屋の費用、フォローアップの予約費用などに基づいてコストも倍増します。現在のパンデミックにより、徴収される料金が約20%減少する可能性があり、調査対象の市場にマイナスの影響を与えることが予想されます。

美容フィラー市場の成長は、アンチエイジング治療を使用する傾向の増加と、より若々しいライフスタイルへの需要に起因すると考えられます。世界的に、美容処置の傾向が高まっています。これは主に、人々が見た目や施術の進歩に注目するようになり、より良い結果が得られることに起因しています。たとえば、ドイツ、イタリア、スペインなどの国々では、美容処置の実施数が増加しています。さらに、かなりの数の形成外科があり、さまざまな美容処置が市場を牽引すると予想されます。たとえば、2020年から2021年の美容整形外科国立データバンクの統計によると、腹部形成術、臀部増大術、脂肪吸引などの全体的な美容整形手術は2020年以来63%増加しました。しかし、豊胸術、豊胸/バストリフト、そして胸のリフト/縮小は48%増加しました。

アンチエイジング治療を利用する傾向が高まり、真皮フィラー手術の増加に伴う組織フィラーの受け入れが増加していることにより、多くの市場開発活動が生まれています。たとえば、2022年8月、アッヴィの傘下企業であるアラガン・エステティックスは、中等度から重度の顎の輪郭を失った21歳以上の成人の顎の輪郭の鮮明化を目的としたJUVEDERM VOLUX XCの米国食品医薬品局(FDA)の承認を発表しました。意味。同様に、2022年 1月に米国食品医薬品局(FDA)はRHA Redensityの承認を発表しました。スイスのヒアルロン酸製品製造会社Teoxaneが製造するRHA Redensityは、顔の組織の特定の領域に注入して線やしわを軽減するゲルインプラントまたは皮膚充填剤です。その急速な成長率により、多くの新興企業がこの市場に引き寄せられています。新しい手術のイントロダクションと実施に取り組んでいる病院が、調査対象の市場の成長をリードしています。その結果、拡大し続ける皮膚充填剤の範囲と実施される手術数に対する需要が、調査対象の市場の成長を押し上げています。しかし、皮膚充填剤に関連する副作用やその他の要因が、研究対象となっている市場の成長を妨げています。

ただし、皮膚充填剤に関連する副作用と未登録の開業医による悪影響は、予測期間中の世界市場の成長を妨げると予想されます。

美容フィラー市場動向

ヒアルロン酸セグメントは予測期間中にかなりの市場シェアを保持

ヒアルロン酸は人間の体内にも存在する天然物質です。高濃度の酸が軟結合組織と目の周囲の体液に存在します。一部の軟骨や皮膚組織にも存在します。パーソナルケアに対する世界の注目の高まりにより、多くのパーソナルケア製品や化粧品におけるヒアルロン酸の需要が増加しています。変形性関節症の蔓延により、ヒアルロン酸は関節内補充療法の治療に不可欠であるため、ヒアルロン酸の需要が増加するとも予想されます。さらに、市場の拡大にプラスの影響を与えると予想されるのは、ヒアルロン酸のさらなる利点を特定するための調査への投資と可処分所得の増加です。ヒアルロン酸ベースのフィラーは、過去数年間で最も使用される軟組織フィラー増強剤になりました。彼らは、使用可能ないくつかの新製品により、美容フィラー市場に革命を起こすことに貢献しました。

FDA承認のヒアルロン酸フィラーには、Belotero Balance、Juvederm製品(Juvederm XC、VOLBELLA、VOLUMA、およびVOLLUR)、およびRestylane製品(Restylane、Restylane Refyne、Restylane Silk、Restylane Lyft、およびRestylane Defyne)が含まれます。 2022年4月に発表された「カナダの単一診療所で2139人の患者にVYCフィラー注射後の遅発性結節の発生率と治療」と題された記事によると、ヒアルロン酸(HA)フィラーは顔の若返りに広く使用されており、臨床現場でも安全であるとされています。初期の非動物安定化HA(NASHA)充填剤に対する遅発性過敏症反応の発生率は0.02%~0.4%と推定されています。したがって、ヒアルロン酸の多用は部分的な成長を促進すると期待されます。

さらに、FDAによる新しいヒアルロン酸ベースの美容フィラーの製品承認が頻繁に行われていることが、市場関係者間の激しい競合の原因となっています。多くの組織が皮膚充填剤の新製品の発売に注力しています。たとえば、2020年10月、IBSA Dermaは、唇を強化する治療に使用される非侵襲性HA皮膚充填剤であるAliaxin LV-Lips Volumeを発売しました。ヒアルロン酸は肌のケアに欠かせない素材として需要が大幅に高まっています。したがって、市場は今後数年間で成長すると予想されています。したがって、上記の要因がこのセグメントの市場成長を促進すると予想されます。

北米は最大の市場シェアを獲得し、その優位性を維持すると予想される

地理的には、北米が審美用フィラー市場全体を支配しており、米国が市場への主要な貢献国となっています。最近、世界中の消費者が自分の美的外観にますます関心を示しています。

米国形成外科学会(ASPS)によると、学会認定の形成外科医は、2020年にCOVID-19の影響で待機的外科手術の実施を平均8.1週間、または年間の15%中止したと報告しました。昨年行われた手術の総数は減少しました。この増加は、安全で効果的な低侵襲手術と副作用の少なさに起因すると考えられます。 Restylane Kysseと呼ばれる唇やシワのための新しいヒアルロン酸皮膚充填剤が、ガルデルマを含むいくつかの企業によって導入されました。さらに、しわやひだ用のTeoxane Resilient Hyaluronic RHAフィラーがRevanceによって導入されました。最先端の製剤を使用したこれらの最先端の医薬品に惹かれる患者が増えています。これらの新しく配合された皮膚充填剤配合物が入手しやすくなった結果、侵襲性の低い美容処置に対するニーズが時間の経過とともに高まっています。副作用が最小限に抑えられることから、先進国でも美容整形への要望が高まっています。米国形成外科医協会によると、2020年には米国だけで340万件以上の軟部組織フィラー治療が実施されました。

さらに、2020年2月、美容および整形外科分野で次世代技術を開発するカナダ企業であるRepliCel Life Sciences Inc.は、商用グレードの自動RepliCel皮膚注射器および消耗品の最初の生産を発注したと発表しました。 RCI-02皮膚注射器は、細胞、皮膚充填剤、薬物、生物製剤などのさまざまな注射可能な物質を送達するように設計された電動注射装置です。したがって、これらの要因により、美容フィラー市場は国を後押ししており、市場で重要な位置を獲得しています。

美容フィラー業界の概要

調査対象の市場は非常に細分化されており、製造事業の大部分は北米諸国にあります。調査対象市場には多数のプレーヤーが存在しており、特にAbbVie Inc.、Vital Esthetique、Galderma Pharma SA、Teoxane、Sinclair Pharma PLCなどの企業の製品価格に影響を与えます。業界では一連の買収や合併が起きています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 高まるフェイシャルエステの需要

- 真皮フィラー手術の増加に伴う組織フィラーの受け入れの増加

- 高齢者の間で顔の美容に対する注目が増加

- 市場抑制要因

- 皮膚充填剤に関連する副作用

- 無登録医師による悪影響

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 製品タイプ別

- 吸収性

- 非吸収性

- 材料タイプ別

- ポリマー・粒子

- コラーゲン

- ヒアルロン酸

- 用途別

- フェイスライン補正

- フェイスリフト

- リップトリートメント

- その他

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- AbbVie Inc.

- BioPlus Co. Ltd.

- Bioxis Pharmaceuticals

- Galderma Pharma SA

- Laboratoires Vivacy SAS

- Merz Pharma

- SCULPT Dermal Fillers Ltd.

- Sinclair Pharma

- Suneva Medical Inc.

- Teoxane

- Vital Esthetique

第7章 市場機会と将来の動向

The Global Aesthetic Fillers Market size is estimated at USD 3.48 billion in 2024, and is expected to reach USD 4.77 billion by 2029, growing at a CAGR of 6.5% during the forecast period (2024-2029).

The COVID-19 outbreak resulted in decreased public mobility and impacted the therapeutic and surgical industry significantly, as the surgical procedures and screening programs are non-immediate and are postponed decreasing the burden on healthcare infrastructure. Thus, the rising COVID-19 cases are expected to have a short-term impact on surgical rates of cosmetic procedures. The short-term effects on the surgical segment are less prominent. However, the adverse impacts of COVID-19 on the global economy may have significant indirect effects on the surgical segment of the market. According to a research article titled 'Plastic Surgery Cost in India' published in October 2021, many people opt for cosmetic or plastic surgery to improve their looks or fix physical deformities. Since plastic surgery is typically considered an aesthetic procedure, it involves high costs. Cosmetic surgeons and plastic surgeons in India may charge anywhere between INR 10,000 to INR 200,000 per sitting. The cost also multiplies based on material costs, surgeon fees, room costs, follow-up appointment costs, etc. The current pandemic may result in an approximately 20% decrease in collected fees, which is expected to show a negative impact on the market studied.

The growth of the aesthetic fillers market can be attributed to the increasing trend of using anti-aging treatments and the demand for a much younger lifestyle. Globally, there has been a rising trend of aesthetic procedures. This is majorly attributed to the increasing focus of people on appearance and advancements done in the procedures, which provides better outcomes. For instance, countries, such as Germany, Italy, and Spain, are witnessing a rise in the number of aesthetic procedures performed. Additionally, there is a significant number of plastic surgeries and different aesthetic procedures are expected to drive the market. For instance, according to Aesthetic Plastic Surgery National Databank Statistics for 2020-2021, overall aesthetic body procedures such as abdominoplasty, buttock augmentation, and liposuction increased by 63% since 2020. However, Breast procedures such as breast augmentation, augmentation/ breast lift, and breast lift/reductions were up 48%.

The increasing trend of using anti-aging treatments and the rising acceptance of tissue fillers with increasing dermal filler surgeries is giving rise to a number of market development activities. For instance, in August 2022, Allergan Aesthetics, an AbbVie company announced the United States Food and Drug Administration (FDA) approval of JUVEDERM VOLUX XC for the improvement of jawline definition in adults over the age of 21 with moderate to a severe loss of jawline definition. Similarly, in January 2022, the US Food and Drug Administration (FDA) announced the approval of RHA Redensity. Produced by Swiss hyaluronic acid product manufacturing company Teoxane, RHA Redensity is a gel implant or dermal filler that is injected in specific areas of facial tissue to reduce the appearance of lines and wrinkles. Due to its rapid growth rate, many new companies are getting attracted to this market. Hospitals working on the introduction and implementation of new surgeries are leading the growth of the market studied. Consequently, the demand for the ever-expanding range of dermal fillers and the number of operations performed has boosted the growth of the market studied. However, the side effects associated with dermal fillers and other factors are hindering the growth of the market studied.

However, side effects associated with dermal fillers and the negative effects of unregistered practitioners are expected to impede the growth of the global market in the forecast period.

Aesthetic Fillers Market Trends

Hyaluronic Acid Segment Holds the Significant Market Share Over the Forecast Period

Hyaluronic acid is a natural substance that is also found in the human body. High concentrations of acid are present in soft connective tissues and the fluid surrounding the eyes. It is also present in some cartilage and skin tissue. The demand for hyaluronic acid in much personal care and cosmetic products has increased as a result of the world's noticeable increase in attention to personal care. The prevalence of osteoarthritis is also anticipated to increase hyaluronic acid demand because it is essential for the treatment of viscosupplementation. Additionally anticipated to positively impact market expansion are investments in research to identify additional advantages of hyaluronic acid and rising disposable income. Hyaluronic acid-based fillers became the most used soft tissue filler augmentation agents over the past few years. They helped revolutionize the aesthetic fillers market with several new products available for use.

The FDA-approved hyaluronic acid fillers include Belotero Balance, Juvederm products (Juvederm XC, VOLBELLA, VOLUMA, and VOLLUR), and Restylane products (Restylane, Restylane Refyne, Restylane Silk, Restylane Lyft, and Restylane Defyne). As per an article titled 'Incidence and treatment of delayed-onset nodules after VYC filler injections to 2139 patients at a single Canadian clinic' published in April 2022, Hyaluronic acid (HA) fillers are widely used in facial rejuvenation and be safe in clinical practice. The incidence of delayed-onset hypersensitivity reactions to earlier nonanimal stabilized HA (NASHA) fillers has been estimated at 0.02%-0.4%. Thus, the high usage of hyaluronic acid is expected to promote segmental growth.

Furthermore, frequent product approvals by the FDA for new hyaluronic acid-based aesthetic fillers are responsible for the intense competition among market players. Numerous organizations are focusing on new product launches for dermal fillers. For instance, in October 2020, IBSA Derma launched its Aliaxin LV - Lips Volume, a non-invasive HA dermal filler used for the treatment to enhance lips. The demand for hyaluronic acid is increasing significantly, as it is an essential material that takes care of the skin. Thus, the market is expected to witness growth in the coming years. Therefore, the above-mentioned factors are expected to drive the market growth of the segment.

North America captured the Largest Market Share and is expected to Retain its Dominance

Geographically, North America dominated the overall aesthetic filler market with the United States accounting for the major contributor to the market. Recently, consumers, around the world are showing increasing interest in their aesthetic appearance.

According to the American Society of Plastic Surgeons (ASPS), the Society board-certified plastic surgeons reported they stopped performing elective surgical procedures for an average of 8.1 weeks in 2020 due to COVID-19, or 15 percent of the year, which mirrors the decline in the total number of procedures performed last year. The increase was attributed to the safe and effective minimally invasive procedure and lesser side effects. A new hyaluronic acid dermal filler for the lips and wrinkles called Restylane Kysse was introduced by several businesses, including Galderma. Additionally, Teoxane Resilient Hyaluronic RHA fillers for wrinkles and folds were introduced by Revance. More patients are drawn to these cutting-edge medications with cutting-edge formulations. The need for less invasive cosmetic procedures has risen over time as a result of the accessibility of these newly formulated dermal filler formulations. The desire for cosmetic operations is also rising in industrialized nations due to their minimal adverse effects. According to the American Society of Plastic Surgeons, more than 3.4 million soft tissue filler treatments were carried out in the United States alone in 2020.

Furthermore, in Feb 2020, RepliCel Life Sciences Inc., a Canadian company developing next-generation technologies in aesthetics and orthopedics, announced that it had ordered the first production run of commercial-grade automated RepliCel dermal injectors and consumables. RCI-02 dermal injector is a motorized injection device designed to deliver a variety of injectable substances, including cells, dermal fillers, drugs, or biologics. Thus, owing to these factors, the aesthetics fillers market is boosting the country and gaining a significant place in the market.

Aesthetic Fillers Industry Overview

The market studied is highly fragmented, with the majority of the manufacturing operations in North American countries. The presence of a significant number of players in the market studied has an impact on the prices of products by firms, such as AbbVie Inc., Vital Esthetique, Galderma Pharma SA, Teoxane, and Sinclair Pharma PLC, among others. The industry is witnessing a series of acquisitions and mergers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand for Facial Aesthetics

- 4.2.2 Rising Acceptance of Tissue Fillers with Increasing Dermal Filler Surgeries

- 4.2.3 Increased Attention on Facial Aesthetics among Older Population

- 4.3 Market Restraints

- 4.3.1 Side Effects Associated with Dermal Fillers

- 4.3.2 Negative Effects of Unregistered Practitioners

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Product Type

- 5.1.1 Absorbable

- 5.1.2 Non-absorbable

- 5.2 By Material Type

- 5.2.1 Polymers and Particles

- 5.2.2 Collagen

- 5.2.3 Hyaluronic Acid

- 5.3 By Application

- 5.3.1 Facial Line Correction

- 5.3.2 Face Lift

- 5.3.3 Lip Treatment

- 5.3.4 Other Applications

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 AbbVie Inc.

- 6.1.2 BioPlus Co. Ltd.

- 6.1.3 Bioxis Pharmaceuticals

- 6.1.4 Galderma Pharma SA

- 6.1.5 Laboratoires Vivacy SAS

- 6.1.6 Merz Pharma

- 6.1.7 SCULPT Dermal Fillers Ltd.

- 6.1.8 Sinclair Pharma

- 6.1.9 Suneva Medical Inc.

- 6.1.10 Teoxane

- 6.1.11 Vital Esthetique