|

市場調査レポート

商品コード

1851726

無細胞タンパク質発現:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Cell-free Protein Expression - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 無細胞タンパク質発現:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月28日

発行: Mordor Intelligence

ページ情報: 英文 118 Pages

納期: 2~3営業日

|

概要

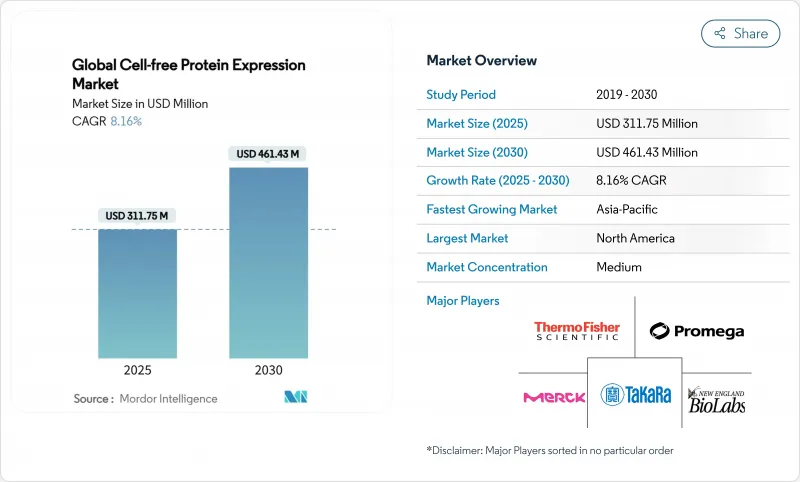

無細胞タンパク質発現の市場規模は、2025年には3億1,175万米ドルに達し、2030年には4億6,143万米ドルに達すると予測されています。

この技術がアカデミックなベンチからcGMPスイートへと移行することで、バイオ製造のワークフローが再構築されつつあります。特に、迅速な設計・構築・試験スケジュールや毒性のあるタンパク質プロファイルが細胞ベースのシステムの課題となっています。米国FDAの先端製造ガイダンスが、商業規模の無細胞施設に対する明確なバリデーションの道筋を示しているように、規制当局の支援も広がっています。合成生物学への戦略的資本流入、溶解液の収率の向上、試薬の標準化の進展により、対応可能な市場は探索研究の枠を大きく超えて拡大しています。一方、アジア太平洋地域はワクチン志向の国家プログラムを背景に急成長しており、北米は医薬品需要の定着により最大の収益基盤を維持しています。競合の激しさは依然として緩やかで、統合プラットフォームプロバイダーはライセートの品質、自動化、エンドツーエンドのワークフローサポートで差別化を図っています。

世界の無細胞タンパク質発現市場の動向と洞察

個別化と迅速なワクチン試作の成長

分散型ワクチン戦略は現在、患者特異的コンジュゲートのオンサイト生産を重視しており、無細胞システムはコールドチェーン依存性を排除しながら、0.50米ドルという低投与コストを実現しています。ノースウェスタン大学のiVAXプラットフォームは、小胞濃縮により収率を91%向上させ、投与あたりのコストを1ドル近くに押し上げました。このような経済性は、凍結乾燥した溶解液の安定性と相まって、大型のステンレス鋼発酵槽では達成できない方法でパンデミック対応策を強化しています。FDAの先進製造フレームワークは、無細胞システムを迅速反応ワクチンの適格経路として明示的に挙げており、臨床応用を加速させています。

オンデマンド生物製剤製造のための無細胞プラットフォームの台頭

契約製造業者は、治療パイプラインが少量多品種の生物製剤へとシフトするにつれて、柔軟性のある施設を拡張しています。サムスンバイオロジクスは60億米ドル、富士フィルムダイオシンスは32億米ドルを、機敏な技術を好む多品種生産工場に投入しました。無細胞ワークフローは、タンパク質合成を細胞増殖から切り離すことで、この戦略に合致しており、ほぼ瞬時にキャンペーンを切り替えることができます。2025年、ベーリンガーインゲルハイムがルベルタマブ・タゼビブリンを製造するために、サトロ・バイオファーマの無細胞プロセスをGMPスケールでフル稼働させたとき、商業的マイルストーンが到来しました。この成功により、安定した収率が検証され、無細胞ラインが抗体薬物複合体に要求される厳しい品質仕様に適合できることが確認されました。

大容量ライセート供給における持続的なギャップ

需要が50mLのベンチ反応から1,000LのcGMPリアクターに移行するにつれ、ライセート活性のバッチ間変動は依然としてアキレス腱です。NIZOのEnzymit社との提携は、酵素組成を安定化させるために連続発酵に重点を置いているが、供給の遅れはアジア太平洋の契約キャンペーンに波及しています。小麦胚芽やヒト細胞エキスのようなニッチ系は、上流のワークフローが複雑なため供給不足に直面し、生産工程での利用が制限されています。バイオリアクターのスケールダウンモデルと標準化された凍結乾燥プロトコルの進歩により、ばらつきは緩和されつつあるが、工業的一貫性はまだ完全には実現されていないです。

セグメント分析

ライセートシステムは2024年の売上高の67.12%を占め、無細胞タンパク質発現市場規模をプロセスの中核に据えています。大腸菌ライセートは、成熟した発酵ノウハウと直線的なスケーラビリティを活用することから優位を占めており、小麦胚芽抽出物は構造研究に不可欠なパラメーターである真核生物タンパク質の優れたフォールディングを実現します。ウサギ網状赤血球と昆虫細胞溶解液は、哺乳類またはバキュロウイルストランスレーション装置が真正性を提供する特殊なニッチを占めています。ヒト細胞溶解液は依然として生産能力に制約があるが、ネイティブの生物学を反映したトランスレーション後修飾のためにプレミアム価格が設定されています。

あらかじめブレンドされたエネルギーミックスや強化されたシャペロンカクテルの標準化により、付属品や消耗品に価値がシフトしており、CAGR8.56%で最も急成長しているサブセグメントです。試薬は現在、生涯運転コストの40%近くを占め、サプライヤーにとって年換算の収益源となっています。シングルユースの反応カートリッジと凍結乾燥エンハンサーペレットはワークフローの再現性を簡素化し、無細胞タンパク質発現市場を支えるハイスループットオートメーションラインと分散製造拠点にとって魅力的な機能です。

トランスレーション専用キットは2024年の売上高の56.65%を占め、その簡便さとmRNAテンプレートライブラリーとの整合が支持されています。これらのキットは、コドンの最適化、開始因子、リボソームの休止を正確に制御することが可能であり、タンパク質の変異体を分析スケールで研究するのに有用です。しかし、トランスクリプションートランスレーション結合システムは、DNA直接入力によるコスト優位性とワークフローのステップ縮小により、CAGR9.71%で拡大しています。プラスミドクローニングをスキップするリニアDNAプロトコールはさらに所要時間を短縮し、AIガイドによるパラメータースイープはマグネシウム、NTP、アミノ酸濃度を同時に最適化します。

この収束は、細胞標準の代謝負担や時間的ペナルティーなしに、細胞力価に近い収量を高めています。ハイスループット施設がマイクログラム当たりのコストとスピードの指標を追い求める中、連成システムは量的シェアを吸収する態勢を整え、より広い無細胞タンパク質発現市場における製品レベルの競争を激化させています。

地域分析

北米は2024年の無細胞タンパク質発現市場の売上高の41.44%を維持し、連邦政府の資金調達メカニズム、深い合成生物学ベンチャープール、新規製造技術を支持する規制環境に支えられています。FDAが高度製造ルートについて明確化したことは、業界の信頼を高め、ベーリンガーインゲルハイムとサトロ・バイオファーマのADC商業化のようなスケールアップ提携の引き金となりました。

アジア太平洋地域は、2030年までのCAGRが9.21%と最も急速に拡大している地域です。シンガポールのmRNAがんワクチン・パイロットプラントへの投資や、韓国のグローバル・ワクチン・ハブという明確な政策目標が、迅速でモジュール化された生産に対する地元での需要を促進しています。細胞・遺伝子治療に関する中国の新たな枠組みは、GMPの透明性を重視する日本と相まって、採用をさらに刺激します。アジアの人口集団の遺伝的不均一性も、無細胞の俊敏性に大きく依存する個別化ワクチンキャンペーンを後押ししています。

欧州では、MHRAのモジュール製造規制が着実に前進しており、分散型無細胞ユニットに自然に適合する、ポイント・オブ・ケアのATMP製造を奨励しています。持続可能性の要請と動物性成分を含まないインプットの選好は、プラットフォームの試薬プロファイルと共鳴し、地域的な受容を高めています。RNAベースの治療技術移転プログラムなど、国境を越えた共同研究が急増し、無細胞タンパク質発現市場におけるこの地域の役割を強化しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 個別化・迅速化ワクチン試作の成長

- オンデマンド生物製剤製造のための無細胞プラットフォームの台頭

- プロテオミクスとゲノミクス分野における研究開発の増加

- 合成生物学のスタートアップ企業への投資急増

- がんやその他の感染症が無細胞タンパク質発現の必要性を高めている

- 無細胞タンパク質発現システムの利点の増加

- 市場抑制要因

- 大容量溶解液供給における永続的なギャップ

- 新興市場におけるCROの認知度の低さ

- 無細胞自動化ワークステーションは初期投資が高め

- 厳しい開発ワークフロー

- バリュー/サプライチェーン分析

- 規制の見通し

- テクノロジーの展望

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品別

- アクセサリー&消耗品

- ライセートシステム

- 大腸菌ライセート

- 小麦胚芽エキス溶解物

- ウサギ網状赤血球溶解液

- 昆虫細胞溶解物

- ヒト細胞溶解物

- その他のライセートシステム

- 発現方法別

- トランスクリプションとトランスレーションの連携

- トランスレーション

- 用途別

- 酵素工学

- ハイスループット生産

- タンパク質ラベリング

- タンパク質間相互作用研究

- ワクチン・治療開発

- その他の用途

- エンドユーザー別

- 製薬・バイオテクノロジー企業

- 学術・研究機関

- CRO &CDMO

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 市場シェア分析

- 企業プロファイル

- Thermo Fisher Scientific Inc.

- Promega Corporation

- Merck KGaA(Sigma-Aldrich)

- Takara Bio Inc.

- New England Biolabs

- Biotechrabbit GmbH

- CellFree Sciences Co., Ltd.

- Cube Biotech GmbH

- GeneCopoeia, Inc.

- Jena Bioscience GmbH

- Creative Biolabs

- Bioneer Corporation

- LenioBio GmbH

- Sutro Biopharma Inc.

- Addgene Inc.

- TAIYO NIPPON SANSO Corporation

- QIAGEN N.V.

- Synthelis biotech

- Arbor Biosciences

- Cayman Chemical

- Nuclera