|

市場調査レポート

商品コード

1852079

インターベンショナルラジオロジー:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Interventional Radiology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| インターベンショナルラジオロジー:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年08月29日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

概要

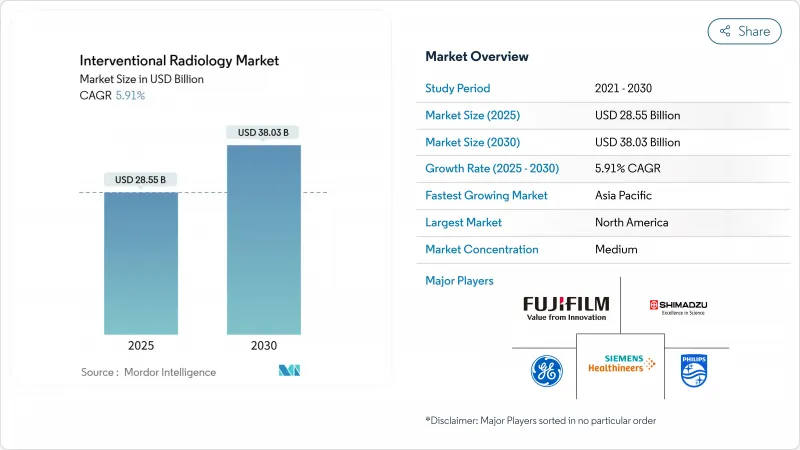

インターベンショナルラジオロジーの市場規模は2025年に285億5,000万米ドル、2030年には380億3,000万米ドルに達すると予測され、CAGRは5.91%で推移します。

開腹手術から低侵襲の画像誘導治療への急速な移行がこの拡大を支えており、回復時間を短縮し、支払者と医療提供者の総支出を削減します。高度な画像処理装置に組み込まれた人工知能は、リアルタイムのガイダンスを向上させ、治療の質を高め、複雑な心臓血管、腫瘍、神経血管の症例における手術件数を刺激します。また、反復的な介入と長期的な疾病管理を必要とする慢性疾患の世界的な増加も、需要の追い風となっています。同時に、外来患者センターは、ペイ・フォー・バリューの償還モデルが費用効率の高いケア設定に報いるにつれて、変化する手技の流れを捉えています。大手メーカーによる研究開発投資の強化は、対応可能な患者プールを拡大し、利益率の高い消耗品の収益源を開拓する機器、ソフトウェア、ロボットの強力なパイプラインを維持しています。

世界のインターベンショナルラジオロジー市場の動向と洞察

慢性疾患と生活習慣病の有病率の上昇

心血管系および腫瘍系の負担が、耐久性のある臨床的利点を提供するカテーテルベースのインターベンションへの需要を高めています。経カテーテル的大動脈弁置換術だけでも2024年には70億米ドル近くを生み出し、持続的な手技の普及を示唆しています。テルモのWEBシステムのような神経血管の進歩は、破裂動脈瘤の閉塞率86.5%を達成し、従来開頭手術で治療されていた適応を拡大した。末梢動脈疾患治療は、アボット社がFDAの認可を受けたEsprit BTK溶解ステントで進歩し、2,000万人以上の罹患者を持つアメリカ人のために設計されました。平均寿命が延びるにつれて、慢性合併症は安定した治療パイプラインを生み出し、インターベンショナルラジオロジー市場の長期的成長を支えています。

低侵襲イメージング技術の絶え間ない進歩

シーメンス・ヘルティニアーズのCiartic Moveに代表されるように、人工知能は透視時間と放射線量を削減し、脊椎と骨盤の手技を最大50%加速します。AIと統合されたロボティクスは、アボット社の治験用伝導系ペーシングプラットフォームで初めて実施されたリードレス左束枝ペーシングを可能にします。RapidAIのLumina 3Dは高品質の神経画像を数分で再構築し、技師不足に対処し、時間に敏感な脳卒中ワークフローをサポートします。フィリップスはエヌビディアとの複数年にわたる協業を通じて、ゼロクリックのスキャン計画を実現するMRI基盤モデルを開発し、イノベーション能力を深化させています。これらの開発により、手技の精度が向上し、プレミアムイメージングスイートにおける差別化が実現します。

ハイブリッド・イメージング・スイートの高い資本コストと運用コスト

血管造影、CT、MRIを組み合わせたハイブリッド・スイートは数百万米ドルを超えることがあり、特殊な遮蔽、空調設備のアップグレード、マルチモーダルソフトウェアの統合が必要となります。継続的なサービス契約とスタッフのトレーニングが総所有コストを引き上げ、予算に制約のある病院での採用を妨げます。シーメンス・ヘルティニアーズは、近代化コストを償却し、機器群を標準化する10年間のバリュー・パートナーシップを通じて、これらの障壁を軽減しています。それにもかかわらず、小規模な施設では、資金調達やプール調達を利用するために合併を追求することが多く、発展していない医療システムでの普及を遅らせています。

セグメント分析

2024年、画像診断システムのシェアは46.34%を維持し、手技計画や手技指導における基本的な役割が強調されました。シーメンスのsyngo DynaCTに搭載されたAI学習による骨除去アルゴリズムなど、継続的な機能アップグレードは、予算が逼迫している中でも、定期的な設備更新サイクルを支えています。しかし、IR消耗品は2030年までのCAGRが7.45%であり、症例数の増加に伴う経常収益の優位性を反映しています。シングルユースのカテーテルや塞栓用コイルは、交差汚染のリスクを低減し、在庫管理を合理化するため、回転率の高い外来ラボにとって魅力的です。消耗品のインターベンショナルラジオロジー市場規模は、治療の複雑性が増すにつれて急速に拡大すると予測されます。

アクセサリーとワークフローソフトウェアは、クラウド分析がモダリティのダウンタイムを短縮し、スケジューリングを最適化するため、ハードウェアの成長を上回る。フィリップスのヘリウムフリーBlueSeal MRIは、1台あたり年間約40MWhを節約し、環境効率が臨床性能を補完することを示しています。AIを活用した線量モニタリング機能を搭載した透視検査システムは、安全性の義務化に対応し、中堅病院にアピールしています。全体として、成熟した画像処理インフラが利益率の高い使い捨ての普及の舞台を整え、インターベンショナルラジオロジー市場全体で収益性の高い拡大を推進しています。

治療的処置はCAGR 7.66%で進んでおり、Merit Medical社のWrapsody細胞不透過性エンドプロテーゼのようなデバイスの画期的な進歩が後押ししています。血管形成術とステント留置術は、アボット社のEsprit BTKプラットフォームなど、薬剤デリバリーを確保しながら血管の治癒をサポートする吸収性スキャフォールドの恩恵を受けています。アブレーション技術の進歩は、予測可能な病変境界をもたらし、側副傷害を縮小することで、腫瘍学や疼痛管理の適応を拡大します。その結果、治療サービスに起因するインターベンショナルラジオロジー市場規模は、セグメントレベルで2030年までに252億米ドルに達すると予測されます。

診断手技は38.23%のシェアを占め、インターベンショニストに不可欠な画像診断のロードマップを提供するが、1件当たりの収益は低いです。とはいえ、コーンビームCTやAI支援血管造影の技術革新は診断精度を高め、間接的に治療拡大を支えています。生検とドレナージは腫瘍の病期分類と感染対策に不可欠であることに変わりはないです。不朽の診断基盤は、治療パイプラインへの安定した患者流入を保証し、より広範なインターベンショナルラジオロジー市場の成長モメンタムを持続させる。

地域分析

北米は2024年の売上高の43.21%を占め、確立された臨床ガイドライン、機器の高い普及率、シーメンス・ヘルティニアーズの米国における1億5,000万米ドルの施設拡張を含む強固な研究開発コミットメントに支えられています。メディケアが2.83%の診療報酬引き下げを実施し、インターベンショナルラジオロジーの診療報酬が4%引き下げられると予測されることから、支払圧力が迫り、医療提供者は費用効率の高い外来設備への投資に拍車がかかります。FDAのTransitional Coverage for Emerging Technologies pathwayのような規制上のイニシアチブは、画期的な医療機器の市場導入を促進し、財政の逼迫にもかかわらず技術革新の流れを維持します。

アジア太平洋地域はCAGR 6.34%と最速の成長を記録しており、大規模なアンメット・ニーズ、都市部での病院建設、合弁事業などがその要因となっています。イナリ・メディカルと6 Dimensions Capitalとの提携は、中国での血栓除去装置の商業化を加速させ、先進治療を現地化する海外と国内の協力関係を示しています。各国政府は医療ツーリズムを抑制するために画像診断インフラと医師養成を優先し、官民提携は地域ネットワーク全体でAIツールを拡張するためにクラウドプラットフォームを活用します。

欧州では、厳格な機器安全基準と強力な大学病院ネットワークに支えられ、安定した拡大を維持しています。フィリップスは2024年に594件の医療技術出願で欧州特許庁をリードし、同地域の技術革新に対する評価を高めました。東欧のシステムは、血管造影ラボのアップグレードに欧州連合(EU)の統合基金を割り当て、手技能力を向上させました。中東・アフリカと南米はまだ始まったばかりだが、タンザニアのRoad2IRプログラムのようなトレーニングイニシアティブが1,500以上の手技を高い成功率で完了させていることから、導入が加速していることがわかる。多国籍OEMは、こうした価値観の強い市場に参入するために融資パッケージを調整し、世界のインターベンショナルラジオロジー市場全体の収益源を多様化しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 慢性疾患と生活習慣病の増加

- 低侵襲イメージング技術の絶え間ない進歩

- 治療領域を超えた用途の拡大

- 外来およびデイケース治療へのシフト

- ハイエンド画像インフラへの設備投資の増加

- 画像誘導手技に対する償還支援の拡大

- 市場抑制要因

- ハイブリッド・イメージング・スイートの高い資本コストと運用コスト

- 厳しい放射線安全規制とコンプライアンス負担

- 熟練したインターベンショナルラジオロジストとスタッフの不足

- 代替血管内治療専門分野からの競争圧力

- 規制情勢

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力/消費者

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品別

- イメージング・システム

- 血管造影システム

- 透視システム

- CTスキャナー

- MRIシステム

- IR消耗品

- カテーテル&ガイドワイヤー

- バルーン&ステントシステム

- 塞栓・血栓除去装置

- アクセサリー&ソフトウェア

- イメージング・システム

- 手術タイプ別

- 診断

- 血管造影

- 生検とドレナージ

- 治療

- 血管形成術とステント留置術

- 塞栓術

- アブレーション

- 診断

- 用途別

- 心臓病学

- 腫瘍学

- 消化器・肝臓領域

- 泌尿器科・腎臓内科

- その他の用途

- エンドユーザー別

- 病院

- 外来手術センター(ASCs)

- オフィスベースのラボ(OBL)とイメージングセンター

- 地理

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 市場シェア分析

- 企業プロファイル

- Siemens Healthineers AG

- GE HealthCare

- Koninklijke Philips NV

- Canon Medical Systems Corp.

- Fujifilm Holdings Corporation

- Shimadzu Corporation

- Hologic Inc.

- Samsung Medison Co. Ltd.

- Boston Scientific Corp.

- Medtronic PLC

- Cook Medical LLC

- Terumo Corp.

- Abbott Laboratories

- Stryker Corp.

- Penumbra Inc.

- AngioDynamics Inc.

- Merit Medical Systems Inc.

- Cardinal Health Inc.

- Teleflex Inc.

- Esaote SpA