|

市場調査レポート

商品コード

1850340

外科手術用ステープラー:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Surgical Stapler - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 外科手術用ステープラー:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月20日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

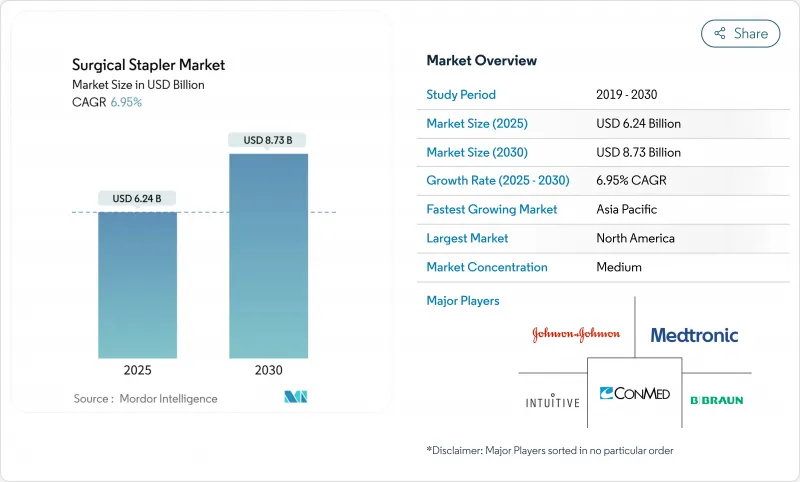

外科手術用ステープラー市場規模は2025年に62億4,000万米ドル、2030年には87億3,000万米ドルに達すると予測、CAGRは6.95%です。

成長の軸となるのは、ロボット手術の急速な統合、リローダブルカートリッジを奨励する病院の持続可能性の義務化、より高い急性期の整形外科手術や肥満手術を後押しする高齢化です。大病院チェーンはOR時間を短縮するために動力式ステープラーを標準化し、外来手術センターは資本予算を節約するためにコスト効率の良い手動式ステープラーを採用しています。また、ISO13485に準拠した品質システムに関する規制が明確化されたことで、機器のアップグレードにおけるコンプライアンスの不確実性が低下したことも、採用のメリットとなっています。これらの要因が相まって、ステープラーはコモディティな閉鎖器具ではなく、データ豊富な手術器具として位置づけられ、世界中で対応可能な手術件数を拡大する進化を遂げています。

世界の外科手術用ステープラー市場の動向と洞察

ロボット支援手術プラットフォームとの統合

ロボットプラットフォームは現在、手首関節用に設計されたステープラーと、組織のフィードバックをミリ秒単位で解釈する予測発射アルゴリズムを搭載して出荷されており、シングルポートまたはマルチポートアクセスによる正確なステープルラインを可能にしています。8,606台のda Vinciシステムの設置ベースは、独自のリロードの安定したプルスルー需要を生み出し、2024年第1四半期のロボット売上高18億9,000万米ドルによって強化された収益モデルとなっています。APACの病院は、ロボット手術室に直行し、混合フリートをサポートし、ベンダーのロックインを低減する、プラットフォームにとらわれないステープラー設計を育成しています。ピアレビューを受けたプロトタイプで紹介された革新的な3アクチュエーター式円形ステープラーは、75度のカートリッジ屈曲を約束し、食道吻合の課題に直接取り組んでいます。次世代システム内のプロセッサが10,000倍に拡張されるにつれて、ステープラーは、個々の組織の厚みに合わせて発射パラメータを調整するリアルタイム分析を組み込み、機器のインテリジェンスを手術現場の端まで押し上げることになります。

低侵襲手術への嗜好の高まり

10mm未満のポートを使って行われる手術は2024年に17%増加し、世界全体で263万例に達します。複雑な前腸や胸郭の手術では、制限の多い腔内で操作できる高度に連結されたステープラーが使用されるようになり、開腹率が低下しています。外来センターでは、セットアップ時間を短縮できるステープラーを求めています。パワードリローダブルステープラーは、ハンドルを何度も握ることなく安定した圧縮を実現することで、このニーズに応えています。2025年4月にSP SureForm 45がFDAから認可されたことは、ステープラーが手技の移動パターンを指示するのではなく、それに従うことを明確に示しています。内蔵されたSmartFireセンサーは、MISアプローチに特有の触感とフィードバックのギャップを埋め、外科医が手技による感触ではなく、デジタル圧縮表示を信頼できるようにします。

術後の感染・漏出事故

使用事例報告では、ステープルラインの漏れが術後数年経ってから小腸閉塞につながったとしており、無差別なステープル使用に対する外科医の警戒心を煽っています。VATS中の血管損傷の発生は、予定外の胸腔切開を引き起こし、ステープル経路の高度な画像診断を促すガイドライン改訂のきっかけとなりました。整形外科の文献では、縫合糸と比較して金属ステープルの感染確率が高く、特に骨が治癒するまでステープルが残ることが示されています。小児の盲腸切除術では、ステープルを留置した場合の年齢特有のリスクが示されています。これらの事象は、癒着しやすい解剖学的構造において縫合または有刺糸を使用する外科医を後押しし、短期的な数量増加を抑制しています。

セグメント分析

2024年の外科手術用ステープラー市場規模の40.74%をリニア機器が占め、断端や吻合が日常的に行われる消化器系や胸部での業務に支えられています。長いカートリッジは、1回のパスで広い組織径をカバーすることにより、スリーブ状胃切除術や肺切除術を合理化し、手術時間や麻酔被ばくを削減します。3列円形ステープラーは、ニッチではあるが、大腸手術における吻合部リークを6.1%から2.1%に削減し、プレミアム価格を維持する標的臨床利益を示しています。カッターの組み合わせは、依然として特殊外傷のシナリオに限られているが、刃の摩耗によって新しいカートリッジが必要になるため、リロードの売上を牽引しています。

年間8.02%の増加が予測されるステープラーのリロードは、外科医のワークフローを変えることなく、ESG目標に向けた迅速な回収経路を調達担当者に提供します。調達データによれば、滅菌のアップタイムが最適化されれば、2年間のライフサイクルにおいて、リロードのコストは完全な使い捨て品よりも30~40%安くなります。一括契約を交渉している病院は、単回使用機器では利用できない、さらなる単位割引を確保しています。その結果、リロード装置は、以前は内視鏡のために確保されていた資本予算項目にますます割り振られるようになり、戦略的ソーシングの課題の中でその足跡を広げています。

腹部手術は、2024年の外科手術用ステープラー市場シェアの36.91%を占め、肥満症、大腸肛門、肝胆膵の症例がスピードと止血のためにステープリングに依存しています。標準化された発射シーケンスにより手術チーム間のばらつきが減少し、病院がバリューベースの購買ベンチマークに準拠するのに役立っています。ロボットシステムは、骨盤深部の大腸吻合に360度の関節を提供することで、臨床での受け入れが拡大し、採用の幅が広がります。

高齢化に伴う膝関節置換術や股関節置換術を背景に、整形外科の需要がCAGR 8.76%で成長します。迅速な皮膚閉鎖により、手術室の回転時間は1症例あたり最大12分短縮され、これは大量の人工関節置換術を行う手術室で1日1枠の増枠につながります。脊椎固定術やスポーツ医学のポータルも、除去のための通院が不要な吸収性ステープラーを採用することで、症例数を増やしています。心臓や胸部の適応症は、肺葉切除術で擦れやすい肺動脈を密封する血管再装填に傾き、子宮摘出術などの産婦人科手術は、正確なステープル留置による出血量減少の恩恵を受けています。

地域分析

北米は2024年の外科手術用ステープラー市場規模の34.57%を占め、最大の株主であり続け、2030年までのCAGRは6.27%になると予測されています。導入されたロボットフリートは安定した消耗品のプルスルーを生み出し、ESGプログラムは無駄を省くリローダブルを促進します。メディケアの一括支払いモデルは再入院の減少に報いるものであるため、病院は経済的マージンを維持するためにステープルラインの漏れを監視するようになっています。しかし、チタン輸入への依存はメーカーを地政学的関税にさらすため、コバルトクロムやバイオポリマーの代替品を模索するメーカーも出てきています。

欧州はCAGR 6.63%で成長し、EUのMDR規則によって品質基準が引き上げられ、先端材料研究が奨励されています。ドイツと英国は、地域のロボット症例の半数以上を占めており、高度に連結されたステープラーの需要を後押ししています。多くの大学病院が調達のカーボンフットプリントを測定しており、その結果、再利用可能なハンドルが北米よりも早く普及しています。現地サプライチェーンはアジア太平洋地域の金属価格の変動からこの地域を保護し、欧州のOEMに原材料ショックの際の継続的な優位性をもたらしています。

アジア太平洋地域は、2030年までのCAGRが8.34%と最も高いです。年間12%のロボット生産能力を追加している中国は、輸出の野望のためにFDAの認可を追い求めながら、輸入品を下回る国内ステープラーブランドを育成しています。インドの110億米ドルの医療機器セクターは、有利な税制優遇措置により2桁成長を見込んでおり、第2級都市病院向けの動力式ステープラーの生産能力拡大を後押ししています。CE認証を取得したAPACのイノベーターは2035年までに世界展開を計画しており、世界的な競合激化が予想されます。中東・アフリカと南米のCAGRはそれぞれ7.82%と7.29%で、医療観光回廊と国の医療ビジョンプログラムに関連した病院インフラ投資が後押ししています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- ロボット支援手術プラットフォームとの統合

- 低侵襲手術への関心の高まり

- 電動式で再装填可能なステープラーの急速な普及

- 高齢者の整形外科手術の増加により、迅速な皮膚閉鎖ソリューションが求められる

- 世界中で肥満および代謝関連手術が急増

- 病院のESGは再利用可能なカートリッジシステムを優先することを義務付けている

- 市場抑制要因

- 機械的ステープルへの依存を軽減する次世代生体接着シーラント

- 術後感染症および漏出事故

- 濃縮チタンの供給が主要原材料の価格を混乱させる

- 厳格な規制上の安全要件とリコール

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 買い手の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 製品別

- リニア外科手術用ステープラー

- 円形の外科手術用ステープラー

- カッターステープラー

- スキンステープラー

- ステープラーリロード

- 用途別

- 腹部手術

- 産婦人科手術

- 心臓・胸部外科

- 整形外科

- その他の外科的用途

- 機構別

- マニュアル

- パワード

- ユーザビリティ別

- 使い捨て

- 再利用可能

- エンドユーザー別

- 病院

- 外来手術センター

- 専門クリニック

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 競合ベンチマーキング

- 市場シェア分析

- 企業プロファイル

- B. Braun Melsungen AG

- Becton, Dickinson and Company

- ConMed Corporation

- EziSurg Medical

- Frankenman International Ltd.

- Grena Limited

- Intuitive Surgical Inc.

- Johnson & Johnson Services, Inc.

- Lexington Medical, Inc.

- Medtronic plc

- Meril Life Sciences Pvt. Ltd.

- Purple Surgical

- Reach Surgical Inc.

- Smith & Nephew plc

- Solventum Corporation

- Standard Bariatrics

- Stryker Corporation

- Surgnova Healthcare Technologies

- Teleflex Incorporated

- Zimmer Biomet Holdings Inc.