|

市場調査レポート

商品コード

1850344

スマート照明:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Smart Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| スマート照明:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月23日

発行: Mordor Intelligence

ページ情報: 英文 154 Pages

納期: 2~3営業日

|

概要

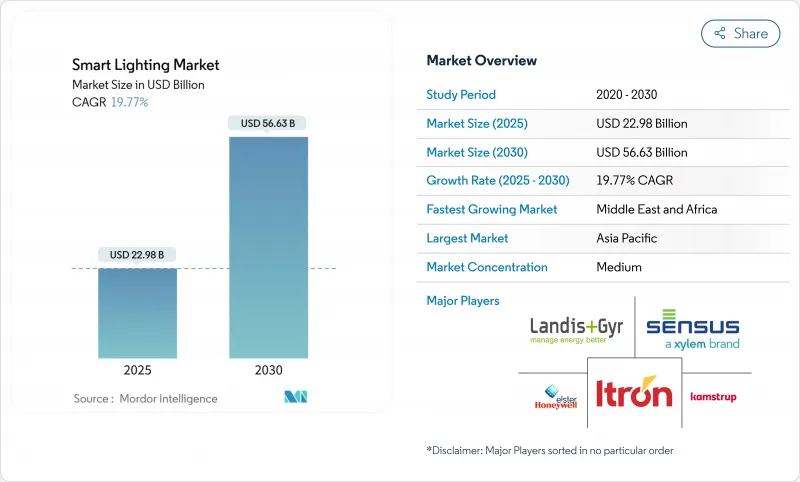

スマート照明の市場規模は2025年に229億8,000万米ドルと推定され、2030年には566億3,000万米ドルに達すると予測されます。

この軌道を支えているのは、規制当局がエネルギー効率の義務付けを強化し、LED部品のコストが低下するにつれて、住宅、商業施設、工業施設での設置が加速していることです。ビル所有者は現在、コネクテッド照明を、電気代を下げ、データ主導の施設管理をサポートし、居住体験を向上させる戦略的プラットフォームと見なしています。ベンダーはエッジAIとクラウド分析を統合して製品の差別化を図り、各国政府はプロジェクト開始時から高度な制御を義務付けるネットゼロ基準を拡大しています。成長機会は特にアジア太平洋で顕著であり、都市化と政策インセンティブがメーカーにスケールメリットをもたらします。

世界のスマート照明市場の動向と洞察

拡大するスマートホームのエコシステム統合

スマート照明システムは現在、全ホームオートメーションプラットフォームを支えています。Matter規格は、独自の障壁を取り除き、異なるブランドのデバイスが統一アプリを通じて通信できるようにします。Philips HueとSamsung SmartThingsの連携により、照明、エンターテイメント、セキュリティが単一のダッシュボードで同期されます。Thread 1.4により、様々なベンダーのボーダールーターがネットワークを共有できるようになり、将来性のある投資に対する消費者の信頼を強化するマイルストーンとなります。

LEDの急速なコスト削減でROIが向上

フリップチップパッケージングなどの先進パッケージングは、10万時間の寿命を維持しながら20%高い効率を実現し、ハイベイサイトのメンテナンスコストを削減します。チップオンボードストリップは、設置の柔軟性を高め、2025年の製品ポートフォリオを再構築します。ユーティリティのリベートと組み合わせることで、これらのコスト削減は、AirPark Northプロジェクトが年間4,990米ドルを節約しているように、多くの商業施設の改修において、投資回収期間を18ヶ月以下に圧縮しています。

無線プロトコルのサイバーセキュリティ脆弱性

調査チームは、Zigbee Light Linkデバイスがデフォルト・キーによってハイジャックされ、企業ネットワークへの側面攻撃が可能であることを示しました。さらにチェック・ポイントは、侵害されたPhilips Hue電球が、より広範なITシステムへの橋頭堡となることを示しました。セキュリティ・クリティカルな環境での急速な導入は、修復コストや法的リスクによって阻まれています。

セグメント分析

2024年のスマート照明市場は、制御システムがCAGR 22.1%で成長し、スマートランプと器具が64.9%のシェアを維持すると予測されます。制御プラットフォームは、センサー、アナリティクス、クラウドダッシュボードを融合し、汎用ランプに勝る経常ソフトウェア収益とマージンをもたらします。Acuity Brandsの12億1,500万米ドルのQSC買収は、同社のインテリジェント・スペース・グループを拡大し、2025年第1四半期のセグメント収益を14.5%押し上げました。

これらのシステムは、エッジAIを使用して稼働パターンを予測し、多くの場合50%を超える省エネを推進します。産業現場はデータストリームを活用してワークフローを最適化し、ハードウェアからインサイトへの戦略的軸足を浮き彫りにしています。対照的に、スマートランプと器具は物理的なレイヤーとして機能するが、LEDコストの低下と量の拡大に伴い、価格圧力に直面しています。

レトロフィット・プロジェクトは、2024年のスマート照明市場規模の52.1%を占める。オーストラリア税務局がレトロフィットによって照明コストを94%削減したように、公共事業による優遇措置と短い投資回収期間がこの分野を魅力的なものにしています。

建築家が設計図の段階からインテリジェント照明を組み込んでいるため、新築の採用率はCAGR 21.3%で上昇しています。カリフォルニア州の2022年基準では、すべての新築物件に高度な制御が義務付けられています。また、グラウンドアップ設置により、Li-Fiや高密度センサーグリッドなど、後から改修するのが面倒な機能が解放されるため、長期的な価値はこのセグメントに傾きます。

スマート照明システム市場は、製品タイプ(制御システム、スマートランプおよび器具)、設置タイプ(新築、改修)、接続技術(Wi-Fi、Bluetooth、その他)、エンドユーザー(住宅、商業施設、その他)、地域別に区分されます。市場予測は金額(米ドル)で提供されます。

地域分析

欧州は、厳しい効率規制と成熟した自動化需要により、2024年の売上高の26.4%を維持。VIVARES Zigbeeアップグレードのようなドイツのレトロフィットは、KfW276補助金の対象となり、政策主導の勢いを証明しました。政府の補助金と炭素目標が、特に公共建物と高級オフィススペースでの継続的な採用を支えています。

アジア太平洋地域は、CAGR19.8%で最速の動きを見せています。中国は2024年に8つの新しい照明基準を導入し、効力の閾値を引き上げてコネクテッド・コントロールを推進することで、国内メーカーのスマート製品ラインの拡大に拍車をかけています。インドのブライトロード・プログラムは、186の都市で従来の電球に取って代わることを目的としており、大規模な調達をネットワーク化されたLEDシステムに誘導しています。香港のオータムライティングフェアなどの地域見本市では、スマートシティ照明に焦点を当てた3,000社の出展があり、サプライチェーンの堅調な拡大を裏付けています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- スマートホームエコシステムの統合拡大

- LEDコストの急速な削減によりROIが向上

- 公益事業資金による需要側管理インセンティブ

- 国家ネットゼロ建築基準(2025~30年導入)

- 倉庫におけるLi-Fi対応照明パイロット

- エッジAI搭載アダプティブディミングアルゴリズム

- 市場抑制要因

- 無線プロトコルにおけるサイバーセキュリティの脆弱性

- 断片化された相互運用性標準

- 希土類リン光体のサプライチェーンの不安定性

- スマートホームのプライバシー規制の不確実性

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

- 市場におけるマクロ経済要因の評価

第5章 市場規模と成長予測

- 製品タイプ別

- 制御システム

- スマートランプと照明器具

- 設置タイプ別

- 新築

- 改造

- コネクティビティテクノロジー別

- Wi-Fi

- Bluetooth

- ジグビー

- その他

- エンドユーザー別

- 住宅用

- 商業用

- 産業

- その他

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- オーストラリアとニュージーランド

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ナイジェリア

- エジプト

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Signify N.V.

- Acuity Brands Inc.

- Hubbell Inc.

- Eaton Corp.

- Lutron Electronics Co. Inc.

- Legrand SA

- Cree Lighting(IDEAL Ind.)

- Samsung Electronics Co. Ltd.

- Xiaomi Corp.

- Snap One LLC(Control4)

- Savant Systems Inc.(GE Lighting)

- Nanoleaf Canada Ltd.

- Sengled Optoelectronics Co.

- Wyze Labs Inc.

- Feit Electric(LIFX)

- Panasonic Corp.

- Opple Lighting

- EGLO Leuchten GmbH

- Zumtobel Group

- Helvar