|

市場調査レポート

商品コード

1444907

組換えタンパク質: 市場シェア分析、業界動向と統計、成長予測(2024年~2029年)Recombinant Protein - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 組換えタンパク質: 市場シェア分析、業界動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

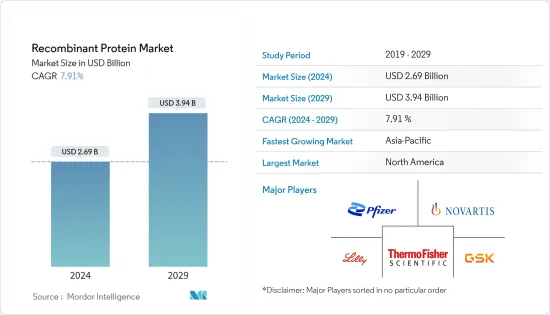

組換えタンパク質の市場規模は、2024年に26億9,000万米ドルと推定され、2029年までに39億4,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に7.91%のCAGRで成長します。

COVID-19のパンデミックは、組換えタンパク質市場の成長に影響を与えました。COVID-19の出現に伴い、それに対抗するための治療法やワクチン接種対策への需要が高まっています。多くの市場関係者や公的機関がCOVID-19治療のための研究開発活動に焦点を移し、組換えタンパク質が重要な役割を果たしました。これらの活動において重要な役割を果たします。たとえば、2022年5月にジャーナルJCLAに掲載された記事では、研究者や科学者がCOVID-19ワクチン開発のために組換えタンパク質をターゲットにしていると報告しました。このように、COVID-19は、組み換えタンパク質ベースの医薬品の需要の急増を引き起こしました。しかし、現在のシナリオでは、他の慢性疾患の高い有病率と他の感染症の存在、およびその治療における組換えタンパク質ベースの医薬品の有効性により、調査対象市場は大幅な成長を遂げると予想されます。予測期間にわたって。

調査対象市場の成長を推進している要因は、研究開発への支出の増加です。慢性疾患の蔓延。人口の高齢化。生物製剤やバイオシミラーへの傾向の高まり。そして高度な組換え製品の発売。

米国がん協会の2022年の統計によると、米国では2022年に新たにがんの症例が1,918,030件発生すると推定されています。このようにがんの負担が大きいため、治療には高度な治療法の必要性が生じており、組換えタンパク質は主にがんの治療に使用されているため、治療法やがん治療法の開発に伴い、がん負担の増加により組換えタンパク質の需要が高まり、それによって市場の成長が促進されると予想されます。

さらに、新しい組換えタンパク質治療薬のイントロダクションを目的とした研究開発への投資の増加も市場の成長に貢献しています。たとえば、2022年 5月、米国国立衛生研究所(NIH)からの最新情報では、米国NIHの自己免疫疾患の研究開発資金として2021年に約10億2,100万米ドルが投資されたと報告されました。米国、このような投資の増加は、組換えベースのタンパク質医薬品の開発につながり、調査対象市場の成長を促進します。

さらに、2021年9月には、ライフサイエンス調査向けの抗体、イムノアッセイキット、組換えタンパク質の製造と開発に従事する企業の1つであるAviva Systems Biologyが、ライフサイエンティスト向けの新しいプロテインオンデマンドのセミカスタム組換えタンパク質ポートフォリオを開始しました。基礎調査と前臨床研究を実施します。

したがって、研究開発への支出の増加、慢性疾患の有病率の増加、人口の高齢化、生物製剤およびバイオシミラーへの傾向の高まり、および高度な組換え製品の発売により、組換えタンパク質市場は、過去を上回る大幅な成長が見込まれています。予測期間。ただし、時間がかかり、高コストの生産プロセスと高コストは、予測期間中の市場の成長を妨げる可能性があります。

組換えタンパク質の市場動向

抗体セグメントは、予測期間中に大幅な成長を遂げると予想されます。

組換え抗体の産生手順には、抗体遺伝子ライブラリーをファージベクターにクローニングし、ファージを宿主細胞株に感染させることが含まれます。次に、宿主細胞は、その表面に組換え抗体を発現する娘ファージを生成します。遺伝子は発現系に挿入でき、望ましい特性を持つ抗体を選択するプロセスを経て、抗体を大量に生産できます。白血病症例の増加、調査、臨床研究などの要因が、予測期間中にこのセグメントの成長を促進すると予想されます。

糖尿病の症例の増加と抗体の使用の増加が、この分野の成長を推進しています。たとえば、2021年に国際糖尿病連盟(IDF)は、2021年に世界で5億3,700万人の糖尿病患者が報告され、この数は2045年までに7億8,300万人増加すると予想していると報告しました。糖尿病などの慢性疾患の増加が原因で、組換え抗体の需要が増加しています。

主要な市場企業による合併、買収、提携、新製品の発売も、この部門の成長を推進しています。たとえば、2021年2月、サノフィとGSKは、アジュバント添加組換えタンパク質COVID-19感染症ワクチン候補の第3相試験に最適な抗原用量を見つけるために、18歳以上の成人720人を対象とした新たな第2b相試験を開始しました。

同様に、2022年4月、Albumedix Ltd.は、Valneva Sとの既存の協力関係を拡大しました。これは、MHRAが最近Valneva社のアルブミン含有不活化COVID-19感染症ワクチン(VLA 2001)を承認したことに続くもので、Valneva社は2022年に欧州委員会と供給契約を締結しました。 2021年11月までに2年間で最大6,000万回分を提供する予定。さらに、ヴァルネバ氏は、2021年12月にバーレーン王国と100万回分の供給に関する事前購入契約を締結したと報告しました。 VLA 2001の重要な成分であるアルブメディクスレコンブミンは、ワクチンの製造と最終製剤の両方に使用されています。したがって、このような開発は、調査対象セグメントの成長を促進しています。

したがって、このセグメントの市場の成長は、糖尿病などの慢性疾患の増加と主要な市場企業の変化によって推進される可能性があります。

北米は、予測期間中に大幅な成長を遂げると予想されます。

北米は、ヘルスケアインフラといくつかの主要な市場企業の存在に加え、調査への支出の増加により、組換えタンパク質市場をリードすると予想されています。この地域全体で増加している慢性疾患は、組換えタンパク質がそのような疾患を治療するための実証済みの解決策の1つであるため、組換えタンパク質療法に対する大きな需要を生み出しています。

さらに、アルツハイマー病や認知症などのさまざまな神経変性疾患の治療に関する新しい調査も、研究対象市場の成長を推進しています。アルツハイマー病の研究者は多大な時間を要し、アミロイドと呼ばれるタンパク質にリソースが費やされてきました。多くのアルツハイマー調査コミュニティは、アミロイドを標的にすることが根本的な疾患を治療する鍵であると信じており、これによりアミロイドベースの治療に対する需要が高まると予想されています。たとえば、2022年 4月にジャーナルANCに掲載された論文では、プラーク関連タンパク質によって、これらの追加のタンパク質が重要であることが明らかになったと述べられています。これらは、アミロイド斑の発生を促進し、アルツハイマー病の潜在的なバイオマーカーまたは治療標的となる因子についての洞察を提供します。

国内での臨床試験の数が増加しているため、研究対象市場の需要が高まっています。たとえば、2022年にClinicaltrials.govは、2022年にバイオ医薬品に関連する米国で現在約15,316件の臨床試験が登録されていると報告しました。この国内で研究される臨床試験の数の増加は、国内の研究対象市場の成長を促進すると予想されます。

さらに、メキシコ人口における慢性疾患の有病率の上昇も市場の成長を促進すると予想されます。たとえば、IDFは2021年12月に発表し、メキシコでは推定1,400万人の成人が糖尿病を抱えて暮らしていると発表しました。このような糖尿病の有病率は、組換えタンパク質の需要を増加させると予想され、それによって予測期間中の市場の成長に貢献します。

したがって、調査への支出の増加、ヘルスケアインフラといくつかの主要な市場企業の存在、慢性疾患の高い罹患率により、北米地域の市場は予測期間中に大幅な成長が見込まれると予想されます。

組換えタンパク質業界の概要

組換えタンパク質市場は、世界的および地域的に事業を展開する少数の企業が存在するため、適度な競争が見られます。競合情勢には、Abbvie Inc.、Amgen Inc.、Bio-Rad Laboratories Inc.、Eli Lilly and Company、Merck KGaA、Novoなど、市場シェアを保持しよく知られている数社の国際企業と国内企業の分析が含まれています。 Nordisk AS、Sanofi SA、Thermo Fisher Scientific Inc.、Novartis AG、GlaxoSmithKline PLC、Novavax Inc.、GigaGen Inc.、およびPfizer Inc.

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 研究開発費の増加

- 増大する慢性疾患の負担

- 生物製剤およびバイオシミラーへの関心の高まり

- 組換え製品における技術の進歩

- 市場抑制要因

- 高価で時間のかかる製造プロセス

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 製品別

- ホルモン

- 成長因子

- 抗体

- 酵素

- その他の製品タイプ

- 用途別

- 調査応用

- 治療的使用

- バイオテクノロジー産業

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Abbvie Inc.

- Amgen Inc.

- Bio-Rad Laboratories Inc.

- Eli Lilly and Company

- Merck KGaA

- Novo Nordisk AS

- Sanofi SA

- Thermo Fisher Scientific Inc.

- Novartis AG

- GlaxoSmithKline PLC

- Novavax Inc.

- Pfizer Inc.

第7章 市場機会と将来の動向

The Recombinant Protein Market size is estimated at USD 2.69 billion in 2024, and is expected to reach USD 3.94 billion by 2029, growing at a CAGR of 7.91% during the forecast period (2024-2029).

The COVID-19 pandemic impacted the growth of the recombinant protein market. With the emergence of COVID-19, there has been an increased demand for therapeutic and vaccination measures to combat it.Many market players and public organizations shifted their focus to research and development activities for the treatment of COVID-19, and recombinant proteins played a vital role in these activities. For instance, an article published in the journal JCLA in May 2022 reported that researchers and scientists targeted recombinant proteins for COVID-19 vaccine development. Thus, COVID-19 sparked a surge in demand for recombinant protein-based medicines. However, in the current scenario, it is anticipated that, with the high prevalence of other chronic diseases and the presence of other infectious diseases, and the efficacy of recombinant protein-based medicine in its treatment, the studied market is expected to witness significant growth over the forecast period.

The factors that are driving the growth of the studied market are the increasing expenditure on research and development; the growing prevalence of chronic diseases; the aging population; the rising inclination towards biologics and biosimilars; and the launch of advanced recombinant products.

According to the American Cancer Society's 2022 statistics, in the United States, there will be an estimated 1,918,030 new cancer cases in 2022. Such a high burden of cancer creates the need for advanced therapeutics for the treatment, and since recombinant proteins are largely used in therapeutics and the development of cancer therapies, an increase in the cancer burden is expected to drive the demand for recombinant proteins, thereby driving the market's growth.

Additionally, increasing investments in research and development aimed at the introduction of new recombinant protein therapeutics also contribute to the growth of the market. For instance, in May 2022, an update from the National Institute of Health (NIH) of the United States reported that about USD 1,021 million had been invested in the year 2021 for the research and development funding for autoimmune diseases in the NIH of the United States, and it is further expected to increase to USD 1,061 million in 2022. Thus, such an increase in investment is leading to the development of recombinant-based protein medicines and thus fueling the growth of the studied market.

Furthermore, in September 2021, Aviva Systems Biology, one of the companies engaged in manufacturing and developing antibodies, immunoassay kits, and recombinant proteins for life science research, launched its new protein-on-demand, semi-custom recombinant protein portfolio for life scientists conducting basic research and preclinical studies.

Thus, due to the increasing expenditure on research and development, the growing prevalence of chronic diseases, the aging population, the rising inclination towards biologics and biosimilars, and the launch of advanced recombinant products The recombinant protein market is expected to project significant growth over the forecast period. However, the time-consuming and high-cost production processes and high costs may hamper the market's growth over the forecast period.

Recombinant Proteins Market Trends

Antibody Segment is Expected to Witness a Significant Growth Over the Forecast Period.

The recombinant antibody production procedure involves cloning antibody gene libraries into phage vectors and allowing the phages to infect a host cell line. The host cells then produce daughter phages expressing the recombinant antibodies on their surfaces. The genes can be inserted into an expression system, and the antibodies can be produced in large quantities after a process of selection for antibodies with the desired characteristics. Factors such as increasing cases of leukemia, research, and clinical studies are expected to drive the growth of this segment over the forecast period.

The rising cases of diabetes and the increasing use of antibodies are driving the growth of this segment. For instance, in 2021, the International Diabetes Federation (IDF) reported that globally in the year 2021, 537 million cases of diabetes were reported and that this number is expected to increase by 783 million by 2045. So, the growth of the segment is being driven by the rise of chronic diseases like diabetes, which is increasing the demand for recombinant antibodies.

The mergers, acquisitions, partnerships, and new product launches by key market players are also driving the growth of this segment. For example, in February 2021, Sanofi and GSK started a new phase 2b study with 720 adults over the age of 18 to find the best antigen dose for phase 3 testing of the adjuvanted recombinant protein COVID-19 vaccine candidate.

Similarly, in April 2022, Albumedix Ltd. expanded its existing collaboration with Valneva S. This follows the MHRA's recent approval of Valneva's inactivated COVID-19 vaccine containing albumin (VLA 2001), for which Valneva entered into a supply agreement with the European Commission in November 2021 to provide up to 60 million doses over two years. In addition, Valneva reported an advance purchase agreement with the Kingdom of Bahrain in December 2021 for the supply of one million doses. A crucial ingredient in VLA 2001, Albumedix Recombumin, is employed in both the vaccine's manufacture and final formulation. Thus, such developments are fueling the growth of the studied segment.

So, the growth of the market in this segment is likely to be driven by the rise of chronic diseases like diabetes and changes among the major market players.

North America is Expected to Witness a Significant Growth Over the Forecast Period.

North America is expected to lead the recombinant protein market, owing to the increasing expenditure on research, coupled with the presence of healthcare infrastructure and several major market players. The chronic diseases that are on the rise across the region are creating a huge demand for recombinant protein therapies, as recombinant proteins are among the proven solutions for treating such diseases.

Furthermore, novel research for the treatment of various neurodegenerative diseases such as Alzheimer's disease and dementia is also propelling the growth of the studied market. Researchers in Alzheimer's disease require a large amount of time and resources have gone toward a protein called amyloid. Many Alzheimer's research community believes targeting amyloid is the key to treating the underlying disease, which is expected to rise the demand for amyloid-based therapies. For instance, an article published in the journal ANC in April 2022, stated that plaque-associated proteins have revealed these additional proteins are important; they offer insight into the factors that drive amyloid plaque development and are potential biomarkers or therapeutic targets for Alzheimer's disease.

The increasing number of clinical trial studies in the country is driving the demand for the studied market. For instance, in 2022, Clinicaltrials.gov reported that around 15,316 clinical trials are currently registered in the United States involving biopharmaceuticals in the year 2022. This increasing number of clinical trials studied in the country is anticipated to drive the studied market growth in the country.

Additionally, the rising prevalence of chronic diseases among the Mexican population is also expected to drive the growth of the market. For instance, IDF published in December 2021, an estimated 14 million adults in Mexico were living with diabetes. Such a prevalence of diabetes is expected to rise the demand for recombinant proteins, thereby contributing to the growth of the market over the forecast period.

Thus, owing to the increasing expenditure on research, coupled with the presence of healthcare infrastructure and several major market players and the high prevalence of chronic diseases the market in the North American region is expected to project significant growth over the forecast period.

Recombinant Proteins Industry Overview

The recombinant protein market is moderately competitive due to the presence of a few companies operating globally and regionally. The competitive landscape includes an analysis of a few international as well as local companies that hold market shares and are well known, such as Abbvie Inc., Amgen Inc., Bio-Rad Laboratories Inc., Eli Lilly and Company, Merck KGaA, Novo Nordisk AS, Sanofi SA, Thermo Fisher Scientific Inc., Novartis AG, GlaxoSmithKline PLC, Novavax Inc., GigaGen Inc., and Pfizer Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Expenditure on Research and Development

- 4.2.2 Growing Burden of Chronic Diseases

- 4.2.3 Rising Inclination toward Biologics and Biosimilars

- 4.2.4 Technological Advancements in Recombinant Products

- 4.3 Market Restraints

- 4.3.1 Expensive and Time-consuming Production Process

- 4.4 Porters' Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Product

- 5.1.1 Hormone

- 5.1.2 Growth Factor

- 5.1.3 Antibody

- 5.1.4 Enzyme

- 5.1.5 Other Types of Products

- 5.2 By Application

- 5.2.1 Research Application

- 5.2.2 Therapeutic Use

- 5.2.3 Biotechnology Industry

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abbvie Inc.

- 6.1.2 Amgen Inc.

- 6.1.3 Bio-Rad Laboratories Inc.

- 6.1.4 Eli Lilly and Company

- 6.1.5 Merck KGaA

- 6.1.6 Novo Nordisk AS

- 6.1.7 Sanofi SA

- 6.1.8 Thermo Fisher Scientific Inc.

- 6.1.9 Novartis AG

- 6.1.10 GlaxoSmithKline PLC

- 6.1.11 Novavax Inc.

- 6.1.12 Pfizer Inc.