|

市場調査レポート

商品コード

1437950

不眠症治療:市場シェア分析、業界動向と統計、成長予測(2024~2029年)Insomnia Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 不眠症治療:市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

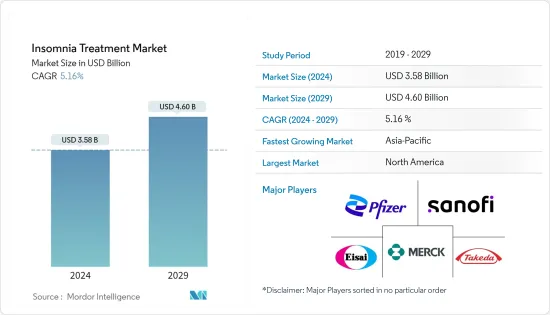

不眠症治療市場規模は2024年に35億8,000万米ドルと推定され、2029年までに46億米ドルに達すると予測されており、予測期間(2024年から2029年)中に5.16%のCAGRで成長します。

主なハイライト

- COVID-19感染症のパンデミックは人々の生活に前例のない変化をもたらしました。多くの人にとって、健康、社会的孤立、雇用、財政、仕事と家族の義務のバランスなどについて、重大なストレス、不安、懸念を引き起こしています。このような重要なライフイベントは睡眠を妨げ、市場の成長に影響を与える可能性があります。新型コロナウイルス感染症(COVID-19)のパンデミックは睡眠に影響を与えました。

- 米国睡眠医学会(AASM)の2020年睡眠優先順位調査によると、成人の約3分の1(33%)が睡眠の質の変化に気づき、30%が入眠能力の変化に気づき、29%が睡眠の質の変化に気づきました。夜の睡眠時間の違いです。さらに、女性は男性よりもCOVID-19感染症のパンデミックが就寝時間に影響を与えたと報告する可能性が高かった(31%対25%)。人々の睡眠に対するこのような影響により、パンデミック中に不眠症治療の需要が高まりました。しかし、パンデミック後も不眠症治療のニーズは変わらないと見込まれており、今後5年間の市場成長に貢献するとみられます。

- また、不眠症の有病率の増加、ストレスレベルの上昇、この症状のさまざまな治療法に対する意識の高まりも、市場を推進すると予想される要因の一部です。たとえば、2021年 7月にSpringerに掲載された記事では、不眠症の全体的な有病率は12.13%、軽度の不眠症は31.97%であると述べられています。同情報筋は、ほとんどの不眠症は男性に比べて女性で増加していると指摘しました。このような不眠症の蔓延は市場の成長を促進すると予想されます。

- 世界人口のストレスレベルの上昇も、市場成長の主な原動力です。 2021年12月に発表された安全衛生執行部の報告書によると、2020年から2021年にかけて82万2,000人を超える労働者が仕事関連のストレス、うつ病、または不安に苦しんでいた。人口のこのような高いストレスレベルも市場の成長を促進すると予想されます。不眠症が単独で発生することはほとんどなく、他の病気と関連していることがよくあります。

- さらに、不眠症治療のための革新的な製品開発も市場の成長に貢献すると期待されています。たとえば、2022年 6月、Pear Therapeuticsは、慢性不眠症を治療するためのFDA認可のデジタル治療法の1つであるSomrystによる治療を示す、分散型トレイルからの現実世界の暫定追跡データを報告しました。このデバイスは、不眠症、不安、うつ病の重症度の症状を大幅に軽減しました。

- したがって、不眠症の蔓延、治療に対する意識の高まり、製品発売の増加などの要因が、予測期間中の市場の成長に寄与すると予想されます。ただし、不眠症の深刻さと患者の治療不履行についての誤解は、予測期間中の市場の成長を制限する可能性のあるいくつかの要因です。

不眠症治療市場の動向

オレキシンアンタゴニストセグメントは、予測期間中に市場でかなりのシェアを保持すると予想されます

- オレキシンアンタゴニストセグメントは、有効性の低下と複数の患者に対する多くの治療選択肢の使用を制限する有害な副作用のため、予測期間中に研究セグメントの成長を支配すると予想されます。オレキシン受容体アンタゴニストには、スボレキサント、レンボレキサント、ダリドレキサントなどがあります。これらの薬剤は、両方の受容体、つまりOX1RとOX2Rをブロックする強力な二重オレキシン受容体アンタゴニストです。覚醒を促進する神経ペプチドであるオレキシンAおよびBを阻害することで睡眠を刺激します。

- スボレキサント(MK-4305、Merck)は、ORA(オレキシン受容体拮抗薬)として知られる不眠症治療用の新しいクラスの薬剤の最初の1つです。この錠剤は、覚醒システムの覚醒を促進するオレキシンニューロンを阻害することにより、不眠から睡眠への自然な移行をサポートします。スボレキサントは、睡眠の開始と睡眠の維持を促進します。この独特の代替案は、有利な許容性と制限された副作用プロファイルを備えています。

- また、製品承認と製品開発活動の増加は、予測期間中の調査対象セグメントの成長に貢献すると予想されます。たとえば、2022年10月、イドルシア・ファーマシューティカルズ・ジャパンは、無作為化された成人および高齢患者490名(30.1%、65歳)を対象に、イドルシアのデュアルオレキシン受容体拮抗薬であるダリドレキサントの25mgおよび50mgの用量を調査した日本の第3相試験の肯定的なトップライン結果を発表しました。不眠症障害を抱えています。

- 同様に、2021年2月、エーザイ株式会社のカナダ子会社であるエーザイリミテッドは、新しい非鎮静性処方薬デイビゴ(レンボレキサント)についてカナダの承認を取得しました。 DAYVIGOは、5 mgと10 mgの用量の両方で、入眠および/または睡眠維持の困難を特徴とする不眠症の治療に使用されます。

- オレキシンクラスの薬剤に関連する明らかな利点、製品承認の増加、不眠症または入眠困難の有病率の上昇により、不眠症治療市場は予測期間中に着実に成長すると予想されます。

予測期間中、北米が不眠症治療市場を独占すると予想される

- 北米は不眠症治療市場で大きなシェアを占めると予想されています。米国とカナダでの睡眠障害治療のニーズの高まりと、睡眠障害の有病率の増加が、予測期間中に市場を牽引すると予想されます。

- たとえば、2022年6月にカナダ政府が発表したデータでは、カナダ人の3分の1が十分な睡眠をとれておらず、数千人が不眠症やその他の睡眠障害に苦しんでいることが述べられています。この地域の人口における睡眠障害のこのような発生率は、市場の成長を促進すると予想されます。

- また、不眠症治療への資金提供という形での政府支援の増加も市場の成長に寄与すると予想されます。たとえば、2022年 6月に保健大臣は、睡眠の健康と不眠症に関する調査を支援するために286万米ドル(380万カナダドル)の資金提供を発表しました。カナダ政府は、Esai LimitedおよびMitacsと提携し、カナダ保健調査(CIHR)を通じてこの取り組みを支援しました。北米でのこのような資金調達は、予測期間中の市場の成長に貢献すると予想されます。

- さらに、新薬のコラボレーションや研究開発、製品の承認など、主要な市場プレーヤーの活動の存在により、調査対象の市場の成長が促進されると予想されます。たとえば、2021年1月に、Minerva Neurosciences Inc.とRoyalty Pharma PLCは、Royalty Pharmaがミネルバのセルトレキサントにおけるロイヤルティ権を取得する契約を締結しました。選択的オレキシン2受容体拮抗薬であるセルトレキサントは、現在、不眠症状を伴う大うつ病性障害(MDD)の治療薬として第3相開発中です。

- したがって、睡眠障害の有病率の増加、主要な市場プレーヤーの存在、および不眠症治療に対する政府資金の増加と相まって、頻繁な製品発売が、この地域の予測期間中の市場の成長に寄与すると予想されます。

不眠症治療業界の概要

不眠症治療市場は複数のメーカーが存在するため、本質的に細分化されています。市場の主要企業は、Merck &Co.、Ebb Therapeutics、Paratek Pharmaceuticals Inc.、Pfizer Inc.、Sanofi SA、Electromedical Products International Inc.、武田薬品工業株式会社、Cereve Inc.、およびInnovative Neurological Devicesです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 個人の非常に活動的なライフスタイルによるストレスの増加

- 特定のOTC薬および処方薬による副作用

- 睡眠前にメディアデバイスを頻繁に使用する

- 市場抑制要因

- 不眠症の深刻さに関する誤解

- 不眠症治療薬の特徴的な副作用による患者の不履行

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手の交渉力

- 供給企業の交渉力

- 代替製品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- 治療タイプ別

- 薬剤

- ベンゾジアゼピン系

- 非ベンゾジアゼピン系薬剤

- オレキシンアンタゴニスト

- その他の薬物

- デバイス

- 薬剤

- 流通チャネル別

- 病院薬局

- 小売薬局

- その他の流通チャネル

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東とアフリカ

- GCC

- 南アフリカ

- その他中東およびアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Merck &Co.

- Ebb Therapeutics

- Paratek Pharmaceuticals Inc.

- Pfizer Inc.

- Sanofi SA

- Electromedical Products International Inc.

- Takeda Pharmaceutical Company Ltd

- Cereve Inc.

- Innovative Neurological Devices

- Eisai Co. Ltd

- Meda Consumer Healthcare

- Purdue Pharma LP

- Pernix Therapeutics

第7章 市場機会と将来の動向

The Insomnia Treatment Market size is estimated at USD 3.58 billion in 2024, and is expected to reach USD 4.60 billion by 2029, growing at a CAGR of 5.16% during the forecast period (2024-2029).

Key Highlights

- The COVID-19 pandemic brought about unprecedented changes in people's lives. For many, it has caused significant stress, anxiety, and concerns over health, social isolation, employment, finances, and balancing work and family obligations. Such an important life event will likely disrupt sleep and impact market growth. The COVID-19 pandemic impacted sleep.

- According to the American Academy of Sleep Medicine's (AASM) Sleep Prioritization Survey 2020, about a third of adults (33%) noticed a change in their sleep quality, 30% noticed a change in their ability to fall asleep, and 29% noticed a difference in their nightly amount of sleep. Furthermore, females were more likely than males to report that the COVID-19 pandemic impacted their bedtimes (31% vs. 25%). Such an impact on people's sleep led to the rising demand for insomnia treatment during the pandemic. However, the need for insomnia treatment, even after the pandemic, is expected to remain the same, contributing to the market's growth over the coming five years.

- Also, the increasing prevalence of insomnia, rising stress levels, and increasing awareness about various treatment options for this condition are some of the factors expected to propel the market. For instance, an article published in Springer in July 2021 mentioned that the overall prevalence of insomnia was 12.13%, and mild insomnia was 31.97%. The same source noted that most insomnia increased in females compared to males. Such a prevalence of insomnia is expected to drive the market's growth.

- The rising stress levels among the global population are another primary driver for the market's growth. According to the Health and Safety Executive report published in December 2021, over 822,000 workers suffered from work-related stress, depression, or anxiety in 2020-2021. Such high-stress levels among the population are also expected to drive the market's growth. Insomnia rarely occurs on its own and is frequently associated with other illnesses.

- Furthermore, innovative product developments for the treatment of insomnia are also expected to contribute to the market's growth. For instance, in June 2022, Pear Therapeutics reported interim follow-up real-world data from a decentralized trail that showed treatment with Somryst, one of the FDA-authorised digital therapeutics for treating chronic insomnia. This device significantly reduced symptoms of insomnia, anxiety, and depression severity.

- Thus, the factors such as the prevalence of insomnia, rising awareness for treatment, and increasing product launches are expected to contribute to the market's growth over the forecast period. However, misconceptions about the seriousness of insomnia and patients' non-adherence to the treatment are some factors that may limit market growth during the forecast period.

Insomnia Treatment Market Trends

Orexin Antagonist Segment is Expected to Hold a Significant Share in the Market Over the Forecast Period

- The Orexin antagonist segment is expected to dominate the growth of the studied segment during the forecast period due to the reduced efficacy and harmful side effects that constrain the use of many treatment options for several patients. Some of the orexin receptor antagonists include suvorexant, Lemborexant, and Daridorexant. These drugs are potent dual orexin receptor antagonist that blocks both receptors, i.e., OX1R and OX2R. It stimulates sleep by inhibiting orexin-A and B, neuropeptides that promote wakefulness.

- Suvorexant (MK-4305, Merck) is one of the first of a new class of drugs for treating insomnia known as ORAs (orexin receptor antagonists). The tablets support the natural transition from sleeplessness to sleep by inhibiting the arousal system's wakefulness-promoting orexin neurons. Suvorexant advances sleep onset, as well as sleep maintenance. This distinctive alternative has advantageous permissibility and a restricted side-effect profile.

- Also, the increasing product approvals and product development activities are expected to contribute to the growth of the studied segment over the forecast period. For instance, in October 2022, Idorsia Pharmaceuticals Japan announced positive top-line results of the Japanese Phase 3 study investigating 25 and 50 mg doses of Idorsia's dual orexin receptor antagonist, daridorexant, in 490 randomized adult and elderly patients (30.1% 65 years) with insomnia disorder.

- Similarly, in February 2021, Eisai Limited, the Canadian subsidiary of Eisai Inc., received Canadian authorization for its new non-sedative prescription medication, DAYVIGO (lemborexant). In both 5 mg and 10 mg dosages, DAYVIGO is taken for the treatment of insomnia, characterized by difficulties with sleep onset and/or sleep maintenance.

- Due to the apparent benefits associated with the orexin class of drugs, increasing product approvals, and the rising prevalence of insomnia or difficulty falling asleep, the insomnia treatment market is expected to grow steadily during the forecast period.

North America is Expected to Dominate the Insomnia Treatment Market Over the Forecast Period

- North America is expected to hold a significant share of the insomnia treatment market. The growing need for sleep disorder treatment in the United States and Canada, coupled with the increasing prevalence of sleep disorders, is expected to drive the market over the forecast period.

- For instance, data published by the Government of Canada in June 2022 mentioned that one-third of Canadians are not getting enough sleep, with thousands of people suffering from insomnia and other sleep disorders. Such incidence of sleep disorders among the population in this region is expected to drive the market's growth.

- Also, the increasing government support in the form of funding for insomnia treatment is expected to contribute to the market's growth. For instance, in June 2022, the Minister of Health released funding of USD 2.86 million (CAD 3.8 million) to support research on sleep health and insomnia. The government of Canada supported this initiative through the Canadian Institutes of Health Research (CIHR) in partnership with Esai Limited and Mitacs. Such funding in North America is expected to contribute to the market's growth during the forecast period.

- Moreover, the presence of key market players' activities, such as collaborations and the R&D of new drugs and product approvals, is expected to boost the growth of the market studied. For instance, in January 2021, Minerva Neurosciences Inc. and Royalty Pharma PLC entered an agreement through which Royalty Pharma will acquire Minerva's royalty interest in seltorexant. Seltorexant, a selective orexin two receptor antagonist, is currently in Phase 3 development for treating major depressive disorder (MDD) with insomnia symptoms.

- Thus, the growing prevalence of sleep disorders, the presence of major market players, and frequent product launches coupled with increasing government funding for insomnia treatments are expected to contribute to the market's growth over the forecast period in this region.

Insomnia Treatment Industry Overview

The insomnia treatment market is fragmented in nature, owing to the presence of multiple manufacturers. The major players in the market are Merck & Co., Ebb Therapeutics, Paratek Pharmaceuticals Inc., Pfizer Inc., Sanofi SA, Electromedical Products International Inc., Takeda Pharmaceutical Company Ltd, Cereve Inc., and Innovative Neurological Devices.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Stress Due to Highly Active Lifestyles of Individuals

- 4.2.2 Side Effects Due to Certain OTC and Prescription Medication

- 4.2.3 High Usage of Media Devices Before Sleep

- 4.3 Market Restraints

- 4.3.1 Misconceptions about the Seriousness of Insomnia

- 4.3.2 Patient Non-adherence due to Characteristic Side Effects of Insomnia Drugs

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Treatment Type

- 5.1.1 By Drug

- 5.1.1.1 Benzodiazepines

- 5.1.1.2 Nonbenzodiazepines

- 5.1.1.3 Orexin Antagonist

- 5.1.1.4 Other Drugs

- 5.1.2 Devices

- 5.1.1 By Drug

- 5.2 By Distribution Channel

- 5.2.1 Hospital Pharmacies

- 5.2.2 Retail Pharmacies

- 5.2.3 Other Distribution Channels

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Merck & Co.

- 6.1.2 Ebb Therapeutics

- 6.1.3 Paratek Pharmaceuticals Inc.

- 6.1.4 Pfizer Inc.

- 6.1.5 Sanofi SA

- 6.1.6 Electromedical Products International Inc.

- 6.1.7 Takeda Pharmaceutical Company Ltd

- 6.1.8 Cereve Inc.

- 6.1.9 Innovative Neurological Devices

- 6.1.10 Eisai Co. Ltd

- 6.1.11 Meda Consumer Healthcare

- 6.1.12 Purdue Pharma LP

- 6.1.13 Pernix Therapeutics