|

市場調査レポート

商品コード

1433520

IoTチップ:世界市場シェア分析、産業動向と統計、成長予測(2024年~2029年)Global IoT Chip - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| IoTチップ:世界市場シェア分析、産業動向と統計、成長予測(2024年~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

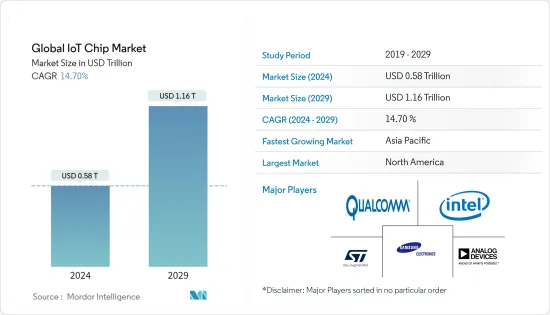

世界のIoTチップの市場規模は、2024年に5,800億米ドルと推定され、2029年までに1兆1,600億米ドルに達すると予測されており、予測期間(2024年~2029年)中に14.70%のCAGRで成長する見込みです。

需要側と供給側の要因により、パンデミック中に特定のセクターでIoT接続数の増加が鈍化しました。企業の廃業や支出の縮小により、一部のIoT契約はキャンセルまたは延期されました。ヘルスケア、コンシューマーエレクトロニクス、産業、自動車、BFSI、小売などのさまざまなエンドユーザー分野における自動化への需要の高まりとIoTデバイスのアプリケーションの拡大により、IoTデバイスの導入がさらに促進されています。

主なハイライト

- この成長は主に、さまざまなネットワークプロトコルの開発と相まって、さまざまなデバイスやアプリケーションにおける接続能力の統合に起因しており、これらのプロトコルが複数のエンドユーザー業界全体でIoTチップ市場の成長を大きく推進しています。

- 2022年3月、マサチューセッツ工科大学(MIT)で働く2人のインド人研究者は、モノのインターネット(IoT)デバイスに対するサイドチャネル攻撃(SCA)を防ぐように設計された低電力セキュリティチップを開発しました。 SCAは脆弱性を利用して、プログラムやソフトウェアを直接攻撃するのではなく、システムハードウェアの動作の間接的な影響から情報を収集できるようにします。

- IoTデバイスの数の急速な増加に伴い、これらのIoTデバイスを構築するためのチップ要件も予測期間中に増加すると予想されます。これに伴い、エネルギー消費量の削減とチップの小型化がメーカーの優先事項となります。

- 5Gの導入の増加により、モノのインターネット(IoT)デバイスに迅速かつ効率的な接続が提供されます。 5G技術の展開への投資は、予測期間中およびそれ以降も市場の成長を促進すると予想されます。 5Gテクノロジーの統合は、次世代のモバイルインターネット接続とみなされており、現在のテクノロジーよりも高速で信頼性の高い接続を提供すると期待されています。したがって、急成長するIoT分野とそれをサポートするチップメーカーにより、予測期間中にIoTチップの需要が増加すると予想されます。

- ソフトウェアの脆弱性やサイバー攻撃などのセキュリティ上の懸念の高まりにより、多くの顧客がIoTデバイスの使用を思いとどまる可能性があります。モノのインターネットにおけるこのようなセキュリティ上の懸念は、ヘルスケア、金融、製造、物流、小売、およびすでにIoTシステムの導入を開始しているその他の業界の組織にとって特に重要です。

- COVID-19の世界的流行により、世界中で深刻なサプライチェーン不足が発生し、市場は大きな影響を受けました。さらに、世界中の政府が人の移動に課した制限も生産に影響を与えました。しかし、世界がパンデミックから回復するにつれて、より自動化された高度なプロセスの必要性が成功の重要な側面となっています。そのため、将来的にはさらに多くのIoT対応デバイスの市場が拡大すると予想されており、それによって世界中でIoTチップに対する強い需要が生み出されます。

IoTチップ市場動向

産業分野は大幅な成長が見込まれる

- インダストリー4.0とIoTは、開発、生産、物流チェーンにおける新しい技術的アプローチの主流となっています。インダストリアル4.0の採用の拡大により、機械間接続や組み込みセンサーの増加、現場や現場での工場の効率化に対するニーズの高まりにより、製造業におけるIoT需要が最大限に保たれています。

- Economic Timesの調査によると、2022年7月にはインドでセルラーIoTモジュール・チップセットの出荷が増加し、Qualcommが42%のシェアで市場をリードしました。同社は、小売、産業、スマートシティなどの業界向けのプレミアム4Gおよび5Gソリューションをターゲットとして、IoTチップセットのポートフォリオを拡大しています。

- ほとんどのメーカーは、予知保全と高度なデータ分析を活用するためにIoTデバイスを導入しています。これにより、生産性と可用性が向上し、ビジネス製品の価値が高まります。たとえば、GEは産業分析によるIoTの機会を模索しています。さらに、Apotexは製造プロセスをアップグレードして手動プロセスを自動化しました。これには、RFID、仕分け、プロセスフロー追跡の導入による一貫したバッチ生産の確保が含まれます。このため、同社は製造業務をリアルタイムで把握できるようになりました。

- さらに、産業用 IoTの動向は、米国のSmart Manufacturing Leadership Coalition(SMLC)などのスマートファクトリーイニシアチブによって促進されています。これにより、収集、処理、意思決定の形成が必要となる大量の機械およびセンサーのデータにより、製造インテリジェンスの広範な導入が促進され、促進されます。

- 2022年6月、外務省は欧州のモノのインターネット(IoT)ソリューション市場が加速していると発表しました。ドイツ、英国、オランダがIoT導入で欧州をリードしており、東欧と北欧諸国もそれに続いています。製造業、家庭、ヘルスケア、金融部門が同氏のIoT導入の最前線にあるが、小売業や農業も目覚ましい成長を見せています。複数の分野におけるこのような進歩により、欧州全体のIoTチップ市場が活用されることになります。

- eLTEやNB-IoTチップなどの無線チップの製造端末への導入は、長年にわたり注目を集めています。たとえば、Huaweiは業界パートナーと協力して、従来の製造業で機器データのアップロードやコマンドの受信に使用されるスマート端末を製造しました。製造端末にeLTEまたはNB-IoTチップを追加し、端末で生成されたデータをeLTEまたはNB-IoTネットワーク経由で送信することで、製造データの収集やコマンドの発行が可能になります。

アジア太平洋は大幅な成長が見込まれる

- アジア太平洋はIoTへの支出の大きなシェアを占めており、シンガポールと韓国がIoTチップを採用する主要市場となっています。経済協力開発機構によると、韓国は生息地ごとのインターネット接続数が最も多い最初の著名な市場です。

- 2022年7月、KIOXIA CorporationとWestern Digital Corporationは、四日市工場の合弁事業Fab7製造施設が日本政府から最大929億円の補助金の承認を取得したと発表しました。この補助金は、最先端の半導体製造施設への企業投資を促進し、日本における半導体の安定生産を確保することを目的とした政府の特別プログラムに基づいて交付されるものです。この地域でのこうした協力は、IoTチップ市場の成長に役立つと思われます。

- IoTのインフラストラクチャには、スマートシティにおけるIoTチップやICの需要の高まりや、コネクテッド自動車やスマート交通システムなどの分野での家庭内オートメーションの需要の高まりにより、オートメーションと交通の新たな段階を可能にする、より優れた無線接続ソリューションに対する需要が含まれています。

- さらに、アジアの政府は長期的な開発プロジェクトにIoTを深く統合しています。たとえば、中国の中央政府は、スマートシティプロジェクトを試験的に実施するために200以上の都市を選択しました。都市には北京、上海、広州、杭州が含まれます。さらに、100都市をスマートシティに変えるというインドのビジョンでは、スマートホームや自動車分野を通じたエレクトロニクスの推進が期待されています。

- 2022年5月、Cyientはインドハイデラバード工科大学(IITH)およびIITH内に設立された新興企業WiSig Networksと提携し、インド初の設計および設計されたチップであるKoala NB-IoT SoC(狭帯域IoT SoC)を発売しました。両者の間で署名された覚書(MOU)は、インド世界にサービスを提供し、世界的なエレクトロニクス製造と設計の拠点への発展をさらに促進するための活気に満ちた半導体設計とイノベーションエコシステムを構築するというMEITY(インド電子情報技術省)の目標と一致しています。

- この地域は、製造業などの分野でコネクテッドデバイスの使用が増加しているため、IoT支出の顕著なプロバイダーとなることが期待されています。 5Gの採用の増加により、IoTサービスが増加し、今後数年間の市場の成長が促進されます。

IoTチップ業界の概要

世界のモノのインターネット(IoT)チップ市場は、かなりの数の地域プレーヤーが存在し、適度に競争しています。両社は、市場シェアと収益性を高めるために、戦略的な共同イニシアチブと買収を活用しています。

- 2021年6月 - RAIN RFIDプロバイダーおよびモノのインターネットプロバイダーであるImpinj Inc.は、IoTデバイスメーカーが小売、サプライチェーン、とりわけ、物流、コンシューマーエレクトロニクスなどの市場におけるアイテムの接続に対する需要の高まりに対応できるようにする3つの新しいRAIN RFIDリーダーチップを発表しました。

- 2021年6月 - Qualcommは、物流、倉庫保管、スマートカメラ、ビデオコラボレーション、小売などのアプリケーションを対象とした7つの新しいIoTチップセットを発売しました。同社はまた、これらの新しいIoTソリューションは、幅広い接続ソリューションとスマートデバイスに重要な機能を提供し、寿命の長いハードウェアとソフトウェアのオプションを提供し、最低8年間の長期サポートを実現すると述べました。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度 - ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 技術スナップショット

- COVID-19の業界への影響評価

第5章 市場力学

- 市場促進要因

- コネクテッドデバイスとウェアラブルデバイスの需要増加

- インダストリー4.0動向の高まりによる先端技術の採用

- 市場抑制要因

- IoTデバイスの普及を妨げるデータのセキュリティとプライバシーに関する問題

- 異なるプラットフォーム間での通信プロトコルの標準化の欠如

第6章 市場セグメンテーション

- 製品別

- プロセッサー

- センサー

- コネクティビティIC

- メモリーデバイス

- ロジック・デバイス

- その他の製品

- エンドユーザー別

- ヘルスケア

- コンシューマーエレクトロニクス

- 産業用

- 自動車

- BFSI

- 小売

- ビルディングオートメーション

- その他のエンドユーザー

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Qualcomm Technologies Inc.

- Intel Corporation

- Texas Instruments Incorporated

- NXP Semiconductors NV

- Cypress Semiconductor Corporation

- Mediatek Inc.

- Microchip Technology Inc.

- Samsung Electronics Co. Ltd

- Silicon Laboratories Inc.

- Invensense Inc.

- STMicroelectronics NV

- Nordic Semiconductor ASA

- Analog Devices Inc.

第8章 投資分析

第9章 市場の将来

The Global IoT Chip Market size is estimated at USD 0.58 trillion in 2024, and is expected to reach USD 1.16 trillion by 2029, growing at a CAGR of 14.70% during the forecast period (2024-2029).

Due to demand-side and supply-side factors, the growth in the number of IoT connections slowed down in specific sectors during the pandemic. Some IoT contracts were canceled or postponed due to firms going out of business or scaling back their spending. The rising demand for automation and the growing application of IoT devices across various end-user verticals, such as healthcare, consumer electronics, industrial, automotive, BFSI, and retail, are further driving the adoption of IoT devices.

Key Highlights

- The growth is primarily attributed to the integration of connectivity competence in a wide range of devices and applications, coupled with the development of different networking protocols that have appreciably driven the growth of the IoT chip market across multiple end-user industries.

- In March 2022, two Indian researchers working at the Massachusetts Institute of Technology (MIT) built a low-power security chip designed to prevent side-channel attacks (SCA) against Internet of Things (IoT) devices. SCA uses vulnerabilities to allow information gleaned from the indirect effects of the behavior of system hardware rather than directly attacking programs and software.

- With the rapid increase in the number of IoT devices, the chip requirement for building these IoT devices is also expected to rise over the forecast period. Along with this, reducing energy consumption combined with the miniaturization of chips will be the priority of manufacturers.

- The increased deployment of 5G provides quick and efficient connectivity for Internet-of-Things (IoT) devices. Investments in the deployment of 5G technology are expected to drive market growth during the forecast period and beyond. The integration of 5G technology is seen as the next generation of mobile internet connectivity and is expected to offer faster and more reliable connections than current technologies. Thus, the booming IoT space and the supporting chip makers are expected to increase demand for IoT chips during the forecast period.

- Rising security concerns, such as software vulnerabilities and cyberattacks, may discourage many customers from using IoT devices. Such security concerns in the Internet of Things are particularly essential to organizations in healthcare, finance, manufacturing, logistics, retail, and other industries that have already started adopting IoT systems.

- With the COVID-19 outbreak worldwide, the market was significantly affected as severe supply chain shortages occurred across the globe. Moreover, the restriction imposed by governments across the globe on the movement of people also impacted production. However, as the world recovers from the pandemic, the need for more automated and advanced processes has become a key aspect of success. As such, the market for more IoT-enabled devices is anticipated to rise in the future, thereby creating strong demand for IoT chips across the globe.

IoT Chip Market Trends

Industrial Segment is Expected to Witness Significant Growth

- Industry 4.0 and the IoT have become mainstream for new technological approaches in development, production, and logistics chains. The growing adoption of industrial 4.0 has kept IoT demand in manufacturing at maximum through increasing machine-to-machine connections and embedded sensors and the increasing need for factory efficiency on the floor and on the field.

- In July 2022, according to Economic Times's survey, cellular IoT module chipset shipments grew in India, and Qualcomm led the market with a 42% share. The company has been broadening its IoT chipset portfolio, targeting premium 4G and 5G solutions for verticals such as retail, industrial, smart cities, and more.

- Most manufacturers implement IoT devices to leverage predictive maintenance and sophisticated data analytics. This improves productivity and availability and adds value to their business offerings. For instance, GE is looking for opportunities in the IoT with industrial analytics. In addition, Apotex upgraded its manufacturing processes to automate manual processes. This includes ensuring consistent batch production by introducing RFID, sorting, and process flow tracking. Due to this, the company had real-time visibility into manufacturing operations.

- Furthermore, the industrial IoT trend is aided by smart factory initiatives, such as the Smart Manufacturing Leadership Coalition (SMLC) in the United States. This drives and facilitates the broad adoption of manufacturing intelligence due to massive amounts of machine and sensor data that need collection, processing, and formation of decisions.

- In June 2022, the Ministry of Foreign Affairs stated that the European market for Internet of Things (IoT) solutions is accelerating. Germany, the UK, and the Netherlands lead Europe in IoT adoption, while Eastern European and Nordic countries follow closely. The manufacturing, home, healthcare, and financial sectors are at the forefront of his IoT adoption, but retail and agriculture are also seeing impressive growth. Such advancement in multiple sectors will leverage the IoT chip market across Europe.

- The deployment of the wireless chip, including eLTE or NB-IoT chip for their manufacturing terminal, has been gaining traction over the years. For instance, Huawei collaborated with industrial partners to make smart terminals used in traditional manufacturing for uploading equipment data and receiving commands. eLTE or NB-IoT chip is added to the manufacturing terminal for transmitting data generated by the terminal via the eLTE or NB-IoT network, enabling manufacturing data to be collected and commands issued.

Asia Pacific is Expected to Witness Significant Growth

- Asia-Pacific accounts for a significant share of spending in IoT, with Singapore and South Korea as major markets adopting IoT chips. According to the Organization for Economic Co-operation and Development, South Korea is the first prominent market to connect more to the internet per habitat.

- In July 2022, KIOXIA Corporation and Western Digital Corporation announced their joint venture Fab7 manufacturing facility at Yokkaichi Plant had received approval from the Japanese government for a subsidy of up to JPY 92.9 billion. The subsidy is granted under a special government program to promote corporate investment in state-of-the-art semiconductor manufacturing facilities and ensure the stable production of semiconductors in Japan. Such collaborations in the region will help the IoT chip market to grow.

- IoT's infrastructure includes the demand for better wireless connectivity solutions to enable new phases in automation and transportation owing to the rise in demand for IoT chips and ICs in smart cities and domestic automation in the areas such as connected automobiles and smart transportation systems.

- Further, Asian governments are deeply integrating IoT in their long-term development projects. For instance, China's central government selected over 200 cities to pilot smart city projects. The cities include Beijing, Shanghai, Guangzhou, and Hangzhou. Furthermore, India's vision to transform 100 cities into smart cities is expected to promote electronics through smart homes and the automotive sector.

- In May 2022, Cyient partnered with IIT Hyderabad, India (IITH) and WiSig Networks, a start-up company founded in IITH, to launch India's first designed and engineered chip, Koala NB-IoT SoC (Narrowband IoT SoC). The Memorandum of Understanding (MOU) signed between the two aligns with the goals of MEITY (Ministry of Electronics and Information Technology, India) to build a vibrant semiconductor design and innovation ecosystem to serve the Indian world and further promote its development into a global electronics manufacturing and design hub.

- The region is expected to be a prominent provider of IoT spending as there is increased use of connected devices in sectors such as manufacturing. Increased adoption of 5G is helping the market grow in the upcoming years as there is an increase in IoT services.

IoT Chip Industry Overview

The Global Internet of Things (IoT) Chip Market is moderately competitive, with a considerable number of regional players. The companies are leveraging strategic collaborative initiatives and acquisitions to increase market share and profitability.

- June 2021 - Impinj Inc., which is a RAIN RFID provider and Internet of Things provider, announced the introduction of three new RAIN RFID reader chips that enable IoT device manufacturers to meet the increasing demand for item connectivity in applications such as retail, supply chain and logistics, and consumer electronics, among other markets.

- June 2021 - Qualcomm launched seven of its new IoT chipsets that were targeted at devices meant for logistics, warehousing, smart cameras, video collaboration, and retail, among other applications. The company also stated that these new IoT solutions offer significant capabilities for a wide range of connected solutions and smart devices with extended life hardware and software options to achieve long-term support for a minimum of eight years.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Technology Snapshot

- 4.4 Assessment of COVID-19 Impact on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rising Demand of Connected and Wearable Devices

- 5.1.2 Adoption of Advance Technologies Due to Rising Trend of Industry 4.0

- 5.2 Market Restraints

- 5.2.1 Issues Related to Security and Privacy of Data to Hinder the Adoption of IoT Devices

- 5.2.2 Lack of Standardization of Communication Protocol across Different Platforms

6 MARKET SEGMENTATION

- 6.1 By Product

- 6.1.1 Processor

- 6.1.2 Sensor

- 6.1.3 Connectivity IC

- 6.1.4 Memory Device

- 6.1.5 Logic Device

- 6.1.6 Other Products

- 6.2 By End-user

- 6.2.1 Healthcare

- 6.2.2 Consumer Electronics

- 6.2.3 Industrial

- 6.2.4 Automotive

- 6.2.5 BFSI

- 6.2.6 Retail

- 6.2.7 Building Automation

- 6.2.8 Other End-users

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East & Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Qualcomm Technologies Inc.

- 7.1.2 Intel Corporation

- 7.1.3 Texas Instruments Incorporated

- 7.1.4 NXP Semiconductors NV

- 7.1.5 Cypress Semiconductor Corporation

- 7.1.6 Mediatek Inc.

- 7.1.7 Microchip Technology Inc.

- 7.1.8 Samsung Electronics Co. Ltd

- 7.1.9 Silicon Laboratories Inc.

- 7.1.10 Invensense Inc.

- 7.1.11 STMicroelectronics NV

- 7.1.12 Nordic Semiconductor ASA

- 7.1.13 Analog Devices Inc.