|

市場調査レポート

商品コード

1641970

ケーブルコネクター:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Cable Connector - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ケーブルコネクター:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

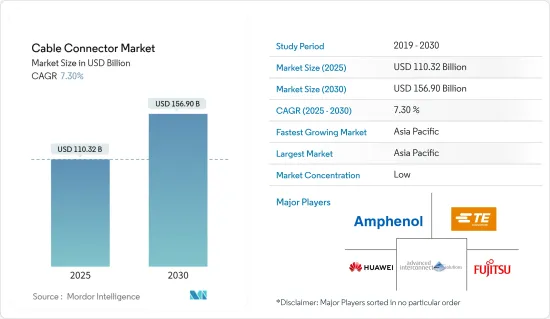

ケーブルコネクターの市場規模は2025年に1,103億2,000万米ドルと推計され、2030年には1,569億米ドルに達すると予測され、市場推計・予測期間(2025-2030年)のCAGRは7.3%です。

メディアとエンターテインメントに対する需要の高まりと、新興経済圏全体におけるインターネットの普及拡大により、テレビとインターネットの加入者数と、スマートフォン、PDA、タブレットの利用者数が増加しました。これらの要因によって、ケーブルコネクターアダプタに対する膨大な需要が創出され、これなしでは効果的なネットワーキングを確立できないです。

主なハイライト

- 世界のデジタル移行により、ケーブルコネクター市場は活況を呈しています。信頼性の高い接続性、高性能、効率性が市場の成長を後押しする主な要因です。高性能ネットワークは、ビジネス、製造、セキュリティ、メディアに不可欠です。さらに、USB Type-CやHDMIなどのケーブルが大きな人気を集めています。

- 長年にわたる固定ブロードバンド接続数の増加が、調査対象市場の成長を可能にしています。ITUによると、世界の固定ブロードバンド接続数は過去5年間で大幅に増加しており、これらの接続の設置にはコネクタが必要なため、調査対象市場の成長機会となっています。国際通信連合によると、世界の固定ブロードバンド接続数は2021年には約13億に増加します。

- 小型アプリケーション用のケーブルコネクターの使用は急速に拡大しています。モバイル技術、航空宇宙・防衛、医療技術など、いくつかの主要市場が市場の成長を牽引しています。スマートフォンやその他のハンドヘルド機器では、超高速データ通信が可能なマイクロコネクターなど、より小型で薄型の部品も必要とされています。例えば、10Gbpsの基板対基板コネクタは標準的であり、一部の先進的な小型基板対基板コネクタは20Gbpsまで対応できます。したがって、家電製品の成長は、ケーブルコネクターの需要に直接的な影響を及ぼしています。

- さらに、ほとんどのデータ接続と電源接続にはRFコネクターとケーブルが使用されており、こうした動向は高速データ、企業ネットワーキング、産業用IoTアプリケーションでも続くと思われます。欧州とAPACでは産業用モノのインターネット(IIoT)の採用が増加しており、コネクタ企業はUSB、CAT 5/6/7、HDMI、DisplayPortなどの新しいコネクタに目を向けています。例えば、Wurth Elektronikは2021年7月、極めてコンパクトな高周波同軸コネクタWR-UMRF(Ultra-Miniature RF Coaxial Connector)を発売しました。

- しかし、複雑な故障識別と修正手順、ケーブルコネクターの製造に使用される原材料価格の変動、Bluetooth、ワイヤレスHDMIトランスミッタなどのワイヤレス接続技術の開発などの課題が、調査した市場の成長に課題しています。

- COVID-19の発生は、他の国々とともに中国に封鎖を発表させ、初期段階では社会的隔離を実施させたため、調査市場の成長に顕著な影響を与えました。この影響により、多くの設備や機械の製造や生産が数週間にわたって停止しました。さらに、重要な原材料や産業機器の輸出入にさまざまな制限が課され、サプライチェーンが大きく混乱しました。しかし、世界のほぼすべての地域で規制が解除され、市場は勢いを取り戻すと予想されています。

ケーブルコネクター市場動向

自動車部門が大きな市場シェアを占める見込み

- 自動車部門は、オーディオ制御、ADAS(先進運転支援システム)、診断システム、クルーズコントロール、インフォテインメントシステムなどの高度な電子システムの採用により、コネクタの旺盛な需要を目の当たりにすると予測されます。さらに、電気自動車の人気の高まりが市場の成長を後押しすると予想されます。このセグメントの重要な市場動向には、デバイスの品質・信頼性基準を満たすための技術革新や設計改善、汎用性の高い小型コネクタの需要、RoHS対応、UL認定、IP規格コネクタの人気、EMI/RFI抑制機能を備えたインテリジェントコネクタなどがあります。

- 新しい自動車技術は、自動車の配線方法を変えました。重要な電気部品は、認証された条件下で電力、信号、データを確実に伝送することが求められています。ハイブリッド電気自動車や電気自動車は、堅牢なコネクター技術を適用する視野を、レースカーから自律走行車という形のロボット工学にまで広げました。このため、ケーブルコネクターだけでなく、設計、材料も大幅に開発されました。

- 現代の自動車の要件を満たすことができるコネクタに対する需要の高まりを考慮し、ケーブルコネクターを提供するベンダーは、ますます革新的な製品の開発に注力しています。例えば、ヒロセ電機は2021年12月、新しい電線対基板コネクタ「GT50シリーズ」を開発しました。このシリーズは、1mmピッチで125℃までの耐熱性を持ち、車載用途に最適な小型で堅牢な製品です。

- 電気自動車が従来の内燃機関車に急速に取って代わるという自動車業界の最近の動向の変化も、これらの自動車がより多くのセンサーや電子部品を搭載し、コネクターのユースケースを拡大していることから、研究市場の成長を支えるものと期待されています。例えば、国際エネルギー機関によると、世界で使用されているバッテリー電気自動車の数は、2016年の120万台から2021年には1,130万台に増加しています。

アジア太平洋地域が最速の成長率を記録する見込み

- アジア太平洋地域における通信技術の継続的な進歩とその他のエンドユーザー産業の成長は、ケーブルコネクター市場の発展を後押しする重要な要因の一つです。さらに、産業用アプリケーションにおける自動化プロセスのためのITと通信によるサポートが、メーカー間での採用を容易にしています。

- センサーコンポーネント、より高速なネットワーク、高レベルの信頼性と安全な階層アクセスを備えた柔軟なインターフェース、エラー訂正オプションは、この地域における生産性、継続的な品質納品、製造コストの最小化に貢献しました。さらに、開発、生産、ロジスティクス・チェーン全体(インテリジェント・ファクトリー・オートメーションとして知られる)の新しい技術的アプローチの中心にIoTがあることから、この地域ではケーブル・コネクタの採用が大幅に増加すると予想されます。

- 例えば、GSMAの推計によると、2025年までに世界全体で138億のIIoT接続が行われます。グレーターチャイナは、世界市場の3分の1にあたる約41億接続を占めると予想されています。2021年6月、中国工業情報化部(MIIT)は産業インターネット2021作業計画を発表し、同国の5Gネットワークと産業モノのインターネット(IIoT)をさらに拡大する目標を詳述しました。また、センサーや光ファイバーケーブルなどの電子部品の導入拡大がケーブルコネクターの需要を押し上げるため、こうした動向はさらなる成長機会を生み出すと予想されます。

- さらに、データセンターの増加と広帯域幅に対する需要の高まりが、ケーブルとコネクターの必要性を高めています。中国はデータセンター建設で世界の同業他社をリードすることに非常に注力しており、大企業はデータサービスの安定性と信頼性を確保するためにデータセンターの規模を拡大しようとしています。例えば、5G、ウェアラブルデバイス、モノのインターネット、人工知能の応用がコンピューティングパワーに対する急増する需要に拍車をかけています。

- また、自動車セクターの成長もアジア太平洋地域のケーブルコネクター市場開拓の重要な一因になると予想されます。例えば、中国自動車工業協会(CAAM)によると、中国では2021年に約290万台のバッテリー電気自動車が販売される予定です。

ケーブルコネクター産業の概要

ケーブルコネクター市場は断片化されています。初期投資が比較的少なくて済むため、新規参入企業は市場に迅速に参入できます。さらに、買収は長年にわたる市場の重要な傾向であり、大手企業はこれを利用して競争を減らし、市場でのプレゼンスをさらに拡大しています。主なプレーヤーには、Amphenol Corporation、Fujitsu Limited、TE Connectivity Limited、Huawei Technologiesなどがあります。

- 2022年9月- アンフェノールRFは、AUTOMATE Type A MiniFAKRA製品シリーズに構成済みケーブルアセンブリを追加しました。同社によると、これらのアセンブリは、両端にストレートクアッドポートminiFAKRAジャックを備え、低損失TFC302LL用に設計されています。さらに、これらのコネクターは、嵌合時の接触損傷を防ぐために嵌合部品のサイズを制限するクローズドエントリーケーブルインターフェイスで構成されています。

- 2022年7月- 電子部品の大手専門ディストリビューターであるTTI, Inc.は、TE Connectivityの産業用Mini-I/Oコネクタを在庫していると発表しました。Mini I/Oコネクタシリーズは、優れた耐衝撃性、耐振動性、耐衝撃性、耐EMI性をコンパクトなサイズで提供し、過酷な産業用アプリケーションで信頼性の高い高性能を発揮します。この開発により、TE Connectivityは新たな顧客へのリーチを拡大します。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3カ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

- 業界バリューチェーン分析

- COVID-19の業界への影響評価

第5章 市場力学

- 市場促進要因

- 電気通信分野における進歩の高まりと接続性向上への需要の高まり

- 高帯域幅に対する需要の増加

- 市場の課題

- 原材料価格の変動

第6章 市場セグメンテーション

- タイプ別

- PCBコネクター

- 丸型/角型コネクター

- 光ファイバーコネクター

- IOコネクター

- その他のタイプ

- 業界別

- ITおよび電気通信

- 自動車/運輸

- 家電(コンピューター、周辺機器、ビジネス機器を含む)

- 産業用

- その他エンドユーザー別(海底、航空宇宙、エネルギー・電力、医療)

- 地域別

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Amphenol Corporation

- Molex Inc.(Koch Industries)

- Fujitsu Limited

- Prysmian SpA

- Nexans SA

- TE Connectivity Limited

- 3M Company

- Huawei Technologies Co. Ltd

- Axon Cable SAS

- Alcatel-Lucent SA

- Aptiv PLC

- Yazaki Corporation

- Huber+Suhner AG

第8章 投資分析

第9章 市場の将来

The Cable Connector Market size is estimated at USD 110.32 billion in 2025, and is expected to reach USD 156.90 billion by 2030, at a CAGR of 7.3% during the forecast period (2025-2030).

The growing demand for media and entertainment and the increasing penetration of the internet across emerging economies led to the increase in the number of television and internet subscribers and users of smartphones, PDAs, and tablets. These factors created an immense demand for cable connector adapters, without which effective networking cannot be established.

Key Highlights

- The market for cable connectors is booming, owing to the global digital transition. Reliable connectivity, high performance, and efficiency are the major factors boosting the market's growth. High-performance networks are essential for business, manufacturing, security, and media. Furthermore, cables, such as USB Type-C and HDMI, are hugely popular.

- The growing number of fixed broadband connections over the years has enabled the growth of the market studied. According to ITU, the number of global fixed broadband subscriptions increased significantly in the last five years, which provides an opportunity for the growth of the market studied, as the installation of these connections requires connectors. According to the International Telecommunication Union, the number of fixed broadband connections globally will increase to about 1.3 billion in 2021.

- The use of cable connectors for miniature applications is rapidly growing. Several key markets, including mobile technology, aerospace and defense, and medical technology, drive the market's growth. Smartphones and other handheld devices also require smaller and lower-profile components, including micro-connectors capable of providing very high data speeds. For example, 10 Gbps board-to-board connectors are standard, and some advanced miniature board-to-board connectors can handle up to 20 Gbps. Therefore, the growth of consumer electronics is having a direct impact on the demand for cable connectors.

- Furthermore, most data and power connections use RF connectors and cables, and these trends will likely continue with high-speed data, enterprise networking, and industrial IoT applications. With the adoption of the Industrial Internet of Things (IIoT) increasing in Europe and APAC, the connector companies are turning to newer connectors, such as USB, CAT 5/6/7, HDMI, and DisplayPort, to name a few. For instance, in July 2021, Wurth Elektronik launched WR-UMRF (Ultra-Miniature RF Coaxial Connector), an extremely compact high-frequency coaxial connector.

- However, the factors such as complex fault identification and correction procedure, fluctuation in raw material prices used to manufacture cable connectors, and the development of wireless connectivity technologies such as Bluetooth, and wireless HDMI transmitters, among others, are challenging the growth of the studied market.

- The outbreak of COVID-19 had a notable impact on the growth of the studied market as it led China, along with other countries, to announce a lockdown and practice social isolation during the initial phase. This factor halted the manufacturing and production of numerous pieces of equipment and machinery for several weeks. Furthermore, various restrictions imposed on importing and exporting critical raw materials and industrial equipment significantly disrupted the supply chain. However, the market is expected to regain momentum with restrictions lifted in almost all parts of the world.

Cable Connector Market Trends

Automotive Sector is Expected to Hold Significant Market Share

- The automotive sector is projected to witness a strong demand for connectors, aided by the adoption of highly advanced electronic systems, such as audio controls, driver assistance systems, diagnostic systems, cruise control, and infotainment systems. Moreover, the increasing popularity of electric vehicles is expected to boost the market's growth. Some of the significant market trends in the segment include innovations and design improvements to meet the quality and reliability standards of devices, demand for versatile miniature connectors, the popularity of RoHS - compliant, UL recognized, and IP -rated connectors, as well as intelligent connectors with EMI/RFI suppression features.

- New automotive technologies have altered the ways cars are wired. The critical electrical components are required to reliably transmit power, signal, and data in certified conditions. The hybrid electric and electric vehicle has expanded the vision for applying robust connector technology from race cars to robotics in the form of autonomous vehicles. This has led to a significant development in design, material, as well as cable connectors.

- Considering the growing demand for connectors that can fulfill the requirements of modern automobiles, the vendors offering cable connectors are increasingly focusing on developing innovative products. For instance, in December 2021, Hirose Electric developed a new wire-to-board connector, the GT50 Series. This small and robust product series has a 1mm pitch and heat resistance up to 125-degree celsius, making it ideal for use in automotive applications.

- The recent shift in the automotive industry's trend wherein electric vehicles are fast replacing the traditional ICE vehicles is also expected to support the growth of the studied market as these vehicles contain more sensors and electronic components, expanding the use cases for connectors. For instance, according to the International Energy Agency, the global number of battery electric vehicles in use has increased from 1.2 million in 2016 to 11.3 million in 2021.

Asia-Pacific Expected to Witness the Fastest Growth Rate

- The continuous advancements in communication technologies and the growth of other end-user industries in the Asia Pacific region are among the significant factors boosting the development of the cable connectors market. Moreover, the support by IT and communications for automated processes in industrial applications have facilitated easier adoption among manufacturers.

- Sensor components, faster networks, flexible interfaces with high levels of reliability and secured hierarchical access, and error-correction options added to productivity, continued quality deliveries and minimized manufacturing costs in the region. Furthermore, with IoT at the center of new technological approaches for the development, production, and the entire logistics chain (otherwise known as intelligent factory automation), the adoption of cable connectors is expected to increase significantly in the region.

- For instance, according to the GSMA estimates, there will be 13.8 billion IIoT connections globally by 2025. Greater China is expected to account for around 4.1 billion connections or a third of the global market. In June 2021, the Chinese Ministry of Industry and Information Technology (MIIT) released its Industrial Internet 2021 Work Plan, detailing its goal to expand further the country's 5G network and the Industrial Internet of Things (IIoT). Such trends are also expected to create further growth opportunities as increased deployment of electronic components such as sensors and optic fiber cables will drive the demand for cable connectors.

- Furthermore, the growing number of data centers and rising demand for higher bandwidth drive the need for cables and connectors. China is highly focused on taking the lead over global peers in data center construction, with larger enterprises looking to scale up their data centers to ensure stability and reliability of data services, such as the application of 5G, wearable devices, the internet of things, and artificial intelligence spurs a burgeoning demand for computing power.

- The growth of the automotive sector is also expected to be a vital contributor to the development of the cable connectors market in the Asia Pacific region. For instance, according to the China Association of Automobile Manufacturers (CAAM), about 2.9 million battery electric vehicles will be sold in China in 2021.

Cable Connector Industry Overview

The Cable Connector Market is fragmented. The relatively lower initial investment requirement enables new players to enter the market quickly. Moreover, acquisitions have been a critical trend in the market over the years as the bigger players are using this to reduce competition and further expand their market presence. Some key players include Amphenol Corporation, Fujitsu Limited, TE Connectivity Limited, and Huawei Technologies Co. Ltd.

- September 2022 - Amphenol RF expanded its AUTOMATE Type A MiniFAKRA product series with pre-configured cable assemblies. According to the company, these assemblies feature a straight quad port miniFAKRA jack on both ends and are designed for low-loss TFC302LL. Furthermore, these connectors are constructed with a closed entry cable interface which limits the size of mating parts to prevent contact damage during mating.

- July 2022 - TTI, Inc., a leading specialty distributor of electronic components, announced that it is stocking the Industrial Mini-I/O connectors from TE Connectivity. The Mini I/O range of connectors provides excellent shock, vibration, shock, and EMI resistance, in a compact size and delivers reliable high performance in rugged industrial applications. The development will expand the reach of TE Connectivity to new customers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of the Impact of COVID-19 on the Industry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Advancements In The Telecom Sector Coupled With Greater Demand for Improved Connectivity

- 5.1.2 Increasing Demand for High Bandwidth

- 5.2 Market Challenges

- 5.2.1 Volatile Prices of Raw Material

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 PCB Connectors

- 6.1.2 Circular/Rectangular Connectors

- 6.1.3 Fiber Optic Connectors

- 6.1.4 IO Connectors

- 6.1.5 Other Types

- 6.2 By End-user Vertical

- 6.2.1 IT and Telecom

- 6.2.2 Automotive/Transportation

- 6.2.3 Consumer Electronics (Including Computer, Peripherals, and Business Equipment)

- 6.2.4 Industrial

- 6.2.5 Other End -user Verticals (Submarine, Aerospace, Energy and Power, and Medical)

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia Pacific

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Amphenol Corporation

- 7.1.2 Molex Inc. (Koch Industries)

- 7.1.3 Fujitsu Limited

- 7.1.4 Prysmian SpA

- 7.1.5 Nexans SA

- 7.1.6 TE Connectivity Limited

- 7.1.7 3M Company

- 7.1.8 Huawei Technologies Co. Ltd

- 7.1.9 Axon Cable SAS

- 7.1.10 Alcatel-Lucent SA

- 7.1.11 Aptiv PLC

- 7.1.12 Yazaki Corporation

- 7.1.13 Huber+Suhner AG