|

市場調査レポート

商品コード

1910493

高級アパレル市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Luxury Apparel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 高級アパレル市場:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 130 Pages

納期: 2~3営業日

|

概要

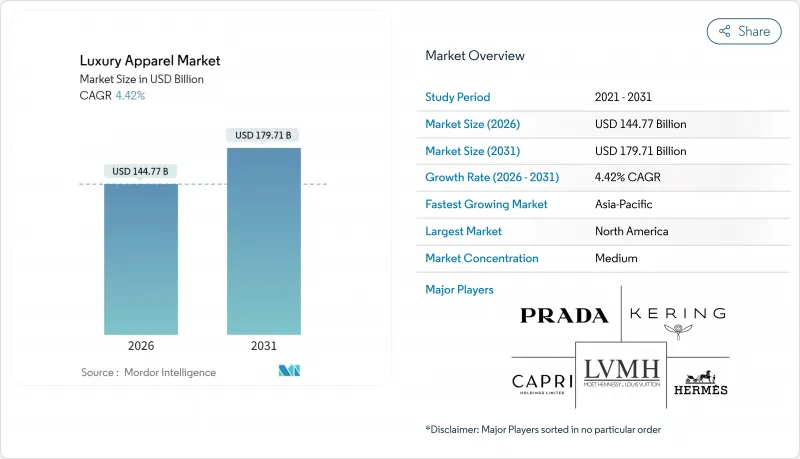

高級アパレル市場は、2025年の1,386億4,000万米ドルから2026年には1,447億7,000万米ドルへ成長し、2026年から2031年にかけてCAGR 4.42%で推移し、2031年までに1,797億1,000万米ドルに達すると予測されております。

この回復力は、消費者がプレミアムな職人技、透明性の高いサプライチェーン、没入型のショッピング体験に投資する意欲によって支えられています。ブロックチェーンを活用したデジタル製品パスポートの普及、旅行小売業の復活、ストリートウェアと伝統的デザインの融合といった要因が、市場範囲を拡大しています。同時に、持続可能性に関する規制の強化により運営基準が向上し、トレーサビリティと少量生産に既に注力しているブランドの価格決定力が強化されています。競合環境は、技術統合、戦略的統合、オムニチャネル小売の影響を受けて変化しています。高級品コングロマリットは、在庫最適化のためにAI予測ツールを活用し、販売時点での真正性確認を確実にするためNFCタグを導入しています。

世界の高級アパレル市場の動向と洞察

持続可能な高級素材への需要拡大

規制要件がラグジュアリーアパレル生産の経済構造を再構築しています。欧州連合(EU)のデジタル製品パスポート要件は新たなコンプライアンスコストを導入し、意図せず市場リーダーの競争優位性を強化しています。2024年カリフォルニア州責任ある繊維回収法では、売上高10億米ドル超の生産者は2026年7月までに生産者責任組織(PRO)への参加が義務付けられます。この措置は事実上の規制障壁となり、既存のラグジュアリー企業を優遇し、その市場シェアを固める効果があります。フランスが提案するファストファッションへの課税枠組み(たばこ税に類似)は、意図せず高級ブランドに利益をもたらします。そのプレミアム価格設定と限定生産量は、持続可能性目標と調和するからです。2027年までに施行予定のEU企業持続可能性デューデリジェンス指令は、サプライチェーンの透明性を誇る高級ブランドに有利に働きます。対照的に、中小規模の企業はより高いコンプライアンスコストに直面しています。こうした変化する規制状況に対応し、高級ブランドはブロックチェーンベースの認証システムへの移行を加速させています。

ソーシャルメディアと著名人起用による影響力

ラグジュアリーブランドは戦略を転換し、単なる起用からブランドエコシステムへの深い統合へと移行しています。この進化の中で、各ブランドは独占的なタレント提携を激しく争い、マーケティング効果を増幅させています。この転換の好例が、シャネルが2025年にケンドリック・ラマーをブランドアンバサダーに起用した件です。この動きは、単なる人口統計的リーチよりも文化的影響力を重視する戦略的転換を示し、若年層消費者を明確にターゲットとしています。別の事例として、ナイキとキム・カーダシアンの「ナイキ・スキムズ」のコラボレーションは、ラグジュアリーブランドと隣接ブランドの融合を浮き彫りにしています。ここでは、セレブリティ起用の影響力が新たな製品カテゴリーを生み出し、伝統的なラグジュアリーの枠組みに課題しています。さらに、世界のソーシャルメディアインフルエンサーがラグジュアリーアパレルブランドを推奨するケースが増加しており、リールや動画を通じてその利点や品質を紹介しています。この動向は、ソーシャルメディアへの関与度が高いZ世代やミレニアル世代に特に共感を呼んでいます。これを裏付けるように、2025年のStatCounter Global Statsのデータによると、英国の個人の66.08%がFacebookを利用しており、10.73%がInstagramを利用していました。

偽造品の蔓延

偽造品は価格の整合性を損ない、ブランドの威信を低下させることで高級アパレル市場を脅かしています。現代の精巧な複製品は、本物の生地や吊り下げタグ、さらにはデジタルIDまでも忠実に模倣します。この状況を受け、正規事業者は法的保護、税関職員の訓練、鑑識的認証への投資を余儀なくされています。主要企業はブロックチェーン連合を主導し、消費者がアプリで読み取れるシリアルタグを導入しています。しかしwhitecase.comが指摘するように、この導入は依然として不均一で資本集約的です。発展途上市場、特にアジア太平洋地域の一部では、根強い生産クラスターが取締りの課題となっています。代替品の脅威は資源を消耗させる一方で、業界を高度なセキュリティ技術へ導き、税関当局との緊密な連携を促進しています。

セグメント分析

2025年には、Tシャツとシャツが売上高の44.62%を占め、快適性と高級感のニュアンスをシームレスに融合させた日常着への消費者の志向を浮き彫りにしました。この優位性は、高級アパレル市場がベーシックアイテムに注力する姿勢を確固たるものにするだけでなく、上質なコットン、シルク混紡、職人技による仕上げの高価格設定を正当化するものです。ジャケット、スウェットシャツ、フーディーは4.72%のCAGRで最も急速な収益成長が見込まれています。この急成長は、通気性メンブレンや撥水加工カシミアなど、機能性素材の汎用性拡大に起因します。一方、オンライン抽選で頻繁に発表されるラグジュアリーストリートウェアのカプセルコレクションは、販売率とソーシャルメディアでの話題性を共に加速させています。

ドレスやガウンは式典需要に応え、ジーンズは若年層をブランドの世界へ誘い込み、将来的な高利益商品へのクロスセリングの基盤を築きます。今後の高級アパレル市場では、プレミアムインナーウェアへの投資拡大が見込まれます。各ブランドは「肌に直接触れる快適さ」というコンセプトを積極的に活用しようとしています。一方、ショートパンツやスカートは、富裕層のリゾートウェア志向の高まりから恩恵を受けており、この動向はレジャー旅行の増加によってさらに後押しされています。全体的に見て、耐久性、修理サービス、再生可能素材といった特性が、従来の美的要素を上回る重要な購買動機となりつつあります。

2025年には、ファッションとカジュアルウェアが売上高の65.05%を占め、単なる機会限定の服装ではなくライフスタイルの選択肢としての地位を確固たるものにしました。しかしアスレジャーは、5.05%という力強いCAGRで拡大する見込みであり、他のすべてのカテゴリーを上回り、高級アパレル市場がパフォーマンス重視のエレガンスへと軸足を移していることを浮き彫りにしています。スポーツ参加者の増加に伴い、市場参入企業はこの急成長する需要に応えるため、ラグジュアリーアスレジャーラインを発表しています。2024年のスポーツイングランドのデータによると、英国では669万5,500人がフィットネスクラスに参加し、222万2,500人がサッカーに参加しました。リサイクルポリアミド製の高機能レギンスから、防臭性のあるメリノポロシャツ、吸湿発散性に優れたカシミアフーディーまで、ラグジュアリー要素がウェルネス中心のワードローブにシームレスに組み込まれています。この進化は、機能性と高級感ある美学を融合させたアパレルへの消費者の需要の高まりを裏付け、生地技術とデザインの進歩を推進しています。

健康意識の高まり、オフィスのドレスコード緩和、ハイブリッドワークモデルの普及に伴い、汎用性の高い服装への需要が急増しています。ラグジュアリーブランドは、独自のニット技術と生体力学的デザインを駆使し、ジムから高級レストランまでシームレスに移行できる衣類にプレミアム価格を設定しています。スポーツとファッションの境界がますます曖昧になる中、旅行用品、靴、アクセサリーとのクロスマーチャンダイジングの好機が訪れ、顧客支出の増加につながっています。さらに、スポーツとスタイルの融合は、ラグジュアリーブランドとアクティブウェア企業間の提携を促進し、市場の成長軌道を加速させています。

地域別分析

2025年、北米は世界のラグジュアリー市場収益の27.62%を占めました。これは豊かなラグジュアリー文化の伝統、超高富裕層の集中、そして堅調な観光支出に支えられた結果です。ニューヨークに55,000平方フィートの旗艦店を開設したプランタンは、eコマースの台頭にもかかわらず、高級不動産への継続的な投資を強調しています。カリフォルニア州の繊維製品回収義務化など地域の持続可能性関連法規は事業運営を複雑化させる一方、コンプライアンスコストを管理できる確立されたプレイヤーに報いる側面もあります。

アジア太平洋地域は2031年までCAGR6.48%で高級アパレル市場を牽引します。この成長は中産階級の所得増加、デジタル購買への移行、越境旅行の回復によって支えられています。円安の日本にはバーゲンハンティングの観光客が訪れ、来日者数の回復に伴い百貨店の売上は過去最高を記録しています。同時に、香港ランドが10の多階層メゾンコンセプトを擁するランドマーク複合施設の拡充に10億米ドルを投資したことは、グレーターチャイナ地域における高級ファッション需要への強気な見通しを示しています。

欧州では、確立された需要と厳格な規制が共存する状況です。EUの企業サステナビリティデューデリジェンス規則導入により文書化基準が強化される一方、トップメゾンはこの課題を透明性を強みとする機会と捉えています。ミラノのモンテ・ナポレオーネ通りでは、年間賃料が平方メートル当たり2万3,583米ドルに達し、観光客の関心によって支えられる高級ショッピング街の回復力を示しています。一方、ブレグジットはクリエイティブ人材の移動構造を変え、汎欧州ビジネスにおける調達・物流に新たな課題を提示しています。南米、中東・アフリカは長期的な成長可能性を秘める一方、為替変動やインフラ課題が即時的な拡大の障壁となっています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 持続可能な高級素材への需要拡大

- ソーシャルメディアと著名人起用による影響

- 生地とデザインにおける技術的進歩

- ファッション動向の世界の化

- ラグジュアリーストリートウェアおよびアスレジャーの拡大

- 旅行・観光の増加

- 市場抑制要因

- 偽造品の蔓延

- 価格に敏感な消費者からの需要の減少

- 価格に敏感な地域における普及の遅れ

- 排他性とアクセシビリティのバランス調整における課題

- 消費者行動分析

- 規制の見通し

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- 製品タイプ別

- ズボン

- ジーンズ

- Tシャツとシャツ

- ショートパンツとスカート

- ジャケット、スウェットシャツ、フーディ

- インナーウェア

- ドレスとガウン

- その他の製品タイプ

- 最終用途別

- アスレジャー

- ファッションとカジュアル

- エンドユーザー別

- 男性

- 女性

- キッズ/子ども向け

- 流通チャネル別

- 専門店

- オンライン小売店

- その他流通チャネル

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- フランス

- 英国

- オランダ

- イタリア

- スウェーデン

- ポーランド

- ベルギー

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- インドネシア

- タイ

- シンガポール

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- チリ

- コロンビア

- ペルー

- その他南米

- 中東・アフリカ

- アラブ首長国連邦

- 南アフリカ

- ナイジェリア

- サウジアラビア

- モロッコ

- トルコ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Kering SA

- LVMH Moet Hennessy Louis Vuitton

- Hermes International S.A.

- Burberry Group plc

- Prada S.p.A.

- Giorgio Armani SpA

- Capri Holdings Ltd

- Chanel S.A.

- Ralph Lauren Corporation

- Brunello Cucinelli SpA

- Moncler S.p.A.

- Ermenegildo Zegna NV

- PVH Corp.(Tommy Hilfiger Collection)

- Valentino S.p.A.

- Salvatore Ferragamo S.p.A.

- Max Mara S.r.l.

- Stella McCartney Limited

- Canada Goose Holdings Inc.

- Loro Piana S.p.A.

- Compagnie Financiere Richemont SA