|

市場調査レポート

商品コード

1939679

UV硬化接着剤:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)UV-Curable Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| UV硬化接着剤:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

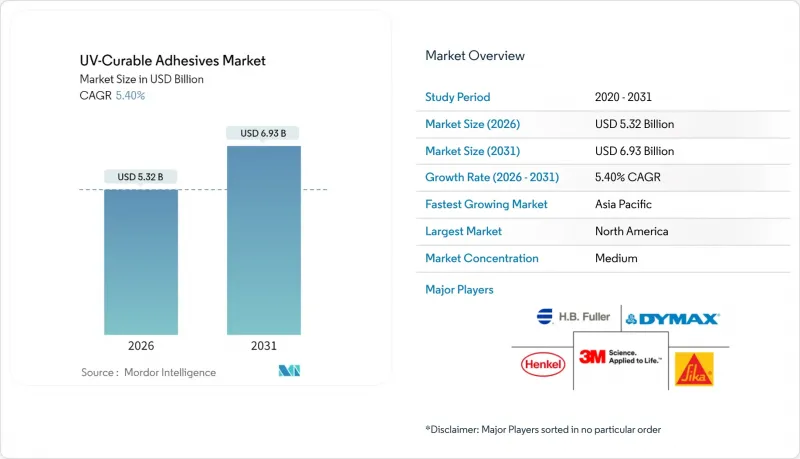

UV硬化接着剤市場は、2025年の50億5,000万米ドルから2026年には53億2,000万米ドルへ成長し、2026年から2031年にかけてCAGR5.4%で推移し、2031年までに69億3,000万米ドルに達すると予測されております。

医療機器、民生用電子機器、自動車用複合材、包装など、あらゆる主要な最終用途分野において、UV硬化接着剤市場はニッチな用途から必須の生産投入物へと進化しています。これは主に、オンデマンドでの即時硬化によりオーブン滞留時間が不要となり、揮発性有機化合物(VOC)の排出が削減され、軽量な複合材料アセンブリの実現を支援するためです。成長の勢いは、半導体の微細化、溶剤フリー化学を促進する欧米の厳格なVOC規制、光開始剤の安定供給を確保する垂直統合型サプライチェーンからも恩恵を受けています。北米は先進的な医療機器製造と自動車業界における光硬化構造接着剤の早期採用により技術的優位性を維持し、アジア太平洋地域は半導体パッケージング能力の増強を背景に成長を加速させています。競合環境においては、製品革新と規制対応の専門知識、特にISO 10993およびREACHガイドラインに適合した配合技術を有する企業が優位性を獲得しています。

世界のUV硬化接着剤市場の動向と洞察

自動車・航空宇宙分野におけるUV硬化接着剤の導入

電気自動車生産の増加に伴い、自動車メーカーはアルミニウムと炭素繊維など異種基材を熱歪みを生じさせずに接合する必要に迫られており、UV硬化接着剤市場は数秒で完全硬化しながら高い重ねせん断強度を維持する配合を提供しています。Polestar 1やロンドンのTX5タクシープラットフォームは、この手法による量産実現可能性を実証し、軽量化と車内騒音管理の両方を達成しています。航空宇宙生産においても、UV硬化技術がオートクレーブ工程の短縮と複合材積層板のエネルギー消費削減を実現するため、自動車業界と同様の動向が見られます。世界のバッテリーパック生産の拡大に伴い、利害関係者は2030年まで高温耐性UV硬化エポキシ樹脂の需要がさらに高まると予測しております。

より厳格なVOC/REACH規制が溶剤フリー化学品を後押し

2023年8月のEUにおけるジイソシアネート含有量0.1%超の規制は、コンバーターにゼロエミッションソリューションへの移行を迫り、UV硬化接着剤市場に即時の規制後押しをもたらしました。2024年1月のカナダVOC規制上限値はこれを反映し、北米のフレキシブル包装ラインにおける採用をさらに促進します。ライフサイクルアセスメント指標が調達基準となる中、無溶剤硬化技術は優れた環境ラベルを獲得し、ブランドのESG評価を高めます。ヘンケルなどの主要サプライヤーは現在、CO2回収原料プロセスを商業化しており、完成接着剤の埋め込み炭素量を低減しています。APAC地域でも同様のVOC指令が検討されているため、2年以内に無溶剤基準の世界の調和が実現し、競合する二液性エポキシ樹脂に先駆けてUV技術の普及が加速する見込みです。

UV-LED硬化システムの高い資本コスト

産業用LEDアレイの価格は5万~50万米ドルに上り、電力コスト削減により大量生産時には投資回収が可能ですが、中小企業は設備更新の資金調達に苦慮し、全ラインの転換が遅れています。波長変更に伴う工程の再検証はダウンタイムリスクを伴い、急速な技術革新サイクルにより投資回収前に陳腐化が懸念されます。ベンダーはリースモデルやモジュール式ヘッドユニットで対応していますが、世界的に融資環境は依然として不均一です。EUや米国における省エネルギー補助金連動型インセンティブが格差解消に寄与する可能性はありますが、普及が拡大するまでは設備費用が一部の接着剤需要を抑制する要因となるでしょう。

セグメント分析

アクリル系配合は、成熟したサプライチェーンと多基材対応性により、2025年のUV硬化接着剤市場シェアの47.10%を占めました。アクリル系製品の市場規模は、価格安定化と世界の調達を可能にする汎用規模の原料供給に支えられています。しかしながら、2031年までにCAGR5.55%と予測されるエポキシ系製品が、高弾性率と耐熱サイクル性能が必須となる自動車構造用接合部や半導体アンダーフィル分野において、アクリル系製品の優位性を侵食しつつあります。

カチオン系光開始剤の最近の革新により、ガラス転移温度を損なうことなくエポキシ硬化時間を数分から数秒に短縮でき、高速ラインタクトを実現しています。シリコーンやポリウレタンは、極端な温度変動や高い柔軟性が引張強度の必要性を上回るニッチ市場で存在感を維持しています。予測期間において、特定アクリレートモノマーに対するREACH規制の継続的な監視により、アクリル樹脂のコスト優位性が縮小する可能性があります。これにより、特殊エポキシ樹脂がUV硬化接着剤市場の主流用途へさらに進出する可能性があります。

UV硬化接着剤レポートは、樹脂タイプ(シリコーン、アクリル、ポリウレタン、エポキシ、その他樹脂タイプ)、エンドユーザー産業(医療、電気・電子、輸送、包装、家具、その他エンドユーザー産業)、地域(アジア太平洋、北米、欧州、南米、中東・アフリカ)別に分類されています。市場予測は金額(米ドル)で提供されます。

地域別分析

北米地域は2025年に世界収益の42.80%を占めました。ミネソタ州、カリフォルニア州、オンタリオ州のOEMメーカーがカテーテルや診断用センサー向けにFDA認可グレードを採用した一方、デトロイトの電気自動車工場ではバッテリーパックにUV構造接着剤を導入したためです。同地域は新規化学品の市場投入期間を短縮する透明性の高い規制経路の恩恵も受けており、サプライヤーの研究開発投資を後押ししています。

アジア太平洋地域は、中国、台湾、韓国における半導体パッケージング能力の急増を背景に、5.65%という最速のCAGRを達成しています。長虹ポリマーの16億米ドル規模のアクリル酸複合施設と、新潟におけるデュポンのフォトレジスト拡張が、地域の原材料および先端材料エコシステムを支えています。自動車需要は、日本および中国の自動車メーカーが複合材料シャーシの採用を拡大するにつれて増加し、高弾性率UVエポキシ樹脂に対する新たな需要を生み出しています。

欧州では、溶剤系競合製品を排除しコンプライアンスコストを増加させる厳格なREACH規制の影響でバランスが拡大しています。持続可能性への要請が、ヘンケル・セラネース社のCO2由来原料や、サペラテック社技術を活用した接着剤リサイクルといった循環型設計の採用を促進しています。中東・アフリカおよび南米は新興市場ながら、食品輸出向けフレキシブル包装設備の導入が勢いを示し、UV硬化接着剤市場に追加需要をもたらしています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 自動車および航空宇宙分野におけるUV硬化接着剤の採用

- より厳格なVOC/REACH規制により、無溶剤化学物質が有利に

- 民生用電子機器の小型化

- ウェアラブル医療機器における急速な普及

- インラインデジタル包装印刷ラインにおける即時接着の需要

- 市場抑制要因

- UV-LED硬化システムの高い資本コスト

- 代替となる2液型エポキシ樹脂およびシアノアクリレートの入手可能性

- 主要光開始剤の供給の不安定さ

- バリューチェーン分析

- ポーターのファイブフォース

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- 樹脂タイプ別

- シリコン

- アクリル

- ポリウレタン

- エポキシ

- その他の樹脂タイプ

- エンドユーザー産業別

- 医療

- 電気・電子機器

- 輸送機関

- 包装

- 家具

- その他のエンドユーザー産業

- 地域別

- アジア太平洋地域

- 中国

- 日本

- 韓国

- インド

- インドネシア

- マレーシア

- タイ

- ベトナム

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- 北欧諸国

- トルコ

- ロシア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- カタール

- エジプト

- ナイジェリア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/ランキング分析

- 企業プロファイル

- 3M

- Arkema

- artience Co., Ltd.

- AVERY DENNISON CORPORATION

- DELO Industrie Klebstoffe GmbH & Co. KGaA

- Dymax

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Master Bond Inc.

- Panacol-Elosol GmbH

- Parson Adhesives, Inc.

- Permabond LLC

- Sika AG