|

市場調査レポート

商品コード

1910520

ペット用口腔ケア製品:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Pet Oral Care Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ペット用口腔ケア製品:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

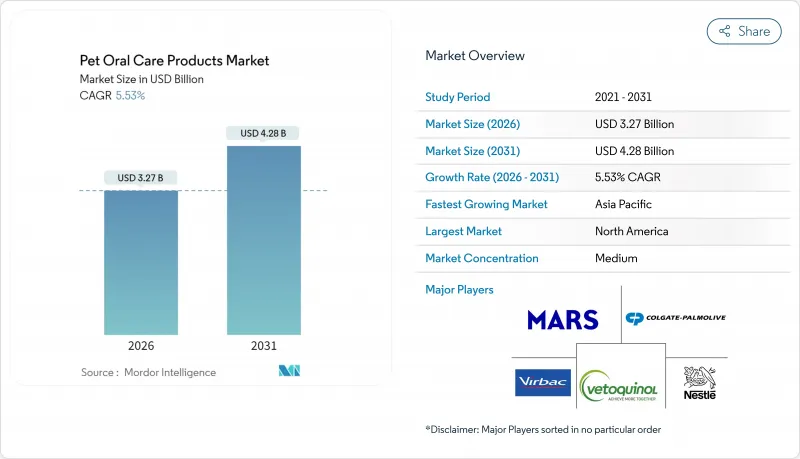

2026年のペット用口腔ケア製品市場規模は32億7,000万米ドルと推定され、2025年の31億米ドルから成長が見込まれます。

2031年までの予測では42億8,000万米ドルに達し、2026年から2031年にかけてCAGR5.53%で拡大する見通しです。

成長の背景には、歯周病の蔓延、予防的健康管理を重視するペットの人間化傾向の高まり、そして獣医テレデンティストリーの普及により、医療サービスが行き届いていない地域にも専門的な指導が届くようになったことが挙げられます。デンタルチューは、使用頻度が低い家庭にも適しているため収益の大部分を占めており、一方、水添加剤は「セットして放置するだけ」の利便性と、ブラッシングなしで歯垢を分解する酵素技術革新を背景に成長を加速させています。eコマースの急速な普及、定期購入プログラム、ターゲットを絞ったソーシャルメディア展開により、特にミレニアル世代のペットオーナー層において、情報収集から購入までのプロセスが短縮されています。一方、キシリトールや効能表示に関する規制当局の監視強化により、メーカーは検証済みの原料への投資や獣医口腔保健評議会(VOHC)の認証取得を迫られており、中小ブランドの参入障壁が高まっています。

世界のペット口腔ケア製品市場の動向と洞察

ペットにおける歯周病の高い罹患率

6歳までに犬の少なくとも44%、猫では最大85%が歯周病変に罹患しており、口腔ケアは任意のカテゴリーから医療上の必要性へと変化しています。心臓・肝臓・腎臓の病態は口腔内細菌の移行と相関するため、飼い主は酵素歯磨き粉、VOHC認定のガム、抗菌性水添加剤を選択する動機が高まっています。小型犬種はリスクが高く、ヨークシャーテリアでは未治療の場合、生後37週間以内に98%が歯周炎を発症します。口腔衛生が全身の健康状態と関連しているという臨床的証拠から、支出は美容目的のグルーミングから予防的治療へと移行しています。

ペットの人間化とプレミアム支出の増加

ペットオーナーの85%が、ペット用サプリメントを自身の栄養ニーズと同等と認識しており、ヒューマングレードの処方と透明性のある表示への需要を後押ししています。特に中国では、中産階級の台頭に伴いプレミアムペット支出が増加する中、サプリメント購入者の78%が価格よりも原材料の品質を重視しています。ブランドは、ヒト向け機能性食品の動向を反映したポストバイオティック粉末や海藻系ガムで対応しています。

歯磨き習慣の低い飼い主の順守率

毎日の歯磨き習慣に対する飼い主の順守率は依然として極めて低く、ヨークシャーテリアを対象とした研究では、専門家の指導や製品提供にもかかわらず、週平均の歯磨き成功率はわずか3.99%でした。この順守率の低さが、従来の歯磨き粉とブラシの組み合わせの市場成長を阻害しており、メーカーは飼い主の介入を最小限に抑える水添加剤、デンタルガム、スプレー剤などの代替投与方法の開発を迫られています。

セグメント分析

デンタルチューは、飼い主の積極的な歯磨き介入に対する順守率が低い状況と合致する利便性とペットの受容性により、2025年時点でペット口腔ケア市場シェアの41.92%を占め、圧倒的な市場リーダーシップを維持しています。水添加剤は2031年までCAGR6.05%で最も急速に成長するセグメントとして台頭しており、飼い主の介入を最小限に抑えた受動的口腔ケア提供へのパラダイムシフトを象徴しています。オラティーン水添加剤などの製品は、デキストラーゼ、グルコースオキシダーゼ、ラクトペルオキシダーゼなどの酵素システムを活用し、プラークバイオフィルムを溶解しながら、アルコール、キシリトール、クロルヘキシジンを含まないため、毎日の安全性を確保しています。歯磨き粉と歯ブラシのセグメントは、使用継続の課題による逆風に見舞われていますが、マウスウォッシュやリンスは、ブラッシングへの抵抗を回避するスプレー式アプリケーションを通じて支持を得ています。

獣医処方製品はプレミアム価格が設定されていますが、特に新興市場では獣医師不足による流通制約に直面しています。ナイジェリアでは推奨最低基準の3,870名に対し、現役獣医師はわずか3,500名と報告されています。歯科用ワイプや口腔プロバイオティクスタブレットなどの他の製品タイプは、専門的な用途を通じてニッチ市場を獲得しており、口腔内微生物叢の調節を目的としたプロバイオティクス製剤は科学的裏付けを得つつあります。この分野では、有効成分の効能を保持するコールドエクストルージョン製造プロセスが活用されており、プロバイオティクスや酵素などの機能性化合物が高温処理で劣化するという従来の課題を解決しています。

地域別分析

2025年時点で北米はペット口腔ケア製品市場シェアの39.35%を占め首位を維持しております。これは69%のペット飼育世帯率と、マース社が約3,000施設に展開する広範な動物病院ネットワークによるものです。同ネットワークは健康管理パッケージを通じた購買行動に影響を与えております。米国では定期購入サービスの導入率が最も高く、飼い主様が消耗品の自動配送サービスを活用されております。

アジア太平洋地域は6.63%のCAGRで最も急速に拡大する地域であり、中国のペット産業が牽引しています。中国のペット産業は、若年層の独身都市住民が伴侶動物に高級ケアを施す傾向から、2030年までに7,565億元(1,051億米ドル)に達する見込みです。eコマースの浸透率は従来型チャネルを上回り、国内プラットフォームでは視聴者を高頻度購入者に転換させるライブ配信教育セッションが展開されています。日本と韓国では科学的に裏付けられた機能性おやつが好まれ、インドでは遠隔獣医相談とラストマイル配送を組み合わせたテレヘルス対応サイトが普及しています。

欧州では、配合メーカーが天然素材や持続可能な包装に注力する中、着実な成長を維持しています。厳格な表示規制により、早期に地域横断的なコンプライアンス投資を行った企業が優位性を得ています。

ブラジルは2029年までに87%の成長が見込まれる南米市場の核となる一方、ペット用品への51%の複合税率が価格設定の障壁となっています。中東・アフリカ地域は未成熟ながら、都市化と可処分所得の増加が、獣医療インフラが整えば潜在需要が顕在化する可能性を示唆しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- ペットにおける歯周病の高い罹患率

- ペットの人間化傾向の高まりとプレミアム支出の増加

- eコマースの拡大がDTC口腔ケア定期購入サービスを後押し

- 新規機能性成分による製品差別化の推進

- 獣医テレデンティストリーの普及によるアクセス拡大

- AIを活用した噛みごたえ設計による歯科効果と飼い主の関与向上

- 市場抑制要因

- 飼い主様の歯磨き習慣への順守率が低いこと

- 製品効能表示に関する規制の曖昧さ

- 新興市場における認定獣医歯科医の不足

- 天然・手作り療法の急増に伴う成分安全性の懸念

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- テクノロジーの展望

- 規制情勢

第5章 市場規模と成長予測

- 製品タイプ別

- 歯磨き粉

- 歯ブラシ

- マウスウォッシュおよびリンス

- デンタルチュー/おやつ

- 水添加剤およびスプレー

- 獣医処方製品

- その他の製品タイプ(デンタルワイプ、口腔プロバイオティクスタブレットなど)

- 動物のタイプ別

- 犬

- 猫

- その他の伴侶動物(ウサギ、フェレットなど)

- 流通チャネル別

- スーパーマーケットおよびハイパーマーケット

- オンラインチャネル

- ペット専門店

- 獣医向けチャネル

- その他のチャネル(定期購入ボックス、グルーミングサロンなど)

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- チリ

- その他南米

- 中東

- サウジアラビア

- アラブ首長国連邦

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Mars, Incorporated

- Colgate-Palmolive Company(Hill's Pet Nutrition)

- Nestle Purina Petcare

- Virbac S.A.

- Elanco Animal Health Incorporated

- Vetoquinol S.A.

- Ceva Sante Animale

- Central Garden & Pet Company

- TropiClean Pet Products(Cosmos Corporation)

- Swedencare AB

- Sentry Pet Care(Perrigo Company plc)

- HealthyMouth LLC

- Ark Naturals Company