獣医用手術器具:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)

Veterinary Surgical Instruments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)- 発行日

- ページ情報

- 英文 112 Pages

- 納期

- 2~3営業日

- 商品コード

- 1850341

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

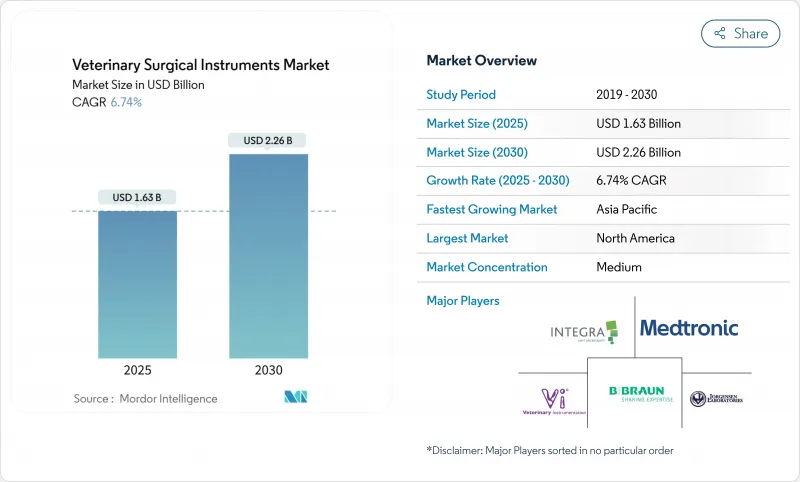

獣医用手術器具市場は、2025年に16億3,000万米ドルと評価され、2030年には22億6,000万米ドルに達し、CAGR 6.74%で進展すると予測されています。

コンパニオンアニマルの需要、電気手術における急速な技術革新、ペット保険の適用拡大が収益を押し上げています。高精度に基づくプロトコル、特に低侵襲手術は、クリニックが高精細視覚化、バイポーラ電気手術、3Dプリント整形外科インプラントにアップグレードすることを後押ししています。アジア太平洋は、可処分所得の増加、政府主導のインフラ・プログラム、都市部でのペット数の増加により、最も強い勢いを見せています。整形外科手術は、カスタムインプラントとAIガイド付きプランニングに支えられ、次の成長エンジンとして浮上しています。しかし、高い資本コストと認定外科医の世界的な不足が導入率を脅かしており、トレーニングの重要性と新しい機器に対する柔軟な資金調達の重要性が浮き彫りになっています。

世界の獣医用手術器具市場の動向と洞察

動物における低侵襲手術の動向

腹腔鏡手術や関節鏡手術の需要が獣医用手術器具市場を変革しています。トロッカー、カニューレ、HD内視鏡が開腹手技に取って代わると、回復時間は最大65%短縮し、合併症発生率は低下します。米国の専門クリニックの報告では、42%が避妊手術にMISを導入し、整形外科専門医の56%が関節診断の精緻化のために関節鏡を導入しています。より短い回復期間を売りにしているクリニックは、より高い症例受け入れ率を示しており、ディストリビューターはMIS対応キットを優先するよう促しています。メーカー各社は、90分を超える手技でも外科医の疲労を最小限に抑える人間工学に基づいた器具ハンドルで対応しています。

ペット飼育率の上昇とペット保険の普及

米国では2024年に9,400万世帯がペットを飼育し、そのうち440万世帯が保険に加入しています。このような行動は、整形外科的修復、心臓インターベンション、高度歯科治療の手技件数を直接的に増加させる。一方、保険会社は、認定された器具を使用する診療所に対して払い戻しを行うことで調達に影響を与え、間接的に保険料の高い器具の購入を加速させています。ロンドン、ニューヨーク、上海のような都市は、ハイエンドの需要が密集するクラスターを形成しており、サプライヤーは、より広範な展開に先立ち、AI対応の電気手術プラットフォームを試験的に導入することができます。

先端機器の導入を阻む高コスト

プレミアム電気手術タワーは、吸煙器やバイポーラ鉗子とセットで5万米ドルを超えることもあります。保守契約、先端交換、技術者トレーニングにより、総所有コストは基本的なメスセットよりはるかに高くなり、ハイエンドの紹介病院と地方の診療所との技術格差が広がります。リース、ペイ・パー・ユース、再生品のオプションが普及しつつあるが、インド、ブラジル、東南アジアではまだ普及にばらつきがあります。

セグメント分析

縫合糸とステープラーは、2024年の売上高の33.7%を占めました。しかし、電気手術システムがCAGR 9.80%で最も急速に伸びており、2030年までに獣医用手術器具市場規模に約2億5,000万米ドルを上乗せする見込みです。獣医用手術器具市場は、人間工学に基づいて設計されたハンドルとフットスイッチの統合により、2時間の腫瘍切除手術でも疲労が少ないという利点があります。ハンドヘルドシザー、ニードルホルダー、ロンジューサーは依然として必要不可欠であるが、現在では切れ味を長持ちさせる高級スチールグレードやマイクロセレーションエッジが需要の中心となっています。

米国やオーストラリアの獣医教育病院は、犬における経カテーテル的僧帽弁修復術のような循環器科初の成果を公表しており、電気外科の臨床範囲が広がっていることを示しています。このようなエビデンスに基づき、民間のクリニックは、エントリーレベルのモノポーラ・ユニットではなく、ミッドレンジのバイポーラ・ジェネレーターを選ぶようになっています。サプライヤーはトロッカーセットとスモークエクストラクターをバンドルし、クリニックあたりの平均販売額を2024年から2025年の間に28%押し上げます。

地域分析

北米は2024年の世界売上高の38.0%を創出。AI支援画像診断の早期導入とペット保険文化により、診療所は10年に1度ではなく5~7年ごとにアップグレードできます。米国の獣医師の30%はすでに診断時に何らかの人工知能を使用しており、手術計画にフィードバックするデータ取得を増やしています。それにもかかわらず、獣医師不足は中西部や山間部の州で深刻で、症例数を増やし、複雑な処置を行う一般開業医の遠隔指導を後押ししています。

アジア太平洋はCAGR10.23%で最も急成長している地域です。中国の2025年医療機器見本市では、AIを統合した整形外科ロボットが紹介され、投資家の高精度システムに対する意欲が強まりました。インドの民間チェーン病院は、設備コストを分散させるため、サブスクリプションベースのサービス契約を試みています。地域政府は、人獣共通感染症のサーベイランスと動物病院の拡張を連携させ、第2級都市ではオートクレーブや内視鏡への助成金を開放しています。このような政策により、代理店ネットワークが拡大し、重要部品の納期が短縮されています。

欧州では、認証された器具のトレーサビリティと無菌再処理ログを要求する厳しい福祉規制が維持されています。CVSグループは、2024年のアップグレードに5,470万米ドルを投じており、この地域がトレーサビリティのあるロット番号の高性能合金に在庫を振り向けようとしていることを示しています。一方、ラテンアメリカと中東・アフリカでは、ペット飼育の増加に伴い需要が加速しています。ブラジルは手術器具の輸入をリードしており、湾岸諸国は馬の手術を優先しているため、長さの長い骨プレートや喉頭鏡の需要が高まっています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 動物における低侵襲手術の動向

- ペット飼育の増加とペット保険の普及率

- 動物疾病負担の増加と避妊去勢プログラムにより手術件数が増加

- 動物ヘルスケアにおける研究開発費の増加と製品イノベーション

- 政府の取り組みと動物福祉規制と相まって獣医ヘルスケアインフラの拡大

- クリニックの法人化により高級機器の予算が解放される

- 市場抑制要因

- 高度な外科器具と手術の高コスト

- 認定獣医師の不足

- 厳格な規制承認

- 小規模クリニックでは滅菌設備が限られているため、複雑な再利用可能な手術器具の導入が制限されています。

- 規制とテクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 縫合糸とステープラー

- ハンドヘルド機器

- メス

- 鉗子

- はさみ

- リトラクター

- 電気手術器具

- その他の製品

- トロカールとカニューラ

- 吸引と灌漑

- ハンドヘルド機器

- 動物別

- コンパニオンアニマル

- 犬

- 猫

- 農場の動物

- 牛

- 豚

- 家禽

- コンパニオンアニマル

- 用途別

- 軟部組織手術

- 歯科手術

- 整形外科

- 眼科手術

- その他の用途

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- B. Braun SE

- Medtronic

- Integra LifeSciences Corporation

- Jorgensen Laboratories

- Kshama Surgical

- Accesia AB

- GerVetUSA

- Arch Medical Solutions Company(gSource)

- Orthomed(UK)Ltd

- Johnson and Johnson

- Eickemeyer

- World Precision Instruments

- Dentalaire International

- SAI Infusion Technologies

- Granim Healthcare(DRE Veterinary)

- Amerisource Bergen Corporation

- Surgical Holdings

- Aspen Surgical Products, Inc.

- IndoSurgicals Private Limited

- Rajindra Surgical Industries

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 112 Pages

- 納期

- 2~3営業日