|

市場調査レポート

商品コード

1910497

ポリフッ化ビニリデン(PVDF):市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Polyvinylidene Fluoride (PVDF) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ポリフッ化ビニリデン(PVDF):市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

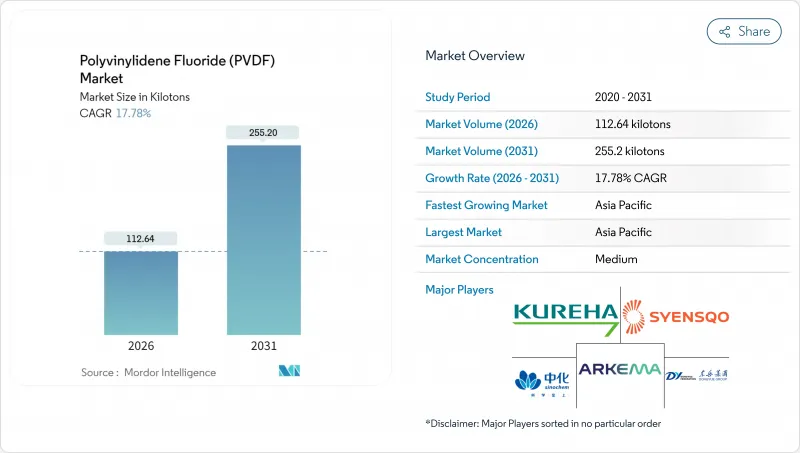

ポリフッ化ビニリデン市場は、2025年の95.64キロトンから2026年には112.64キロトンへ成長し、2026年から2031年にかけてCAGR17.78%で推移し、2031年までに255.2キロトンに達すると予測されております。

輸送手段の持続的な電動化、10ナノメートル以下のチップ向けクリーンルーム建設の加速、長寿命な建築仕上げ材を指定するインフラプロジェクトなど、これら全てが複数年にわたる需要の持続的な伸びを支えています。フッ化ビニリデンモノマーへの後方統合、電池製造拠点に近い地域での生産能力、クリーンルームシステムにおけるアプリケーションエンジニアリング支援を組み合わせたメーカーは、持続的な競争優位性を確保しています。一方、供給過剰状態にある中国のスポット市場における価格変動は、規律ある生産能力拡大と長期原料調達契約の必要性を浮き彫りにしています。特に米国による1億7,800万米ドルの助成金(北米初の世界規模プラントの基盤となる)をはじめとする政府の優遇措置は、地域別供給構造の均衡化と重要産業向けPVDFの安定供給を確保する上で、戦略的な政策支援が引き続き極めて重要であることを示しています。

世界のポリフッ化ビニリデン(PVDF)市場の動向と洞察

EVバッテリー生産の急増

自動車メーカーによる数十億米ドル規模の電動化ロードマップは、数千回の充電サイクルにわたり電極の完全性を維持する特殊バインダーの需要を直接牽引します。Syensqo社のオーガスタ複合施設は、年間500万台以上のEVバッテリーパック向けPVDFを供給します。この規模は、国内カソードバインダー供給網の基盤となる米国エネルギー省の1億7,800万米ドルの助成金によって実現可能となりました。主要セルメーカーによる垂直統合が進む中、仕様範囲が狭まり、ドイツ自動車工業会(VDA)が確認した通り、パック当たりのPVDF使用量は15~50g/kWhに増加しています。米国、欧州、インドでギガファクトリー群が拡大する中、現地生産能力を有するメーカーは輸送コスト優位性と認証取得の近接性を獲得し、地域の供給安定性を強化しています。こうした動向が相まってベースライン消費量と流通マージンを押し上げ、ポリフッ化ビニリデン市場はEV転換の主要受益者となっています。

耐薬品性コーティングへの需要

建築設計者は、色保持性、光沢安定性、チョーク抵抗性においてAAMA 2605性能基準を上回るPVDFコイルコーティングシステムへの移行を継続しています。フロリダ州、テキサス州、台風多発地域であるアジア太平洋沿岸地域では、建築基準によりこうした高品質仕上げ材の採用が義務化されつつあり、再塗装サイクルを30年に延長し、ファサードのライフサイクルコストを低減しています。産業分野でも同様の動向が見られます。化学処理業者は、強酸・強アルカリに耐えるPVDFトップコートで鋼製タンクを改修し、腐食による操業停止や規制罰則を軽減しています。インフラ刺激策法案が耐性のある公共建築物を優先する中、コーティングのバリューチェーンはマクロ景気後退シナリオにおいても安定した数量成長が見込まれ、ポリフッ化ビニリデンの市場の防御的属性を強化しています。

原料(VF2)価格の変動性

中国におけるPVDFスポット価格は、急速な生産能力拡大がリチウムイオン電池用バインダー需要を上回ったため、6ヶ月以内に下落しました。ビニリデンフッ化物の原価がPVDFの現金コストの65~70%を占めるため、このような変動はマージンを圧迫し、長期購買契約を混乱させます。欧米のコンバーターは指数連動型フォーミュラ契約でリスクを回避していますが、アジアの中堅押出メーカーは依然として影響を受けやすく、投機的な在庫積み増しにより変動性が拡大しています。供給が合理化されるまでは、調達部門は原料調達先の多様化を優先し、ポリフッ化ビニリデン市場における原料供給の安定化を図るため、委託加工契約の検討を進めるでしょう。

セグメント分析

2025年時点で、リチウムイオン電池用バインダーはポリフッ化ビニリデン市場規模の33.62%という圧倒的なシェアを占めており、2031年までCAGR31.05%で拡大が見込まれています。これは高エネルギー密度電池化学において本材料が確立した役割を反映したものです。主要自動車メーカーは次世代高ニッケル正極材にPVDFバインダーを指定しています。代替ポリマーはサイクル寿命とレート性能を損なうためです。同時に、シリコン強化負極における高充填率化によりセル当たりの消費量が増加し、基準トン数要件が倍増しています。

コーティングおよび塗料分野では、米国におけるファサード改修の加速や欧州のグリーンビルディング規制により、安定した中程度の単一桁成長が見込まれます。電線・ケーブル絶縁材は、低煙・ハロゲンフリー規格がPVCジャケットに取って代わりつつあるデータセンター電力ネットワークでシェアを拡大しています。フィルム、シート、膜は、ガス分離モジュールから強溶剤用特殊包装材に至るニッチ分野に対応し、PVDFのバリア特性がプレミアム価格設定を正当化します。パイプおよび継手は半導体・化学プロセス向けに供給され、生産量は工場拡張サイクルの影響を受けやすいもの、ポリフッ化ビニリデン市場で最高の粗利益率を誇ります。

ポリフッ化ビニリデン市場レポートは、用途別(リチウムイオン電池用バインダー、塗料・コーティング、パイプ・継手、フィルム・シートなど)、エンドユーザー産業別(航空宇宙、自動車、建築・建設、電気・電子など)、地域別(アジア太平洋、北米、欧州など)に分類されています。市場予測は、数量(トン)および金額(米ドル)で提供されます。

地域別分析

アジア太平洋地域は2025年に世界の出荷量の56.12%を占め、2031年までCAGR20.10%で成長すると予測されています。供給量の急拡大が価格変動を引き起こしたもの、顧客への近接性と規模の経済性により、アジア太平洋地域は低コスト生産の拠点としての地位を確固たるものに保っています。日本の技術優位性を強化する動きとして、クレハ株式会社がいわき工場に4億7,000万米ドル(700億円)を投じた拡張計画により、高ニッケル正極材向けに特化したグレードが供給されます。政府補助金は戦略的自立性を確保します。インドと韓国では、新興ギガファクトリー計画と家電組立産業の拡大により需要が増加し、ポリフッ化ビニリデン市場における地域的な深みを拡大しています。

北米のシェアは、リショアリング政策とインフレ抑制法(EV税額控除の全額適用には米国産電池材料の使用が義務付けられる)を背景に拡大しています。サイエンスコのオーガスタ工場は北米最大級の単一ラインPVDFプラントとなり、年間500万台のバッテリー向け現地供給を支えます。バインダーを補完する形で、アルケマ社がカルバートシティ工場で15%の生産能力増強を実施し、アリゾナ州とオハイオ州に工場を建設する半導体顧客向けに高純度グレードを確保しました。メキシコ国境地帯の製造業回廊では自動車用ハーネス向けに米国製PVDFを輸入しており、カナダのオイルサンド事業者は耐食性配管を指定するなど、複数セグメントからの需要が加わっています。

欧州では、グリーンディールによる非必須包装材でのPFAS段階的廃止が進む一方、電池・航空宇宙用途は例外として認められており、成長と規制監視のバランスが取られています。ドイツでは自動車メーカーの電池合弁事業やBASFのカソード活性材料プロジェクトが需要を支え、フランスとオランダではネットゼロ建築外皮を目指す改修プログラム向け建築用塗料の需要が牽引役となっています。同地域の厳格な環境基準は、ライフサイクル上の利点が実証されたPVDFソリューションの採用を促進する一方、コンプライアンスコストも増加させています。これにより、規制強化が進むポリフッ化ビニリデン市場において、トップクラスのサプライヤーが繁栄する二極化した状況が生じています。

南米、中東・アフリカは依然として新興市場です。ブラジルのプレソルト油田やサウジアラビアの化学下流複合施設では、総トン数は少ないものPVDFパイプが求められています。アフリカの鉱業プロジェクトでは、酸性鉱山排水処理のためのPVDF膜技術が模索されており、資源主導型経済においてこの技術の認知度を高めるニッチな成長機会を生み出しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- EV用バッテリー生産量の急増

- 耐薬品性コーティングの需要

- 半導体クリーンルーム拡張

- 石油・ガス腐食防止配管

- 航空宇宙部品の3Dプリント

- 市場抑制要因

- 原材料(VF2)価格変動性

- PFAS関連規制の監視強化

- VF2モノマー生産能力は限定されています

- バリューチェーン分析

- 規制情勢

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 新規参入業者の脅威

- 最終用途セクター動向

- 航空宇宙(航空宇宙部品生産収益)

- 自動車(自動車生産台数)

- 建築・建設(新築床面積)

- 電気・電子(電気・電子製品生産収益)

- 包装(プラスチック包装量)

第5章 市場規模と成長予測(金額ベースおよび数量ベース)

- 用途別

- リチウムイオン電池用バインダー

- コーティング・塗料

- パイプ・継手

- フィルム・シート

- 電線・ケーブル絶縁材

- その他(膜など)

- エンドユーザー産業別

- 航空宇宙産業

- 自動車

- 建築・建設

- 電気・電子機器

- 産業・機械

- 包装

- その他のエンドユーザー産業

- 地域別

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- マレーシア

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- イタリア

- 英国

- ロシア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- ナイジェリア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/ランキング分析

- 企業プロファイル

- Arkema

- Dongyue Group

- Gujarat Fluorochemicals Limited

- Hubei Everflon Polymer Co., Ltd.

- Kureha Corporation

- RTP Company

- Sinochem

- Syensqo

- Zhejiang Juhua Co., Ltd.

- ZheJiang Yonghe Refrigerant Co.,Ltd