|

市場調査レポート

商品コード

1445936

防塵システム・化学抑制剤: 市場シェア分析、業界動向と統計、成長予測(2024~2029年)Dust Control Systems And Suppression Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 防塵システム・化学抑制剤: 市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 150 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

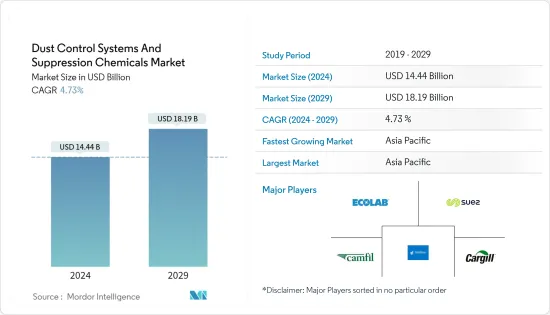

防塵システム・化学抑制剤の市場規模は、2024年に144億4,000万米ドルと推定され、2029年までに181億9,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に4.73%のCAGRで成長します。

COVID-19のパンデミックは市場に悪影響を及ぼしました。ただし、市場はパンデミック前のレベルに達しており、予測期間中に着実に成長すると予想されます。

主なハイライト

- 短期的には、市場の成長を牽引する主な要因は、アジア太平洋における建設とインフラの成長と、規制遵守の強化です。

- 食品および医薬品業界における集塵の問題は、市場の成長を妨げると予想されます。

- アジア太平洋が世界中の市場を独占しており、最大の消費は中国とインドから来ています。

防塵システム・化学抑制剤の市場動向

建設業界が市場を独占する

- 粉塵対策は、情勢や空気中を移動する粉塵による大気汚染や水質汚染の可能性がある建設現場に適用できます。

- HSE統計(英国政府の安全衛生行政統計)によると、毎年、世界中で500人以上の建設作業員がシリカ粉塵への曝露により死亡しています。したがって、有害な粉塵の排出を規制することが重要となり、ここ数年で防塵システム・化学抑制剤に対する大きな需要が生まれました。

- 従来のプロセスと比較して、粉塵抑制ソリューションは、施工が簡単で、極端な気候条件下でも長寿命で保護できるなど、建設用途に明確な利点と大きな利益をもたらします。

- 現在、建設現場や主要幹線道路、高速道路から輸送道路、工業用道路、田舎道、駐機場、ハードスタンドに至るまで、あらゆる種類の道路でさまざまな粉塵制御問題を解決できる最先端の粉塵制御ソリューションが存在します。

- 塩化カルシウムは、建設業界で使用される主要な粉塵抑制抑制化学物質です。さらに、建設業界では、運搬道路やアクセス道路を安定させるためにポリマーエマルジョンが使用されています。

- 米国は、 760万人を超える従業員を雇用する巨大な建設部門を誇っています。米国国勢調査局によると、2022年の建設額は1兆7,929億米ドルで、2021年の1兆6,264億米ドルと比べて10.2%増加しました。

- さらに、米国国勢調査局が作成したさらなる統計によると、米国の年間新築建設額は、2021年の1兆4,998億2,200万米ドルに対し、2022年には1兆6,575億9,000万米ドルとなっています。さらに、米国の年間住宅建設は、国内で実施された非住宅建設の年間価値は、2021年の7,591億7,700万米ドルと比較して、2022年には8,084億2,700万米ドルとなり、これにより、2021年の7,406億4,500万米ドルと比較して、2022年の非住宅建設の価値は8,491億6,400万米ドルとなった。市場の消費を短期的に調査します。

- さらに、アジア太平洋地域における外国企業の存在感の増大により、新しいオフィス、ビル、生産ハウスなどの需要が生まれ、この地域の建設部門を牽引しています。

- こうした要因により、建設業界が市場を独占する可能性が高いです。

中国がアジア太平洋市場を独占へ

- 中国の建設業界は恒大債務危機を経験しており、今後しばらくは衰退すると予想されています。

- 同国は、主に環境への懸念と気候目標を理由に、過去数年間石炭消費量の削減に注力してきました。

- 国内生産量の減少による石炭輸入の増加を受けて、政府はこの措置を講じた。

- 同国で承認された新規炭鉱は、石炭専用生産基地での産出量の統合を目指す国家戦略に支えられ、新疆、内モンゴル、山西省、陝西省の地域にあります。

- これらの新しい鉱山は、既存の炭鉱の拡張のために計画されています。この国では、このような新しい鉱山の開発および運営のため、防塵システム・化学抑制剤に対する高い需要が見込まれています。

- この国の人口動態は住宅や商業建設活動に有利になると予想されます。人口の増加により、官民セクターによる手頃な価格の住宅コロニーへの投資が活発化しています。中国政府は率先して40の主要都市に、約1,300万人が居住できると想定される650万戸の政府補助付き賃貸住宅を贈呈しました。

- さらに、中国政府は大規模な建設計画を展開しており、これには今後10年間で2億5,000万人の農村住民が新たな大都市に移動するための準備が含まれており、建設中のさまざまな用途に将来使用される建設資材の大きな範囲が生まれています。建物の特性を高める活動。香港の住宅当局は、低コスト住宅の建設開始を促進するためのいくつかの措置を開始しました。政府当局は、2030年までの10年間に30万1,000戸の公営住宅を供給することを目標としています。これらの要因により国内の建設業界が成長すると予想され、それによって将来調査される市場の需要を下支えする可能性が高いです。

- したがって、さまざまなエンドユーザー産業の成長により、さまざまな用途向けの防塵システム・化学抑制剤の需要が高まっています。

防塵システム・化学抑制剤業界の概要

粉塵抑制化学薬品市場は、非常に少数のプレーヤーの間で部分的に統合されています。粉塵抑制システム市場における他の著名なプレーヤーには、Cargill Incorporated、SUEZ、Ecolab、Camfil、Donaldson Company Inc.などがあります(順不同)。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- アジア太平洋における建設とインフラの成長

- 規制遵守の増加

- その他の 促進要因

- 抑制要因

- 食品および製薬業界における集塵の問題

- その他の抑制要因

- 業界のバリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替製品やサービスの脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション(金額ベースの市場規模)

- 化学タイプ

- リグニンスルホン酸塩

- 塩化カルシウム

- 塩化マグネシウム

- アスファルト乳剤

- 油乳剤

- ポリマーエマルション

- その他

- システムタイプ

- 乾式コレクション

- 湿式サプレッション

- エンドユーザー産業

- 鉱業

- 建設

- 食品・飲料

- 石油・ガス、石油化学

- 医薬品

- その他

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東とアフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- 合併と買収、合弁事業、コラボレーション、および契約

- 市場シェア(%)/ランキング分析

- 有力企業が採用した戦略

- 企業プロファイル

- Chemical Providers

- ADM

- Benetech Inc.

- Borregaard

- Cargill Incorporated

- Chemtex Speciality Limited

- Evonik Industries AG

- GelTech Solutions

- Hexion

- Quaker Houghton(Quaker Chemical Corporation)

- Shaw Almex Industries Ltd

- SUEZ

- Ecolab

- System Providers

- BossTek

- Camfil

- CW Machine Worx

- Donaldson Company Inc.

- DSH Systems Ltd

- Duztech AB

- Nederman Holding AB

- SLY Inc.

- The ACT Group

- Chemical Providers

第7章 市場機会と将来の動向

The Dust Control Systems And Suppression Chemicals Market size is estimated at USD 14.44 billion in 2024, and is expected to reach USD 18.19 billion by 2029, growing at a CAGR of 4.73% during the forecast period (2024-2029).

The COVID-19 pandemic negatively impacted the market. However, the market is reaching pre-pandemic levels and is expected to grow steadily during the forecast period.

Key Highlights

- Over the short term, the major factors driving the growth of the market are the growth in construction and infrastructure in Asia-Pacific and the increasing regulatory compliances.

- Dust collection problems in the food and pharmaceutical industry are expected to hinder the market's growth.

- Asia-Pacific dominated the market worldwide, with the largest consumption coming from China and India.

Dust Control Systems & Suppression Chemicals Market Trends

Construction Industry to Dominate the Market

- Dust control measures are applicable to any construction site with potential air and water pollution from dust traveling across the landscape or through the air.

- According to HSE statistics (the U.K. government's Health and Safety Executive statistics), every year, more than 500 construction workers die from exposure to silica dust worldwide. Hence, it became important to regulate hazardous dust emissions, creating a significant demand for dust control systems and suppression chemicals over the last few years.

- Compared to conventional processes, dust suppression solutions offer distinct advantages and lucrative benefits for construction applications, including easy application and long-life protection during extreme climatic conditions.

- Currently, there are state-of-the-art dust control solutions that can solve a range of dust control problems at construction sites and on all types of roads, from major highways and freeways to haulage, industrial, and rural roads, tarmacs, hardstand areas, and water-repellent pavements.

- Calcium chloride is the major dust control suppression chemical used in the construction industry. In addition, the construction industry uses polymer emulsions for stabilizing haul and access roads.

- The United States boasts a colossal construction sector that employs over 7.6 million employees. According to U.S. Census Bureau, in 2022, the value of construction was USD 1,792.9 billion, a 10.2% increase over the USD 1,626.4 billion spent in 2021.

- Further, as per further statistics generated by the U.S. Census Bureau, the annual value for new construction in the United States accounted for USD 1,657,590 million in 2022, compared to USD 1,499,822 million in 2021. Moreover, the annual residential construction in the United States was valued at USD 849,164 million in 2022, compared to USD 740,645 million in 2021. The annual value of non-residential construction put in place in the country was valued at USD 808,427 million in 2022, compared to USD 759,177 million in 2021, thereby decreasing the consumption of the market studied in the short term.

- Moreover, the increasing presence of foreign companies in the Asia-Pacific region has created a demand for new offices, buildings, production houses, etc., thereby driving the construction sector in the region.

- Such factors are likely to help the construction industry dominate the market.

China to Dominate the Asia-Pacific Market

- China's construction industry has been going through the Evergrande debt crisis, and it is expected to decline for a short while in the future.

- The country has been focusing on reducing coal consumption for the past few years, mainly due to environmental concerns and climate goals.

- The government took this step in accordance with the growing coal imports of the country due to the reduction in domestic production.

- The new coal mines approved in the country are located in the regions of Xinjiang, Inner Mongolia, Shanxi, and Shaanxi, supported by the national strategy toward consolidating the output at dedicated coal production bases.

- These new mines are planned for the expansion of the existing collieries. The country is expected to witness high demand for dust control systems and suppression chemicals for developing and operating such new mines.

- The country's demographics are expected to favor housing and commercial construction activities. The growing population has triggered investments in affordable residential colonies by the public and private sectors. China's government has taken the initiative to gift 40 key cities with 6.5 million government-subsidized rental homes that are supposed to accommodate around 13 million people.

- Additionally, the Chinese government has rolled out massive construction plans, which include making provisions for the movement of 250 million rural people to its new megacities over the next ten years, creating a major scope for construction materials used in the future in various applications during construction activities to enhance the building properties. The housing authorities of Hong Kong launched several measures to push start the construction of low-cost housing. The officials aim to provide 301,000 public housing units in 10 years till 2030. These factors are expected to raise the construction industry in the country and thereby are likely to support the demand for the market studied in the future.

- Thus, growth in various end-user industries is boosting the demand for dust control systems and suppression chemicals for various applications.

Dust Control Systems & Suppression Chemicals Industry Overview

The dust suppression chemicals market is partially consolidated among very few players. Some of the other prominent players in the dust suppression systems market include Cargill Incorporated, SUEZ, Ecolab, Camfil, and Donaldson Company Inc. (not in any particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growth in Construction and Infrastructure in Asia-Pacific

- 4.1.2 Increase in Regulatory Compliances

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Dust Collection Problems in Food and Pharmaceutical Industry

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Chemical Type

- 5.1.1 Lignin Sulfonate

- 5.1.2 Calcium Chloride

- 5.1.3 Magnesium Chloride

- 5.1.4 Asphalt Emulsions

- 5.1.5 Oil Emulsions

- 5.1.6 Polymeric Emulsions

- 5.1.7 Other Chemical Types

- 5.2 System Type

- 5.2.1 Dry Collection

- 5.2.2 Wet Suppression

- 5.3 End-user Industry

- 5.3.1 Mining

- 5.3.2 Construction

- 5.3.3 Food and Beverage

- 5.3.4 Oil and Gas and Petrochemical

- 5.3.5 Pharmaceutical

- 5.3.6 Other End-user Industries

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Chemical Providers

- 6.4.1.1 ADM

- 6.4.1.2 Benetech Inc.

- 6.4.1.3 Borregaard

- 6.4.1.4 Cargill Incorporated

- 6.4.1.5 Chemtex Speciality Limited

- 6.4.1.6 Evonik Industries AG

- 6.4.1.7 GelTech Solutions

- 6.4.1.8 Hexion

- 6.4.1.9 Quaker Houghton (Quaker Chemical Corporation)

- 6.4.1.10 Shaw Almex Industries Ltd

- 6.4.1.11 SUEZ

- 6.4.1.12 Ecolab

- 6.4.2 System Providers

- 6.4.2.1 BossTek

- 6.4.2.2 Camfil

- 6.4.2.3 CW Machine Worx

- 6.4.2.4 Donaldson Company Inc.

- 6.4.2.5 DSH Systems Ltd

- 6.4.2.6 Duztech AB

- 6.4.2.7 Nederman Holding AB

- 6.4.2.8 SLY Inc.

- 6.4.2.9 The ACT Group

- 6.4.1 Chemical Providers

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Investments in the Chemical Sector

- 7.2 Emergence of Green Products for Dust Control