|

市場調査レポート

商品コード

1851596

グラファイト:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Graphite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| グラファイト:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年07月01日

発行: Mordor Intelligence

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

概要

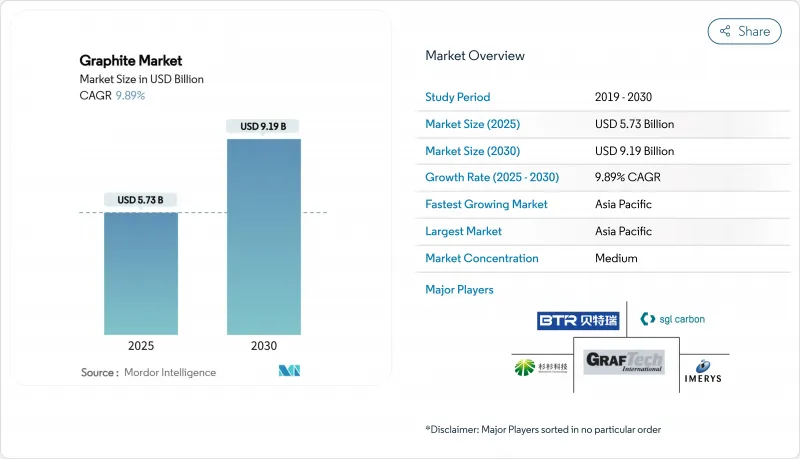

グラファイト市場規模は2025年に57億3,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは9.89%で、2030年には91億9,000万米ドルに達すると予測されます。

旺盛なバッテリー需要、鉄鋼製造の構造転換、重要素材のサプライチェーンを現地化する取り組みの強化が、この軌道を総体的に支えています。グラファイト産業は、バルク商品部門から、モビリティ、電力、重工業の脱炭素化を支える戦略的材料分野への決定的な転換を経験しています。アジア太平洋における天然資源の集中、北米と欧州における政策的インセンティブが、採掘、加工、リサイクル資産への新たな投資を促進しています。同時に、資本コストの上昇と環境規制の強化が、責任ある調達を確保しながらリスクを分散する合弁事業を後押ししています。新たな推論として、契約形態が長期化し、現在では10年以上にわたるオフテイク契約が定期的に結ばれていることが挙げられます。

世界のグラファイト市場の動向と洞察

リチウムイオン電池業界の需要拡大

現在、グラファイトの市場シェアは電池メーカーが最も大きく、このセグメントのCAGRは17%以上となっており、10年を通じて持続的に加速することを示しています。電気自動車(EV)ブランド間の価格競争の激化は、アノードのコスト感応度を高め、合成代替品よりもトン当たり数千ドルの優位性を提供する天然グラファイトへの嗜好を傾けています。合成品の製造には3,000℃の温度が必要なのに対し、天然品の精製は通常1,800℃以下で行われるためです。最近の入札データから読み取れる推論としては、自動車メーカー各社が、天然素材のESGプロファイルの向上と引き換えに、ファーストサイクル効率の若干の低下を容認していることがあげられます。

アジアと中東における鉄鋼生産の増加

排出削減を目的とした電気アーク炉(EAF)へのシフトは、超高出力グラファイト電極の需要を大幅に引き上げています。機械と自動車用途が鉄鋼消費量の大きな割合を占めるようになり、電極の耐久性と導電性の要求が暗黙のうちに高まっています。電極の純度、タップ・ツー・タップ時間、炉全体のエネルギー効率には直接的な関連があるため、電極サプライヤーは硫黄と窒素の含有量が低いことを証明し、プレミアム価格を実現することができます。

厳しい環境規制

炭素価格規制とScope-3開示の枠組みは、生産者に再生可能電力の採用を促し、米国エネルギー省が開発した低温触媒グラファイト化を試験的に導入することを促しています。

セグメント分析

天然グラファイトは、2024年には合成グラファイトが市場の58.09%を占め、現在優勢であるにもかかわらず、急速にシェアを拡大しています。マイクロ波加熱と組み合わせた苛性ベーキングのような新鮮な精製プロセスは、現在99.95%の純度を提供し、過去の性能差を縮めています。明確な推論としては、現在OEMの購買ダッシュボードに掲載されているライフサイクル・アセスメント・データが、たとえ直接的なセルレベルのエネルギー密度が僅かに低くても、調達方針を天然グラファイトに傾けているということです。

バイオマス由来の合成グラファイトは、採掘された天然グラファイトや石油ニードルコークスへの依存を減らすことができるため、供給安全性への懸念が高まっています。リグニンベースの前駆体から、リチウムのインターカレーションに適した層間間隔を持つターボストラティックカーボンが得られることが、パイロットスタディで確認されました。新たな推論としては、天然フレークとバイオグラファイトの二重調達戦略が、地政学的混乱と炭素価格高騰に対する魅力的なヘッジとして浮上しています。

地域分析

アジア太平洋地域のグラファイト市場シェアは現在55.42%で、CAGRは11%以上と最も速いです。中国の優位性は、フレーク状グラファイト鉱山、精製ライン、球状化プラントを単一の物流通路に統合したクラスターに起因します。インドネシアやマレーシアのようなASEAN諸国は、中国のクラスター・モデルを模倣し、バリュー・チェーンの代替ノードを作ることを期待して、中流加工業者を誘致しているというのが、新たな推論です。

北米は、輸入に依存する消費者ベースから新興生産者ベースへと移行しつつあるが、これはインフレ削減法の税額控除(適格陽極部品コストの10%を払い戻す)によって助けられています。欧州のグラファイト産業は、資源の供給よりもむしろ規制のリーダーシップによって形成されています。バッテリーにおけるリサイクル含有量の最低基準値の義務化により、ギガファクトリーはリサイクル業者と複数年にわたる供給契約を締結することになります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- リチウムイオン電池産業の需要拡大

- アジアと中東における鉄鋼生産の増加

- グラファイト自然循環型社会への取り組みの増加

- エレクトロニクス産業における導電性グラファイトの需要拡大

- 航空宇宙・防衛産業からの需要増加

- 市場抑制要因

- 厳しい環境規制

- 高品質の天然黒鉛の限られた供給

- 原材料価格の変動

- バリューチェーン分析

- 規制と環境の展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場規模と成長予測

- タイプ別

- 天然グラファイト

- 合成グラファイト

- 用途別

- 電極

- 耐火物、鋳造およびファウンダリ

- バッテリー

- 潤滑油

- その他の用途(放熱材料、摩擦材、ブレーキライニングなど)

- エンドユーザー業界別

- 冶金

- 電子部品

- 自動車

- その他の産業(エネルギー、航空宇宙・防衛など)

- 地域別

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- ロシア

- その他欧州地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- アジア太平洋地域

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア(%)/ランキング分析

- 企業プロファイル

- Asbury Carbons

- BTR New Material Group Co., Ltd.

- GrafTech International

- Graphit Kropfmuhl GmbH

- Imerys

- Mason Resources Inc.

- Mersen

- Nippon Kokuen Group

- Northern Graphite

- POCO

- Resonac Holdings Corporation

- SGL Carbon

- Shanghai Shanshan Technology Co., Ltd.

- Syrah Resources Limited

- Tokai Carbon Co., Ltd.

- Triton Minerals Limited