|

市場調査レポート

商品コード

1445868

ガスエンジン: 市場シェア分析、業界動向と統計、成長予測(2024~2029年)Gas Engine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ガスエンジン: 市場シェア分析、業界動向と統計、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 95 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

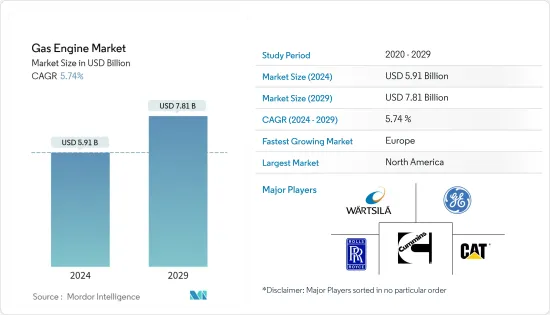

ガスエンジン市場規模は2024年に59億1,000万米ドルと推定され、2029年までに78億1,000万米ドルに達すると予測されており、予測期間(2024年から2029年)中に5.74%のCAGRで成長します。

主なハイライト

- 中期的には、ガスエンジン市場は世界レベルでの天然ガスの供給量が多いことと、発電および自動車分野での排出ガスのない燃料システムの需要によって主に動かされています。

- 一方で、再生可能エネルギー源への傾向の高まりにより、ガスエンジンの将来の繁栄は妨げられています。

- それにもかかわらず、より優れたバージョンのガスエンジンを生産するための技術の進歩により、市場開発の十分な機会が生まれています。最近、ドイツの企業MAN Energy Solutions Enginesは、ニュルンベルクで開催されたバイオガスコンベンション&トレードフェアで、新しいMAN E3872ガスエンジンシリーズを初めて発表しました。このエンジンは、排気量29.6リットル、ボア 138 mm、ストローク 165 mmの4ストローク火花点火ガスエンジンとして設計されています。わずか12個のシリンダーで効率が44%向上しました。

ガスエンジン市場動向

大幅な成長が期待される電力ユーティリティ

- 電力ユーティリティは、基本的な電力負荷に供給するためにガスエンジンを好みます。さらに、ガスエンジン発電機の使用は、ピーク負荷需要に対処するために非常に有用であると考えられています。世界中のいくつかの電力ユーティリティは、特に朝と夕方の時間帯におけるピーク負荷需要の急激な急増に直面しています。

- 天然ガスベースの発電は、世界の発電構成において石炭に次いで第2位にあります。 2022年の発電量は6631.39TWhを記録し、総発電量の約23%を占めました。ガスベースのエンジンがこれほど大規模に導入された理由で最も注目されたのは、電力部門の脱炭素化でした。多くのガス発電プロジェクトが世界の発電ポートフォリオに追加される途上にあります。

- Global Energy Monitorによると、2022年の時点で世界中で600ギガワットを超える天然ガス発電所が開発段階にあり、そのうち160ギガワットがすでに建設されています。

- 2022年 1月に、ワルチラは、インドのチェンナイにある15.5 MW自家発電所向けに、タミルナドゥペトロプロダクツリミテッド(TPL)から2台の34SGガスエンジンを受注すると発表しました。

- 2023年 10月、済能(舟山)ガス発電有限公司は、ハルビン電力公司と協力してGE Vernovaに9HA.02コンバインドサイクルガスタービン2基を発注しました。中国の国営電力ユーティリティ済能(舟山)ガス発電有限公司は、同諸島最大の島である舟山市で新たなコンバインドサイクル発電所の建設を開始すると発表しました。この発電所は2025年末までに運転開始予定で、舟山市に合計 1.7ギガワット(GW)近くの電力を供給することが見込まれています。 9HA.02 DLN2.6e燃焼システムは、体積比で最大50%の水素で動作するように設計されており、最大10%の水素で動作するというプラントの当初の目標を大幅に上回っています。

- このような種類の開発により、電力事業セグメントは、予測期間中にガスエンジンシステムのすべてのアプリケーションの中で大きなシェアを占めると予想されます。

大幅な成長が期待される欧州

- 欧州地域には、さまざまな用途でガスエンジンを大量に導入できる最大の可能性があります。よりグリーンなエネルギーへの移行を目指す政府の政策は、水素および天然ガスベースの技術が排出ガスのない環境を実現するため、市場の成長の触媒として機能します。

- さらに、この地域における業界をリードする企業の存在により、ガスエンジン産業のさらなる技術的成長が推進されています。多くの企業が、新しい用途向けに、より多用途性を備えた、より優れたガスエンジンシステムを発表しています。

- 2023年 4月、クラークエナジーは、イミンガムエネルギーハブにあるVPIの拡張施設に50MWの水素対応INNIO Jenbacherガスエンジンを納入する注文を受け取りました。 Clarke Energyが設置した50MWガス往復ピーキング設備は来年初めに運転開始予定であり、299MWオープンサイクルガスタービン(OCGT)は2025年夏までに運転開始予定であり、エネルギーの成功に不可欠な容量に対するVPIの投資を表しています。

- 2023年1月、ロールスロイスは、100%水素燃料で動作するmtuシリーズ4000 L64エンジンの12気筒ガスバージョンのテストに成功したと発表しました。パワーシステム事業部門が実施したテストでは、エンジンは効率、性能、排出ガス、燃焼の点で優れた特性を示したと同社は述べています。

- このような発展により、予測期間中に欧州地域が市場のエースになると予想されます。

ガスエンジン業界の概要

ガスエンジン市場は半統合されています。この市場の主要企業には、ゼネラル・エレクトリック・カンパニー、ワルチラ・オイジ・アブプ、ロールス・ロイス・ホールディングスPLC、キャタピラー社、カミンズ社などが含まれます(順不同)。

カミンズ社は、自社製品用のエンジンを製造するOEMだけでなく、さまざまな独立系エンジンメーカーや発電機セット組立業者との健全な競合に参加すると主張しています。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3か月のアナリストサポート

目次

第1章 イントロダクション

- 調査範囲

- 市場の定義

- 調査の前提条件

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場概要

- イントロダクション

- 2028年までの市場規模と需要予測(10億米ドル)

- 最近の動向と発展

- 政府の政策と規制

- 市場力学

- 促進要因

- さまざまなエンドユーザー業界におけるガスベースのシステム供給・消費の増加

- 世界の排ガス規制強化の実施

- 抑制要因

- 再生可能資源への関心の高まり

- 促進要因

- サプライチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の激しさ

第5章 市場セグメンテーション

- エンドユーザー

- 電力ユーティリティ

- 自動車

- 船舶

- 産業

- その他

- 燃料タイプ

- 天然ガス

- 水素

- その他

- 地域

- 北米

- 米国

- カナダ

- その他北米

- 欧州

- ドイツ

- フランス

- 英国

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東とアフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- その他中東とアフリカ

- 北米

第6章 競合情勢

- 合併と買収、合弁事業、コラボレーション、および契約

- 有力企業が採用した戦略

- 企業プロファイル

- Caterpillar Inc.

- Cummins Inc.

- Siemens AG

- Rolls-Royce Holdings PLC

- Wartsila Oyj Abp

- Mitsubishi Heavy Industries Ltd

- Hyundai Heavy Industries Co. Ltd

- Man SE

- General Electric Company

- Kawasaki Heavy Industries Ltd

- JFE Engineering Corporation

- Liebherr Group

第7章 市場機会と将来の動向

The Gas Engine Market size is estimated at USD 5.91 billion in 2024, and is expected to reach USD 7.81 billion by 2029, growing at a CAGR of 5.74% during the forecast period (2024-2029).

Key Highlights

- Over the medium term, the gas engine market is largely driven by high natural gas supply at the global level and the demand for the emissions-free fuel system in the power generation and automotive sector.

- On the other hand, the thriving future of gas engines is thwarted by the growing inclination towards renewable sources of energy.

- Nevertheless, the technical advancements to produce the better versions of gas engines create ample opportunities for market development. Recently, the German company MAN Energy Solutions Engines introduced a new MAN E3872 gas-engine series for the first time at Biogas Convention & Trade Fair in Nuremberg. It is designed as a four-stroke spark-ignition gas engine with a displacement of 29.6 liters, a bore of 138mm, and a stroke of 165mm. It has 44% greater efficiency from just 12 cylinders.

Gas Engine Market Trends

Power Utilities Expected to Witness Significant Growth

- Electric Utilities prefer gas engines to serve base electrical loads. In addition, the use of gas engine generators is also considered highly useful for handling peak load demand. Several utilities worldwide have faced a rapid spike in the peak load demand, especially during the morning and evening time periods.

- Natural gas-based power generation stands at second place in the global electricity generation mix, after coal. The output was recorded as 6631.39 TWh in 2022, making around 23% of total power generation. The most highlighted reason for such a huge deployment of gas-based engines was the decarbonization of the power sector. Many gas-to-power projects are still on the way to be added to the global power generation portfolio.

- According to global energy monitor, over 600 gigawatts of natural gas power plants are in the development stage worldwide as of 2022, of which 160 gigawatts have already been constructed.

- In Nomeber 2022, Wartsila announced to receive order for two 34SG gas engines by the Tamilnadu Petroproducts Limited (TPL) for 15.5 MW captive power plant in Chennai, India.

- In October 2023, Jineng (Zhoushan) Gas Power Generation Co. placed an order with GE Vernova for two of its 9HA.02 combined-cycle gas turbines in collaboration with Harbin Electric Corporation. China's state-owned utility Jineng (Zhoushan) Gas Power Generation Co. announced starting construction of a new combined-cycle power plant on Zhoushan, the archipelago's largest island. Scheduled to begin operations by the end of 2025, the plant is expected to deliver a total of nearly 1.7 gigawatts (GW) of electricity for Zhoushan. The 9HA.02 DLN2.6e combustion system is designed to operate on up to 50% hydrogen by volume, well above the plant's initial goal to operate on up to 10% hydrogen.

- Owing to such kind of developments, the power utility segment is expected to have a significant share among all the applications of gas engine systems during the forecast period.

Europe Expected to Have a Significant Growth

- The European region has the maximum potential to allow high deployment of gas engines in various applications. The government policies to have a greener energy transition act as a catalyst for the growth of the market, as hydrogen and natural-gas-based technologies render an emission-free environment.

- Furthermore, the presence of industry-leading companies in the region propels a higher techno-growth of the gas engine industry. Many companies have come out with better gas engine systems with more versatility for new applications.

- In April 2023, Clarke Energy recieved order to deliver 50MW of hydrogen ready INNIO Jenbacher gas engines to VPI's expansion at Immingham energy hub. A 50MW gas reciprocating peaking facility installed by Clarke Energy, scheduled to begin operation early next year, and a 299MW open cycle gas turbine (OCGT), scheduled to begin operation by summer 2025, represent VPI's investment in capacity essential to the success of the energy transition.

- In January 2023, Rolls-Royce announced that it had conducted successful tests of a 12-cylinder gas variant of the mtu Series 4000 L64 engine running on 100% hydrogen fuel. In the tests carried out by the Power Systems business unit, the company stated that the engine showed excellent characteristics in terms of efficiency, performance, emissions, and combustion.

- Owing to such developments, the European region is expected to ace the market during the forecast period.

Gas Engine Industry Overview

The gas engine market is semi-consolidated. The key players in this market include (in not particula order) General Electric Company, Wartsila Oyj Abp, Rolls-Royce Holdings PLC, Caterpillar Inc., and Cummins Inc., among others.

Cummins Inc claims to participate in healthy competition with a variety of independent engine manufacturers and generator set assemblers as well as OEMs who manufacture engines for their own products. Some of the company's major competitors in the region include CAT, MTU (Rolls Royce Power Systems Group) and Kohler/SDMO (Kohler Group), Generac, Mitsubishi Heavy Industries (MHI), etc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

- 4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.1.1 Increasing Supply and Consumption of Gas-based Systems in Various End-user Industry

- 4.5.1.2 Implementation of stricter emission regulations worldwide

- 4.5.2 Restraints

- 4.5.2.1 Growing Inclination towards Renewable Sources

- 4.5.1 Drivers

- 4.6 Supply Chain Analysis

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 End-User

- 5.1.1 Power Utilities

- 5.1.2 Automotive

- 5.1.3 Marine

- 5.1.4 Industrial

- 5.1.5 Others

- 5.2 Fuel Type

- 5.2.1 Natural Gas

- 5.2.2 Hydrogen

- 5.2.3 Other Fuel Types

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Company Profiles

- 6.3.1 Caterpillar Inc.

- 6.3.2 Cummins Inc.

- 6.3.3 Siemens AG

- 6.3.4 Rolls-Royce Holdings PLC

- 6.3.5 Wartsila Oyj Abp

- 6.3.6 Mitsubishi Heavy Industries Ltd

- 6.3.7 Hyundai Heavy Industries Co. Ltd

- 6.3.8 Man SE

- 6.3.9 General Electric Company

- 6.3.10 Kawasaki Heavy Industries Ltd

- 6.3.11 JFE Engineering Corporation

- 6.3.12 Liebherr Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 The Technical Advancements to Produce the Better Versions of Gas Engines