|

市場調査レポート

商品コード

1850128

農業用接種剤:市場シェア分析、産業動向、統計、成長予測(2025年~2030年)Agricultural Inoculants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 農業用接種剤:市場シェア分析、産業動向、統計、成長予測(2025年~2030年) |

|

出版日: 2025年06月29日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

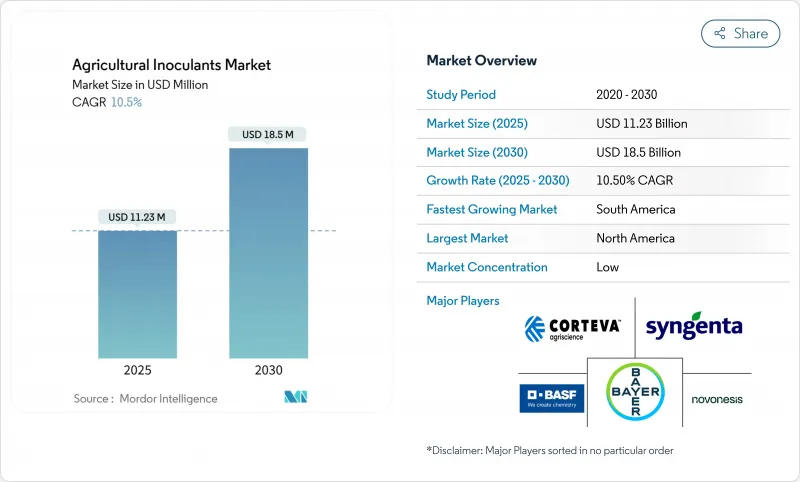

農業用接種剤市場は、2025年に112億3,000万米ドルと評価され、CAGR 10.5%を反映して2030年には185億米ドルに達すると予測されています。

合成肥料の排出を抑制するための政策圧力の高まり、生物学的窒素固定に報いる炭素クレジットのインセンティブ強化、厳格化する有機基準に適合した残留物のない食品に対する小売需要の高まりなどです。この分野は、農家が測定可能な収量の安定と土壌の健全性の向上を認識するにつれて、ニッチな生物学的投入物から作物管理ツールの主流へと移行しました。サプライヤーは、持続可能性目標に沿ったプレミアムな複数菌株配合によって魅力的なマージンを獲得し、同時に生産者の養分コストを引き下げています。主な資本流入が上昇傾向を強めています。微生物カプセル化とAI誘導型施用システムにおけるベンチャー企業の資金調達は急速に拡大しており、新興企業は差別化された技術を商業化するためのリソースを得ています。同時に、既存企業は微生物の生存期間を延長し、農場での使用を簡素化する次世代デリバリー方法の研究開発を加速させています。この革新と統合の二重の軌道は、価値がコモディティな単一菌株製品から、検証可能な農学的成果をもたらす統合生物学的プラットフォームへと移行するにつれて、市場が継続的に拡大する態勢にあることを示唆しています。

世界の農業用接種剤市場動向と洞察

有機認証基準へのシフト

小売業者と消費者は現在、残留農薬のない農産物を求めており、厳格な有機基準を満たす投入資材の大きな市場を形成しています。EUのFarm to Fork戦略は、2030年までに化学農薬の使用量を50%削減することを目標としており、EU全域で微生物の採用を加速させました。米国農務省(USDA)の全米有機プログラム規則が更新され、許容可能な微生物生産慣行が明確化されたことで、買い手の不確実性が軽減され、サプライヤーの投資が支援されました。20%から40%の有機価格プレミアムは、生物学的接種剤の高い初期費用を正当化します。とはいえ、専門的な保管・取り扱いインフラを持たない小規模生産者は、サプライチェーン全体で認証を維持する上でハードルに直面しています。

耕地面積の縮小と食糧安全保障への圧力

世界の1人当たり耕地面積は、1970年の0.38ヘクタールから2020年には0.19ヘクタールに減少し、土地の拡大よりも収量強化に焦点が絞られるようになりました。アジア太平洋では、急速な都市化がこの圧力を増幅させています。圃場研究によれば、微生物接種剤は栄養循環と土壌構造を改善することにより、低生産性土壌でも収量を4.8~6.2%向上させることができます。土地価格が1ヘクタール当たり1万米ドルを超える地域では、生物学的インプットは費用対効果の高い増収経路を提供します。エネルギー市場の逼迫により合成肥料の価格が不安定なままであるため、このメリットはますます大きくなります。

農家の認識ギャップと農場での取り扱いの複雑さ

多くの農家は、微生物の貯蔵、生存性試験、施用時期に関するトレーニングを受けていないです。普及指導員は肥料や農薬に重点を置いていることが多く、生物学的肥料については知識のギャップがあります。その結果、製品の誤った取り扱いが、一貫性のないパフォーマンスや懐疑的な見方を招いています。根粒から根粒菌を増殖させるブラジルの「結節破砕」技術は、草の根技術革新が普及のギャップを埋め、導入の障壁を低くできることを示しています。

セグメント分析

作物栄養アプリケーションは、窒素固定およびリン可溶化微生物が合成肥料の一部を置き換えるため、2024年の収益の52%を占めました。肥料コストの上昇が生物学的代替を促すため、栄養分野の農業用接種剤市場規模は着実に拡大すると予測されます。農家は、収量を維持しながら窒素投入量を15~25%節約できるとしており、これは投資回収期間の短縮につながります。

作物保護生物学的製剤は、その貢献度は低いもの、2030年までのCAGRは10.9%となります。化学農薬に対する規制の取り締まりと、主要病原菌の耐性問題の急増が需要を加速しています。企業は現在、微生物保護剤と栄養株をバンドルし、土壌から葉までを総合的にカバーすることを約束しています。この収束は、単体の栄養剤メーカーにポートフォリオを広げるか、統合された製品にシェアを奪われるリスクを迫るものです。

2024年の農業用接種剤市場シェアは細菌が71%を占め、これは数十年にわたるマメ科植物での根粒菌の成功と穀類での使用の拡大を反映しています。このリーダーシップは、十分に立証された有効性、低コスト、規制当局の間でのなじみの深さによるものです。

菌類は最も急速に成長しているグループであり、2030年までのCAGRは11.5%と予測されています。トリコデルマ菌と菌根菌は、病害の抑制とリンの取り込みで支持を集めています。カプセル化の進歩により保存安定性が向上し、最近のEPA耐性免除により承認がスムーズに進みます。細菌性の既存企業は規模の優位性を維持しているが、真菌類の革新的企業はストレス緩和の優れた利点で投資を集めています。

地域分析

北米は、旺盛な研究開発活動と確立された投入農薬流通網に支えられ、2024年に最大の地域シェアを維持した。この地域の2030年までのCAGRは6.9%で世界平均を下回るが、これは多くの生産者が生物学的肥料が化学合成肥料の信頼性に匹敵するという確信を持っていないためです。規制経路は徐々に改善されつつあり、バチルス菌とトリコデルマ菌株に対する最近のEPA免除措置により、新製品の市場投入までの時間が短縮されました。農家への継続的な教育と炭素クレジットの統合により、コーンベルトとプレーリー州全域で採用が進む可能性があります。

南米はCAGR10.4%で最も急成長している地域です。ブラジルの国家バイオ投入物プログラムは、2023~24年シーズンに50億ブランドル(10億米ドル)の売上を計上し、15%増となりました。アルゼンチンの成熟した大豆接種インフラは、ブラジルの積極的な新規作物への取り組みを補完し、大陸全体のホットスポットを形成しています。ICLによるNitro 1000の買収やFMCによるBallagroとの提携に見られるように、多国籍企業は規制上の足がかりと生産能力を確保するため、現地での提携を深めています。

アジア太平洋とアフリカには新たなビジネスチャンスがあり、それぞれCAGR 9.8%と8.3%で成長しています。中国では550以上の微生物農薬製品が登録され、規制の勢いを示しており、インドの中央殺虫剤委員会(Central Insecticides Board)は2024年初頭に416の生物学的製剤を承認しました。アフリカでは、農場での根粒菌増殖のような零細農家に優しいアプローチがコールドチェーンの制約を回避しているが、より広範な市場開拓は、改良普及支援と接種剤散布設備への資金アクセスに依存しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 有機認証基準への移行

- 耕作地の減少と食糧安全保障への圧力

- 政府の肥料補助金のバイオインプットへの再編

- 種子応用生物コンソーシアムの急速な拡大

- 微生物のカプセル化技術へのベンチャー投資

- 生物学的窒素固定のための炭素クレジットの収益化

- 市場抑制要因

- 農家の意識ギャップと農場での取り扱いの複雑さ

- 速効性合成肥料の好み

- 微生物カクテルの規制上のグレーゾーン

- 拡張サプライチェーンにおける生物学的汚染リスク

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 機能別

- 作物栄養

- 農作物保護

- 微生物別

- 細菌

- 根圏細菌

- アゾトバクター

- リン酸化細菌

- その他の細菌

- 菌類

- トリコデルマ

- 菌根

- その他の菌類

- その他の微生物

- 細菌

- 使用方法別

- 種子接種

- 土壌接種

- 作物タイプ別

- 穀物

- 豆類と油糧種子

- 商業作物

- 果物と野菜

- その他の用途

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東

- サウジアラビア

- アラブ首長国連邦

- その他中東

- アフリカ

- 南アフリカ

- ケニア

- その他アフリカ

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- BASF SE

- Novonesis(Novozymes A/S)

- Corteva Agriscience

- Premier Tech Ltd.

- Lallemand Inc.

- Lesaffre-Agrauxine(Lesaffre Group)

- Bioceres Crop Solutions Corp.

- Verdesian Life Sciences(AEA Investors)

- Mapleton Agri Biotec

- New Edge Microbials

- T. Stanes and Company(Amalgamations Group)

- Valent BioSciences(Sumitomo Chemical)

- Bayer AG

- Syngenta AG(ChemChina)