|

市場調査レポート

商品コード

1404356

神経調節:市場シェア分析、産業動向と統計、2024~2029年の成長予測Neuromodulation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 神経調節:市場シェア分析、産業動向と統計、2024~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 115 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

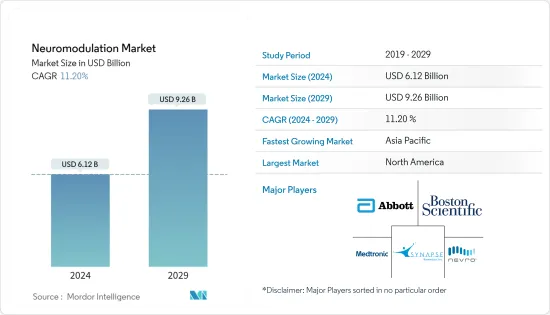

神経調節市場規模は2024年に61億2,000万米ドルと推定・予測され、2029年には92億6,000万米ドルに達し、予測期間中(2024-2029年)にCAGR 11.20%で成長すると予測されます。

主なハイライト

- COVID-19パンデミックの発生は、2020年の初期段階において調査市場に大きな影響を与えました。政府の規制に従い、神経調節術を含む選択的手術やその他の治療が延期されました。神経調節術は対象患者の治療のために外科的介入を必要とするため、神経調節術の延期は、施術中に使用される機器の需要と供給に障害をもたらしました。このため、システムや機器の採用や販売が妨げられ、調査対象の市場に悪影響を及ぼしました。

- しかし、2021年には、COVID-19患者が神経調節デバイスを使用することで恩恵を受けていることを示唆する多くの研究の結果として、神経調節のニーズが増加しました。例えば、2021年7月にEuropean Pharmaceutical Review誌に掲載された調査研究によると、慢性的なCOVID-19の症状を持つ患者グループの治療に神経調節が使用され、治療開始から14日以内にすべての患者から症状の有意な改善が報告されました。

- したがって、このような事例は、パンデミックの後期における神経調節手技の採用に拍車をかけた。一方、SARS-CoV-2ウイルスの様々な株の発症とそれに伴うCOVID後の症状により、神経調節技術の適用が増加しており、予測期間中に調査市場の成長に寄与すると予想されています。

- 神経疾患の有病率の上昇、高齢化人口の増加、新たな適応症や対象用途の拡大などの要因が、主に分析期間中の市場全体の成長を促進すると予測されています。

- 認知症やその他の神経障害を患う人口数は世界的に増加しており、神経調節技術や処置の採用や開発に多くの機会が生まれると予想されています。2022年8月にNeuroscience Insights誌に掲載された調査研究によると、世界各国の疫学データを分析したところ、認知症、アルツハイマー病、パーキンソン病、多発性硬化症、運動ニューロン疾患の有病率と世界の負担の増加は、調査期間中、世界195カ国で高いと報告されました。したがって、このような神経疾患の負担は、神経調節デバイスの機会を生み出し、市場全体の成長をさらに促進すると予想されます。

- さらに、神経疾患の重荷により、多くの市場関係者が神経調節製品の開拓に注力しています。このため、市場競争は激化しています。例えば、2021年1月、Functional Neuromodulation社は、Vercise Deep Brain Stimulation(DBS)Systemsについて、米国のCentre for Devices and Radiological HealthからBreakthrough Deviceの指定を受けました。ファンクショナル・ニューロモジュレーション社は、アルツハイマー病の治療を目的とした脳深部刺激装置BDS-f DBSシステムを開発しました。65歳以上の軽度アルツハイマー病患者が治療の対象となります。このアプローチにより、有効性の確立と普及拡大が期待されます。

- さらに2022年7月、アボット・ラボラトリーズはFDAのBreakthrough Device Designationの認定を受け、重度の治療抵抗性うつ病の管理における脳深部刺激療法(DBS)の使用を調査できるようになった。

- そのため、さまざまな製品が入手可能になり、予測期間中に市場需要が急増すると予想されます。しかし、一貫性のない償還政策と訓練を受けた専門家の不足が、予測期間中の市場成長の妨げになると予想されます。

神経調節市場の動向

深部脳刺激(DBS)セグメントが大きなシェアを占めると予測

- 深部脳刺激(DBS)セグメントは、分析期間中、調査市場において大きなシェアを占めると予測されています。DBSは、慢性疼痛、てんかん、パーキンソン病(PD)、ジストニア、振戦などの運動障害、トゥレット症候群、強迫性障害、うつ病などの精神疾患の治療に推奨されています。

- DBSにはいくつかの利点があり、そのためエンドユーザーの間でこの技術の採用が増加しています。DBSの適用が承認されているのは、本態性振戦、PD、ジストニア、強迫性障害など一部の疾患だけです。しかし、技術の進歩に伴い、DBSの応用が台頭してきています。

- 2022年9月にNeurology Perspectives Journalに掲載された調査結果によると、DBSの使用は増加し、神経疾患、精神外科、さらには全身疾患にますます焦点が当てられており、この処置は運動障害に最も使用されています。したがって、他の用途へのDBSの高い採用率は、予測期間中の同分野の成長に寄与すると予想されます。

- さらに、メーカーは現在、現行のDBSシステムを強化する一方で、新世代の装置を開発しています。脳のさまざまな領域がDBSの標的となっており、パーキンソン病患者などさまざまな患者集団で治療法が検討されています。例えば、アボット社は2022年7月、治療抵抗性うつ病(TRD)における脳深部刺激(DBS)システムの使用を調査するため、FDAの画期的医療機器指定を受けました。

- さらに2022年9月、アレバ・ニューロセラピューティクス社は、directSTIM脳深部刺激(DBS)システムの磁気共鳴画像(MRI)ラベリングのCEマーク承認を取得し、欧州全域でこの技術を全身MRI環境で使用できるようになった。

- したがって、これらすべての新しい技術の進歩は、DBSの採用の増加につながり、調査された市場の成長を推進しています。

分析期間中、北米が大きな市場シェアを占める見込み

- 北米は神経調節市場全体で大きなシェアを占めており、今後数年間も成長傾向が続くと予測されています。さらに、カナダとメキシコは、分析期間中に調査された市場でかなりのシェアを占めると予想されています。

- 確立された市場プレーヤーや巨大な製薬・バイオ医薬品産業の存在と、米国における先端技術導入のための投資の高まりが相まって、同国の市場成長を後押しすると予想されます。例えば、Parkinson's Foundationが2022年に更新したデータによると、米国では毎年約9万人がパーキンソン病(PD)と診断されており、これは以前推定されていた年間6万人の診断率から50%増加したことになります。

- また、上記の出典にあるように、北米では過去10年間にPDの罹患率が増加しており、これは多発性硬化症、筋ジストロフィー、ルー・ゲーリッグ病と診断された人の合計数よりも多いです。PDの患者数は2030年までに120万人に達すると予想されています。そのため、この国の研究者たちは、これらの神経疾患を管理するために神経調節を幅広く研究しています。このことは、革新的な神経調節装置に新たな機会をもたらし、同地域の研究市場全体の成長を促進すると予想されます。

- さらに、同地域では食品医薬品局(FDA)による継続的な製品承認が市場競争を激化させており、これがさらに先進的な製品のイノベーションの機会を生み出すと期待されています。例えば、2022年1月、Medtronic plcは、糖尿病性末梢神経障害(DPN)に伴う慢性疼痛治療用の充電式神経刺激装置Intellisと充電不要の神経刺激装置VantaのFDA承認を取得しました。

- さらに、2022年3月には、サルーダのEvoke脊髄刺激システムが、腰痛症、難治性腰痛症、下肢痛に伴う片側または両側の痛みを含む、体幹および/または四肢の慢性難治性疼痛の治療に適応するFDAの承認を取得しました。したがって、こうした規制当局の承認と現在進行中の神経調節技術の開発が北米の神経調節市場の成長に拍車をかけ、同地域の市場全体の成長を加速させると予想されます。

神経調節産業の概要

神経調節市場は適度な競争状態にあります。さまざまな公的機関や民間企業による技術革新と投資の増加により、世界的に業界の競争が激化すると予想されます。同市場における主な業界プレイヤーとしては、Medtronic PLC、Boston Scientific Corporation、Abbott Laboratories、Synapse Biomedical Inc.、Nevro Corporationなどが挙げられます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 神経疾患の有病率の上昇

- 高齢化人口の増加

- 新たな適応症と対象用途の拡大

- 市場抑制要因

- 一貫性のない償還政策

- 訓練された専門家の不足

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(金額ベース市場規模)

- 技術別

- 体内神経調節

- 脊髄刺激(SCS)

- 脳深部刺激療法(DBS)

- 迷走神経刺激(VNS)

- 仙骨神経刺激(SNS)

- 胃電気刺激(GES)

- 体外神経調節(非侵襲性)

- 経皮的電気神経刺激(TENS)

- 経頭蓋磁気刺激(TMS)

- その他の体外神経調節

- 体内神経調節

- 用途別

- パーキンソン病

- てんかん

- うつ病

- ジストニア

- 疼痛管理

- その他の用途

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Abbott Laboratories

- Boston Scientific Corporation

- Medtronic PLC

- Nevro Corporation

- Neuropace Inc.

- Neurosigma Inc.

- Neuronetics Inc.

- LivaNova PLC

- Nuvectra

- Synapse Biomedical Inc.

- Bioness

- Soterix Medical

第7章 市場機会と今後の動向

The Neuromodulation Market size is estimated at USD 6.12 billion in 2024, and is expected to reach USD 9.26 billion by 2029, growing at a CAGR of 11.20% during the forecast period (2024-2029).

Key Highlights

- The onset of the COVID-19 pandemic significantly impacted the studied market during the initial phases of 2020. Elective surgeries and other treatments were postponed in accordance with government restrictions, including neuromodulation procedures. As neuromodulation requires surgical interventions for the treatment of target patients, postponing neuromodulation procedures created obstruction in the demand and supply of the devices used during the procedures. This hampered the adoption and sales of the systems and devices and adversely impacted the market studied.

- However, in 2021, the need for neuromodulation increased as a result of numerous studies that suggested COVID-19 patients have benefited from using neuromodulation devices. For instance, as per a research study published in the European Pharmaceutical Review journal in July 2021, neuromodulation was used to treat a group of patients with chronic COVID-19 symptoms, and all of them reported significant improvements in their symptoms within 14 days of beginning the treatment.

- Hence, such instances fueled the adoption of neuromodulation procedures during the later phases of the pandemic. Meanwhile, with the onset of various strains of the SARS-CoV-2 virus and associated post-COVID symptoms, the application of neuromodulation technologies is increasing and is anticipated to contribute to the growth of the studied market during the forecast period.

- Factors such as the rising prevalence of neurological disorders, the increase in the aging population, and new indications and expanded target applications are primarily anticipated to drive the overall market growth during the analysis period.

- The number of populations suffering from dementia and other neurological disorders is rising globally, and it is expected to create numerous opportunities for the adoption and development of neuromodulation technologies and procedures. According to a research study published in the Neuroscience Insights journal in August 2022, when the epidemiological data from several countries across the globe were analyzed, the prevalence and increasing global burden of dementia, Alzheimer's Disease, Parkinson's disease, multiple sclerosis, and motor neuron diseases was reported to be high in 195 countries worldwide, during the study period. Hence, this burden of neurological diseases is anticipated to create opportunities for neuromodulation devices, further driving the overall growth of the market.

- Moreover, the burden of neurological diseases has led many market players to focus on the development of neuromodulation products. This is creating a competitive environment in the market studied. For instance, in January 2021, Functional Neuromodulation received the Breakthrough Device designation from the Centre for Devices and Radiological Health, the United States, for the Vercise Deep Brain Stimulation (DBS) Systems. Functional Neuromodulation has developed a deep brain stimulator BDS-f DBS system designed to treat Alzheimer's. Patients with mild probable Alzheimer's disease who are 65 years of age or older are eligible for therapy. With this approach, the established effectiveness and expanding adoption of this technology are expected.

- In addition, in July 2022, Abbott Laboratories received FDA Breakthrough Device Designation recognition, which allows them to investigate the use of deep brain stimulation (DBS) in managing severe treatment-resistant depression.

- Therefore, the availability of various products is expected to lead to a surge in market demand during the forecast period. However, inconsistent reimbursement policies and a lack of trained professionals are expected to hinder the market growth during the forecast period.

Neuromodulation Market Trends

Deep Brain Stimulation (DBS) Segment is Predicted to Hold a Significant Share

- The deep brain stimulation (DBS) segment is predicted to hold a significant share of the studied market during the analysis period. DBS is recommended for the treatment of chronic pain, epilepsy, movement disorders like Parkinson's disease (PD), dystonia, and tremors, as well as for some psychiatric conditions like Tourette syndrome, obsessive-compulsive disorder, and depression.

- There are several advantages associated with DBS, due to which the adoption of the technology is on the rise among the end users. Even if the application of DBS is approved for a few conditions such as essential tremor, PD, dystonia, and obsessive-compulsive disorder. However, with advancements in technologies, the application of DBS is emerging.

- As per a research study published in the Neurology Perspectives Journal in September 2022, the use of DBS is growing and increasingly focused on neurological diseases, psychosurgery, and even systemic diseases, and this procedure has been of greatest use for movement disorders. Hence, this high adoption of DBS for other applications is expected to contribute to the segment's growth during the forecast period.

- Moreover, manufacturers are currently developing a new generation of devices while enhancing their current DBS systems. Different regions of the brain are being targeted by DBS, and the treatment is being examined in various populations of patients, such as Parkinson's patients. For example, in July 2022, Abbott received the FDA Breakthrough Device Designation to investigate the use of its deep brain stimulation (DBS) system in treatment-resistant depression (TRD).

- In addition, in September 2022, Aleva Neurotherapeutics received CE-mark approval for its magnetic resonance imaging (MRI) labeling for the directSTIM deep brain stimulation (DBS) system, allowing the technology to be used in a full-body MRI environment across Europe.

- Hence, all these new advancements in technologies have led to an increase in the adoption of DBS, driving the growth of the market studied.

North America is expected to Hold a Significant Market Share During the Analysis Period

- North America held a significant share of the overall neuromodulation market and is anticipated to continue its growth trend during the coming years, with the United States being the major contributor to the market. In addition, Canada and Mexico are expected to hold a considerable share of the market studied over the analysis period.

- The presence of established market players and huge pharmaceutical and biopharmaceutical industries, coupled with the rising investments in the United States for the adoption of advanced technologies, are expected to boost the growth of the market in the country. For instance, as per the data updated by the Parkinson's Foundation in 2022, approximately 90,000 people are diagnosed with Parkinson's disease (PD) every year in the United States, which represents a 50% increase from the previously estimated rate of 60,000 diagnoses annually.

- In addition, as per the source above, the incidence of PD has increased in North America in the past decade, which is more than the combined number of people diagnosed with multiple sclerosis, muscular dystrophy, and Lou Gehrig's disease. The number of patients affected with PD is expected to rise to 1.2 million by 2030. Hence, the researchers of the country extensively research neuromodulation to manage these neurological diseases. This is anticipated to open new opportunities for innovative neuromodulation devices and garner the overall growth of the studied market in the region.

- Additionally, continuous product approvals by the Food and Drug Administration (FDA) in the region are increasing competition in the market, which is further expected to create opportunities for the innovation of advanced products. For instance, in January 2022, Medtronic plc received FDA approval for its Intellis rechargeable neurostimulator and Vanta recharge-free neurostimulator for the treatment of chronic pain associated with diabetic peripheral neuropathy (DPN).

- Moreover, in March 2022, Saluda's Evoke spinal cord stimulation system received approval from the FDA that is indicated for the treatment of chronic intractable pain of the trunk and/or limbs, including unilateral or bilateral pain associated with failed back surgery syndrome, intractable low back pain, and leg pain. Hence, these regulatory approvals and the ongoing development of neuromodulation technologies are expected to spur the growth of the neuromodulation market in North America, thereby accelerating the overall market growth in the region.

Neuromodulation Industry Overview

The neuromodulation market is moderately competitive. The increasing innovation and investment for various public and private organizations are expected to intensify industry rivalry worldwide. The major industry players in the market include Medtronic PLC, Boston Scientific Corporation, Abbott Laboratories, Synapse Biomedical Inc., and Nevro Corporation, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Neurological Disorders

- 4.2.2 Increase in the Aging Population

- 4.2.3 New Indications and Expanded Target Applications

- 4.3 Market Restraints

- 4.3.1 Inconsistent Reimbursement Policies

- 4.3.2 Lack of Trained Professionals

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value )

- 5.1 By Technology

- 5.1.1 Internal Neuromodulation

- 5.1.1.1 Spinal Cord Stimulation (SCS)

- 5.1.1.2 Deep Brain Stimulation (DBS)

- 5.1.1.3 Vagus Nerve Stimulation (VNS)

- 5.1.1.4 Sacral Nerve Stimulation (SNS)

- 5.1.1.5 Gastric Electrical Stimulation (GES)

- 5.1.2 External Neuromodulation (Non-invasive)

- 5.1.2.1 Transcutaneous Electrical Nerve Stimulation (TENS)

- 5.1.2.2 Transcranial Magnetic Stimulation (TMS)

- 5.1.2.3 Other External Neuromodulations

- 5.1.1 Internal Neuromodulation

- 5.2 By Application

- 5.2.1 Parkinson's Disease

- 5.2.2 Epilepsy

- 5.2.3 Depression

- 5.2.4 Dystonia

- 5.2.5 Pain Management

- 5.2.6 Other Applications

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abbott Laboratories

- 6.1.2 Boston Scientific Corporation

- 6.1.3 Medtronic PLC

- 6.1.4 Nevro Corporation

- 6.1.5 Neuropace Inc.

- 6.1.6 Neurosigma Inc.

- 6.1.7 Neuronetics Inc.

- 6.1.8 LivaNova PLC

- 6.1.9 Nuvectra

- 6.1.10 Synapse Biomedical Inc.

- 6.1.11 Bioness

- 6.1.12 Soterix Medical