|

|

市場調査レポート

商品コード

1685730

眼科薬:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Ophthalmic Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 眼科薬:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 114 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

眼科薬の市場規模は、2025年に374億9,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは8.24%で、2030年には557億1,000万米ドルに達すると予測されます。

業界の革新と拡大を促進する様々な要因に支えられ、著しい成長を遂げています。主な促進要因としては、眼に関連する疾患の有病率の増加や、市場展望を再構築している医薬品開発技術の進歩などが挙げられます。

業界を形成するメガ動向:眼疾患の世界の増加、人口の高齢化、薬剤製剤技術の進歩が市場成長の強固な基盤となっています。これらの要因は、特定の業界促進要因とともに、眼科薬業界を新たな高みへと押し上げています。

目に関連する障害の発生率と有病率の増加:視力障害を持つ人の増加が市場成長を促進する主な要因です。National Eye Instituteのデータによると、2030年までに加齢黄斑変性が米国で370万人に影響を及ぼすと予測されています。さらに、同じ情報源は、緑内障が2030年までに430万人の米国人に影響を及ぼすと推定しています。これらの眼疾患の負担の大きさは、新しく効果的な眼科治療に対する緊急の必要性を強調し、市場を前進させる。

新薬開発に関わる研究開発の高まり:眼科薬の世界市場調査によると、業界は新規治療ソリューションの創出を目的とした研究開発活動の増加から恩恵を受けています。臨床試験と医薬品承認の増加はこの動向を浮き彫りにしています。2023年、FDAはドライアイ用の新規抗炎症剤CyclASolの新薬申請を受理しました。同様に、Xbrane Biopharma ABとSTADA Arzneimittel AGによるラニビズマブのバイオシミラーの欧州での発売は、費用対効果の高い治療選択肢の急増を示しています。このような革新的な医薬品は治療領域を拡大し、市場成長率を押し上げています。

併用療法開発への注目の高まり:眼科薬市場では、併用療法への注目が高まっています。これらの治療は、複雑な眼疾患の管理に優れた治療効果をもたらします。例えば、2023年7月、Tenpoint Therapeutics社は、変性性眼疾患と闘うことを目的とした発売の先陣を切るための資金を確保しました。同社は、様々な細胞ベースの治療薬を組み合わせ、個々の症例に合わせた治療を行うことを専門としています。同社のアプローチは、加齢や遺伝性疾患によって損なわれた眼球細胞を若返らせることを中心としています。このようなパートナーシップは、この分野での技術革新に拍車をかけ、アンメット・メディカル・ニーズへの対応によって市場拡大を加速させています。

世界の産業は、こうした市場動向や開発に牽引され、着実な成長軌道に乗っています。医薬品イノベーション、個別化治療、眼科医療へのアクセス向上における今後の進歩は、引き続き業界を形成していくと思われます。目の健康に対する人々の意識が高まり、早期介入がより重要になるにつれて、市場は持続的な成長を遂げる態勢が整っています。

眼科薬市場の動向

処方薬:眼科治療における原動力

セグメントの概要:処方薬は眼科治療において極めて重要な役割を果たしており、緑内障、ドライアイ、網膜疾患など幅広い症状に対応しています。これらの医薬品は、その効能と精度の高さゆえに医学的な監視が必要です。処方箋眼科治療薬は市場シェアの約65%を占めており、眼科治療管理における支配的な役割を示しています。

成長の原動力:加齢黄斑変性や緑内障などの慢性眼疾患の有病率の上昇が、処方眼科薬の需要を押し上げています。徐放性技術や併用療法の進歩により、患者のコンプライアンスと治療成績がさらに向上しています。世界の高齢化社会は特にこれらの疾患に罹患しやすく、業界の研究開発努力の増加とともに、この分野の成長を後押しすると予想されます。

競合情勢:処方薬市場の主要企業は、競争力を高めるために技術革新に注力しています。硝子体内インプラントのような先進ドラッグデリバリーシステムの開発は、複雑な眼疾患に対する新たな解決策を提供しています。戦略的提携や買収は製品ポートフォリオを拡大し、個別化医療の台頭は標的治療の開発を促進しています。しかし、遺伝子治療や再生医療を含む潜在的な混乱が市場を再編成する可能性もあります。

北米:眼科医療イノベーションの牽引役

地域のダイナミクス:北米は引き続き世界の眼科薬市場規模をリードしており、力強い成長とイノベーションを示しています。高度に発達したヘルスケアインフラと強力な市場プレゼンスにより、北米は2024年から2029年にかけてCAGR8%以上で拡大すると予想されています。この成長の原動力となるのは、技術の進歩、ヘルスケア投資の増加、目の健康に対する意識の高まりです。

マーケットカタリスト:北米が眼科薬で優位に立つ原動力となっている要因はいくつかあります。同地域は高齢化が進んでおり、生活習慣に関連した眼疾患が蔓延しているため、患者数が多いです。また、好意的な保険償還政策と支援的な規制環境も、医薬品の技術革新と患者の治療へのアクセスを後押ししています。産業研究への旺盛な資金供給と精密医療への注力により、北米は眼科薬開発におけるリーダーシップを維持すると予想されます。

戦略的課題市場での地位を維持するため、企業は遺伝子治療や再生医療などの研究分野に投資しています。イノベーションを加速するためには、バイオテクノロジー企業や学術機関との連携が不可欠です。さらに、遠隔医療や人工知能(AI)を含むデジタル・ヘルス・ソリューションが、眼科医療に統合されつつあります。企業はまた、ハイテク企業の参入やバリュー・ベース・ケア・モデルによる競合情勢の潜在的な変化にも備える必要があります。

眼科薬業界の概要

市場力学:世界プレーヤーが統合情勢を支配

この世界の業界は、幅広い製品ポートフォリオを持つ大手多国籍製薬企業によってほぼ支配されています。ノバルティス、ロシュ、リジェネロンなどの主要企業は、その広範な研究開発能力と強力な販売網により、眼科薬市場で大きなシェアを占めています。市場は統合されており、少数の市場リーダーや主要企業が総売上の大部分を占めています。参入障壁が高く、規制の枠組みが複雑で、研究開発に多額の投資を必要とするため、新規参入企業が既存企業と競争するのは困難です。

市場リーダーイノベーションとパイプラインの強さが成功の原動力

ノバルティス、ロシュ、リジェネロン・ファーマシューティカルズといった主要企業は、網膜疾患治療やその他の眼科領域で大きな進歩を遂げています。ノバルティスの網膜治療における技術革新や、リジェネロンの加齢黄斑変性治療におけるEYLEAの成功がその例です。また、これらのマーケットリーダーは、今後数年間に上市が予定されている複数の後期臨床候補化合物を有する強力な製品パイプラインによっても強化されています。広大な世界プレゼンスとヘルスケア利害関係者との深い関係が、競合優位性を確固たるものにしています。

将来の成功に向けた戦略アンメットニーズと新技術への注力

将来の市場成長を獲得するためには、企業は眼科領域のアンメットニーズ、特にドライアイや糖尿病性網膜症などの治療に注力する必要があります。遺伝子治療や徐放性ドラッグデリバリーシステムなどの新技術を活用すれば、競争力を高めることができると思われます。例えば、緑内障用の長時間作用型眼内インプラントを開発する企業は、従来の治療から大きな市場シェアを獲得できる可能性があります。アジア太平洋のような高成長地域への進出は、イノベーションを促進するためのバイオテクノロジー企業や研究機関との提携と並んで重要です。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 眼に関連する疾患の発生率と有病率の増加

- 新薬開発に関わる研究開発の活発化

- 併用療法開発への注目の高まり

- 市場抑制要因

- 大衆薬の特許切れ

- 新興諸国における医療保険の欠如

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 薬剤クラス別

- 抗緑内障薬

- ドライアイ治療薬

- 眼科用抗アレルギー/抗炎症薬

- 網膜用薬

- 抗感染症薬

- その他の医薬品

- 製品タイプ別

- 一般用医薬品

- 処方薬

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東とアフリカ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Aerie Pharmaceuticals Inc.

- AbbVie(Allergan)

- Bausch Health Companies Inc.

- Bayer AG

- F. Hoffmann-La Roche Ltd

- Novartis AG

- Viatris Inc.

- Regeneron Pharmaceuticals Inc.

- Santen Pharmaceutical Co. Ltd

- Alcon

- Sun Pharmaceutical Industries Ltd.

- Teva Pharmaceutical Industries Ltd.

第7章 市場機会と今後の動向

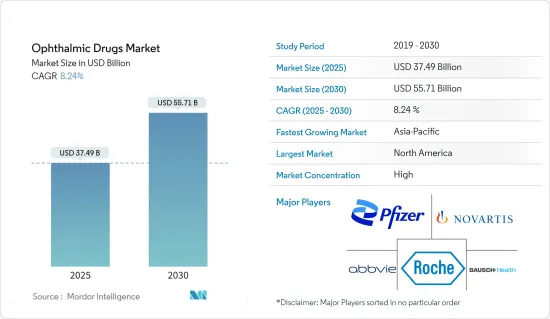

The Ophthalmic Drugs Market size is estimated at USD 37.49 billion in 2025, and is expected to reach USD 55.71 billion by 2030, at a CAGR of 8.24% during the forecast period (2025-2030).

It is witnessing significant growth, underpinned by various factors driving both innovation and expansion in the industry. Key drivers include the increasing prevalence of eye-related disorders and advancements in drug development technologies, which are reshaping the market landscape.

Megatrends Shaping the Industry: The global rise in ocular conditions, an aging population, and advancements in drug formulation technologies are creating robust foundations for market growth. These factors, along with specific industry drivers, are pushing the ophthalmic drugs industry to new heights.

Increasing Incidence and Prevalence of Eye-related Disorders: The growing number of individuals with vision impairment is a major factor driving the market growth. Data from the National Eye Institute projects that by 2030, age-related macular degeneration will impact 3.7 million individuals in the United States. Additionally, the same source estimates that glaucoma will affect 4.3 million Americans by 2030. The high burden of these eye diseases underscores the urgent need for new and effective ophthalmic treatments, driving the market forward.

Rising Research and Development Pertaining to the Development of Novel Drugs: Global ophthalmic drugs market research says that the industry is benefiting from increased R&D activity aimed at creating novel therapeutic solutions. The rise in clinical trials and drug approvals highlights this trend. In 2023, the FDA accepted a New Drug Application for CyclASol, a novel anti-inflammatory product for dry eye disease. Similarly, the European launch of a ranibizumab biosimilar by Xbrane Biopharma AB and STADA Arzneimittel AG showcases the surge in cost-effective treatment options. These innovative drugs are expanding the therapeutic landscape and boosting the market at a decent growth rate.

Increasing Focus on Developing Combination Therapies: The emphasis on combination therapies within the ophthalmic drugs market is growing. These treatments offer superior therapeutic results for managing complex ocular diseases. For instance, in July 2023, Tenpoint Therapeutics secured funding to spearhead its launch aimed at combating degenerative eye diseases. The company specializes in combining various cell-based therapeutics and crafting treatments tailored to individual cases. Their approach centers on rejuvenating eye cells compromised by age-related or inherited ailments. Such partnerships are fueling innovation in the field, accelerating market expansion by addressing unmet medical needs.

Global industry is on a steady growth trajectory, driven by these market trends and developments. Future advancements in drug innovation, personalized treatments, and increased access to eye care will continue to shape the industry. As public awareness around eye health rises and early intervention becomes more critical, the market is poised for sustained growth.

Ophthalmic Drugs Market Trends

Prescription Drugs: Driving Force in Ophthalmic Treatments

Segment Overview: Prescription drugs play a pivotal role in ophthalmic treatments, addressing a wide range of conditions including glaucoma, dry eye, and retinal disorders. These drugs require medical oversight due to their potency and precision. Prescription ophthalmic medications account for approximately 65% of the market share, illustrating their dominant role in eye care management.

Growth Drivers: The rising prevalence of chronic eye disorders, such as age-related macular degeneration and glaucoma, is boosting demand for prescription ophthalmic drugs. Advances in sustained-release technologies and combination therapies are further enhancing patient compliance and treatment outcomes. The global aging population is particularly susceptible to these disorders, which, along with increasing industry research and development efforts, are expected to bolster the growth of this segment.

Competitive Landscape: Leading companies in the prescription drug market are focusing on innovation to gain a competitive edge. The development of advanced drug delivery systems, such as intravitreal implants, is providing new solutions for complex eye conditions. Strategic collaborations and acquisitions are expanding product portfolios, while the rise of personalized medicine is driving the development of targeted therapies. However, potential disruptions, including gene therapies and regenerative medicine, may reshape the market.

North America: Leading the Charge in Ophthalmic Innovation

Regional Dynamics: North America continues to lead the global ophthalmic drugs market size, exhibiting robust growth and innovation. With a highly developed healthcare infrastructure and strong market presence, North America is expected to expand at a compound annual growth rate (CAGR) of over 8% from 2024 to 2029. This growth is fueled by technological advancements, increasing healthcare investments, and rising awareness around eye health.

Market Catalysts: Several factors are driving North America's dominance in ophthalmic drugs. The region's aging population and the prevalence of lifestyle-related ocular disorders contribute to a significant patient base. Favorable reimbursement policies and a supportive regulatory environment also encourage drug innovation and patient access to treatments. With strong funding for industry research and a focus on precision medicine, North America is expected to maintain its leadership in ophthalmic drug development.

Strategic Imperatives: To maintain their market position, companies are investing in research areas like gene therapy and regenerative medicine. Collaborations with biotech firms and academic institutions are essential for accelerating innovation. Additionally, digital health solutions, including telemedicine and artific ial intelligence (AI), are increasingly integrated into eye care. Companies should also prepare for potential shifts in the competitive landscape, driven by tech entrants and value-based care models.

Ophthalmic Drugs Industry Overview

Market Dynamics: Global Players Dominate Consolidated Landscape

This global industry is largely controlled by major multinational pharmaceutical firms with broad product portfolios. Leading companies such as Novartis, Roche, and Regeneron hold substantial ophthalmic drugs market share due to their expansive R&D capabilities and strong distribution networks. The market is consolidated, with a few market leaders and key players dominating a large portion of the total revenue. High entry barriers, complex regulatory frameworks, and the need for significant investment in R&D make it challenging for new entrants to compete with established players.

Market Leaders: Innovation and Pipeline Strength Drive Success

Leading companies like Novartis, Roche, and Regeneron Pharmaceuticals Inc. have made significant strides in retinal disease treatments and other areas of ophthalmology. Novartis' innovations in retinal therapies and Regeneron's success with EYLEA in treating age-related macular degeneration exemplify this. These market leaders are also bolstered by their strong product pipelines, with several late-stage clinical candidates set to launch in the coming years. Their vast global presence and deep relationships with healthcare stakeholders solidify their competitive advantage.

Strategies for Future Success: Focus on Unmet Needs and Emerging Technologies

To capture future market growth, companies must focus on unmet needs in ophthalmology, particularly in treating conditions like dry eye disease and diabetic retinopathy. Leveraging emerging technologies such as gene therapies and sustained-release drug delivery systems could provide a competitive edge. Companies developing long-acting intraocular implants for glaucoma, for instance, could capture significant market share from traditional treatments. Expansion into high-growth regions such as the Asia-Pacific will be critical, alongside partnerships with biotechnology firms and research institutions to foster innovation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Incidence and Prevalence of Eye-related Disorders

- 4.2.2 Rising Research and Development Pertaining to the Development of Novel Drugs

- 4.2.3 Increasing Focus on Developing Combination Therapies

- 4.3 Market Restraints

- 4.3.1 Loss of Patent Protection for Popular Drugs

- 4.3.2 Lack of Health Insurance in the Developing Countries

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value- USD)

- 5.1 By Drug Class

- 5.1.1 Anti-glaucoma Drugs

- 5.1.2 Dry Eye Drugs

- 5.1.3 Ophthalmic Anti-allergy/Inflammatory

- 5.1.4 Retinal Drugs

- 5.1.5 Anti-infective Drugs

- 5.1.6 Other Drugs

- 5.2 By Product Type

- 5.2.1 OTC Drugs

- 5.2.2 Prescription Drugs

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Aerie Pharmaceuticals Inc.

- 6.1.2 AbbVie (Allergan)

- 6.1.3 Bausch Health Companies Inc.

- 6.1.4 Bayer AG

- 6.1.5 F. Hoffmann-La Roche Ltd

- 6.1.6 Novartis AG

- 6.1.7 Viatris Inc.

- 6.1.8 Regeneron Pharmaceuticals Inc.

- 6.1.9 Santen Pharmaceutical Co. Ltd

- 6.1.10 Alcon

- 6.1.11 Sun Pharmaceutical Industries Ltd.

- 6.1.12 Teva Pharmaceutical Industries Ltd.